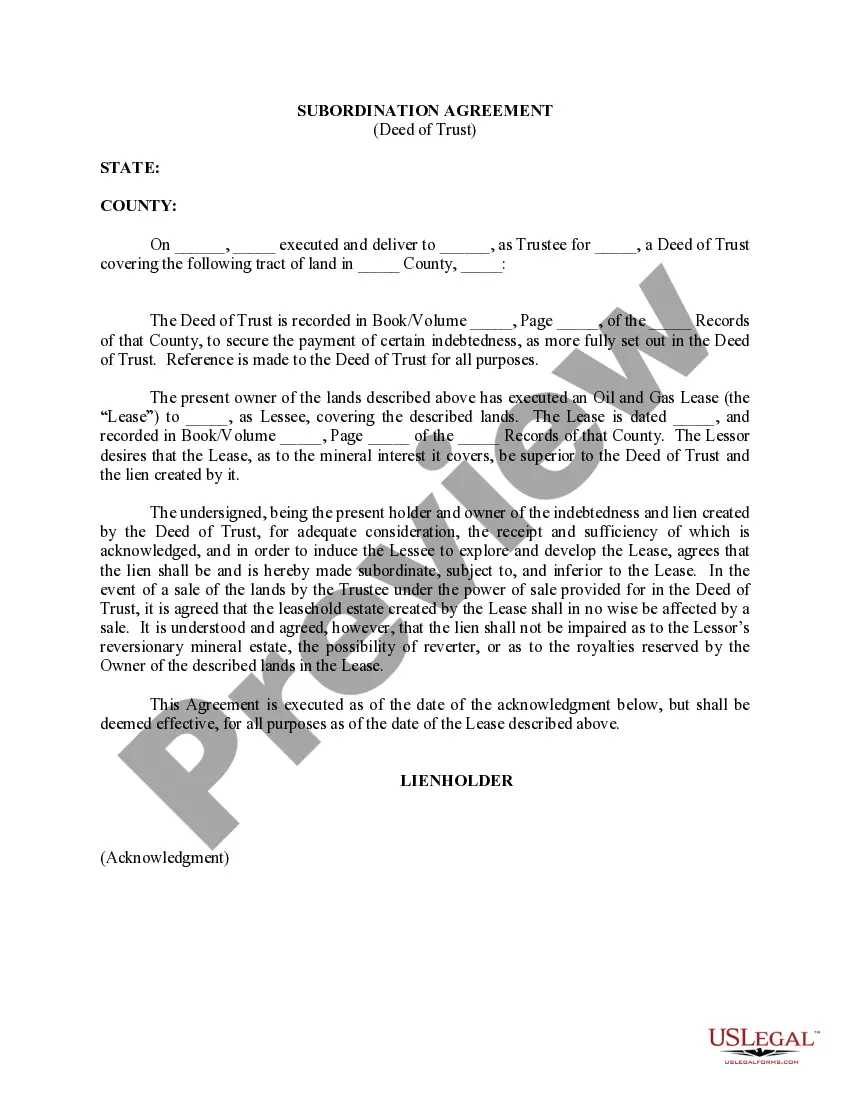

In North Carolina, a Subordination Agreement refers to a legal document known as a Deed of Trust that establishes a hierarchical order among multiple mortgage holders or lien holders. This agreement helps clarify the priority of claims in case of default or foreclosure on a property. A Subordination Agreement (Deed of Trust) is often utilized when a property owner seeks additional financing or refinancing, resulting in multiple loans secured by the same property. By entering into this agreement, the parties involved agree to modify the order of priority of their respective liens or mortgages. One example of a North Carolina Subordination Agreement is the First Lien Subordination. In this scenario, a property owner with an existing mortgage wants to obtain a second mortgage or additional financing on the same property. The first mortgage lender must agree to subordinate their lien to the new lender or subsequent lien holder. Another type of Subordination Agreement is the Second Lien Subordination. This occurs when a property owner, already having one mortgage in place, seeks to obtain a second mortgage while keeping the first one intact. In this case, the second mortgage lender agrees to subordinate their lien to the first mortgage lender. North Carolina also recognizes the concept of Subordinate Deeds of Trust, which pertain to liens or mortgages that are of lower priority compared to another lien or mortgage. This can arise in situations where the property owner has multiple financing options and wants to establish a clear order of priority among the lenders. A North Carolina Subordination Agreement (Deed of Trust) typically includes essential information such as the names of the parties involved, a legal description of the property, the original loan amount, terms and conditions of the subordinate lien, and the consent and agreement of all parties involved. Overall, a North Carolina Subordination Agreement (Deed of Trust) is a crucial legal document that determines the priority of multiple liens or mortgages on a property. It provides clarity and protects the interests of all parties involved in the event of default or foreclosure.

North Carolina Subordination Agreement (Deed of Trust)

Description

How to fill out North Carolina Subordination Agreement (Deed Of Trust)?

Choosing the best legitimate file template could be a have a problem. Naturally, there are tons of web templates available online, but how will you find the legitimate type you want? Use the US Legal Forms web site. The assistance gives a huge number of web templates, such as the North Carolina Subordination Agreement (Deed of Trust), which you can use for enterprise and private demands. All the forms are checked out by pros and fulfill state and federal demands.

When you are currently authorized, log in to your bank account and click the Acquire key to have the North Carolina Subordination Agreement (Deed of Trust). Utilize your bank account to search throughout the legitimate forms you might have bought earlier. Proceed to the My Forms tab of your own bank account and get an additional copy of your file you want.

When you are a new user of US Legal Forms, listed here are basic guidelines so that you can comply with:

- Very first, ensure you have chosen the proper type for your city/state. You are able to examine the form utilizing the Preview key and study the form outline to make sure this is the right one for you.

- In case the type is not going to fulfill your requirements, use the Seach discipline to find the appropriate type.

- When you are sure that the form is suitable, go through the Get now key to have the type.

- Select the costs strategy you want and enter the necessary information and facts. Make your bank account and purchase the transaction utilizing your PayPal bank account or Visa or Mastercard.

- Choose the data file format and acquire the legitimate file template to your gadget.

- Full, revise and print and signal the received North Carolina Subordination Agreement (Deed of Trust).

US Legal Forms may be the largest local library of legitimate forms where you can see various file web templates. Use the service to acquire professionally-made papers that comply with condition demands.

Form popularity

FAQ

The deed of trust is signed by the borrowing party and recorded with the register of deeds where the property is located. The legal description of the property is included and used as collateral. Unlike a mortgage, a deed of trust involves three parties instead of two: The borrower, aka the trustor.

Example of a Subordination Agreement A standard subordination agreement covers property owners that take a second mortgage against a property. One loan becomes the subordinated debt, and the other becomes (or remains) the senior debt. Senior debt has higher claim priority than junior debt.

For instance, usually a trust deed incorporating a subordination agreement will state that the lien of the trust deed will, on recordation, automatically be junior to the lien of another trust deed, or it will state that the new loan and deed of trust will, without any other or further instrument of subordination, ...

A subordination clause is a clause in an agreement that states that the current claim on any debts will take priority over any other claims formed in other agreements made in the future.

Let's illustrate a subordinate clause in a sentence: 'I played out until it went dark. ' The phrase 'until it went dark' is the subordinate clause because it requires additional information in order to make sense.

This Lease and any Option granted hereby shall be subject and subordinate to any ground lease, mortgage, deed of trust, or other hypothecation or security device (collectively, ?Security Device?), now or hereafter placed upon the Premises, to any and all advances made on the security thereof, and to all renewals, ...

Focusing on this geographical region, the Deed of Trust is the preferred or required security instrument for real property in the following states: Maryland, North Carolina, Tennessee, Virginia and West Virginia. Mortgages are used in Kentucky, Ohio and Pennsylvania.

A subordination agreement must be signed and acknowledged by a notary and recorded in the official records of the county to be enforceable.