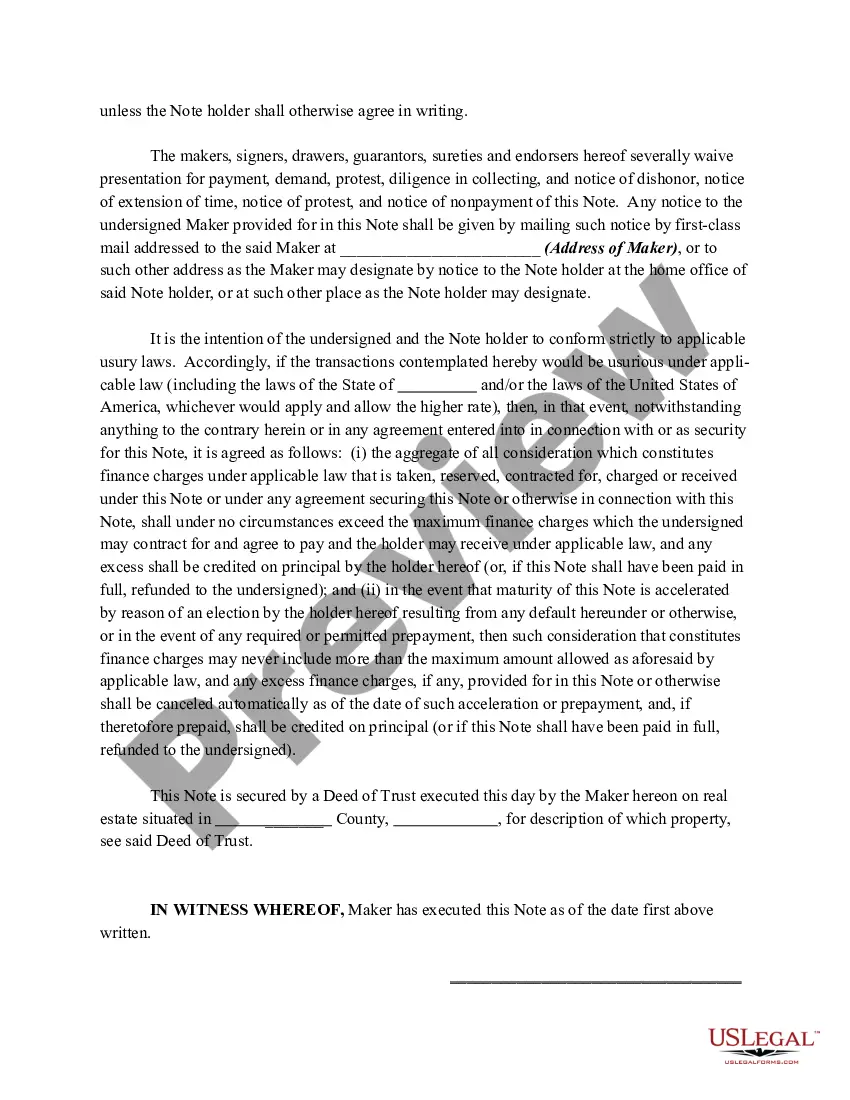

A North Dakota Promissory Note — Balloon Note is a legal document that outlines a financial agreement between a borrower and a lender. It is specifically referred to as a "Balloon Note" because it involves the gradual repayment of a loan amount over a specified period of time, with a large "balloon payment" due at the end of the term. The Balloon Note is typically used in situations where the borrower requires a lower monthly payment for a fixed period, with the expectation that they will have the resources to make a substantial final payment at the end of the agreed-upon term. This type of loan structure is commonly employed in real estate transactions and commercial financing. The North Dakota Promissory Note — Balloon Note includes essential details regarding the loan agreement, such as the principal amount borrowed, the interest rate applied to the loan, the repayment schedule (including the number of installments and their payment amounts), and the final balloon payment due date. In North Dakota, there may be variations in the types of Balloon Notes used depending on the specific circumstances. For instance, there can be residential Balloon Notes for real estate transactions, commercial Balloon Notes for business financing, and agricultural Balloon Notes for farming and agricultural operations. These different types of Balloon Notes share similar characteristics but may have some distinctions to address the particular needs of the borrowers and lenders involved. The North Dakota Promissory Note — Balloon Note is a legally binding agreement that obligates the borrower to make all scheduled payments as per the terms specified. Non-compliance or failure to fulfill the financial obligations outlined in the Balloon Note can result in severe consequences, such as penalties, late fees, or legal action. It is crucial for both borrowers and lenders to thoroughly understand all the terms and conditions outlined in the North Dakota Promissory Note — Balloon Note before signing it. Seeking legal advice or assistance from a qualified professional can be beneficial to ensure compliance with applicable laws and to protect the interests of all parties involved in the loan agreement.

North Dakota Promissory Note - Balloon Note

Description

How to fill out North Dakota Promissory Note - Balloon Note?

If you need to comprehensive, acquire, or printing legal file themes, use US Legal Forms, the most important collection of legal forms, which can be found on-line. Take advantage of the site`s easy and handy research to obtain the documents you want. Various themes for enterprise and personal functions are categorized by classes and states, or search phrases. Use US Legal Forms to obtain the North Dakota Promissory Note - Balloon Note in just a few clicks.

If you are presently a US Legal Forms buyer, log in to your account and then click the Download key to have the North Dakota Promissory Note - Balloon Note. Also you can entry forms you earlier downloaded inside the My Forms tab of the account.

If you work with US Legal Forms initially, refer to the instructions beneath:

- Step 1. Be sure you have selected the form to the right town/region.

- Step 2. Utilize the Preview method to check out the form`s content. Don`t neglect to read through the outline.

- Step 3. If you are not happy together with the develop, take advantage of the Look for field on top of the display screen to get other models from the legal develop template.

- Step 4. After you have discovered the form you want, click the Get now key. Choose the rates strategy you favor and add your qualifications to sign up for an account.

- Step 5. Procedure the financial transaction. You may use your charge card or PayPal account to perform the financial transaction.

- Step 6. Find the formatting from the legal develop and acquire it on the product.

- Step 7. Complete, edit and printing or indication the North Dakota Promissory Note - Balloon Note.

Every legal file template you acquire is yours forever. You might have acces to every develop you downloaded within your acccount. Click on the My Forms section and decide on a develop to printing or acquire once more.

Be competitive and acquire, and printing the North Dakota Promissory Note - Balloon Note with US Legal Forms. There are millions of professional and state-particular forms you may use to your enterprise or personal needs.