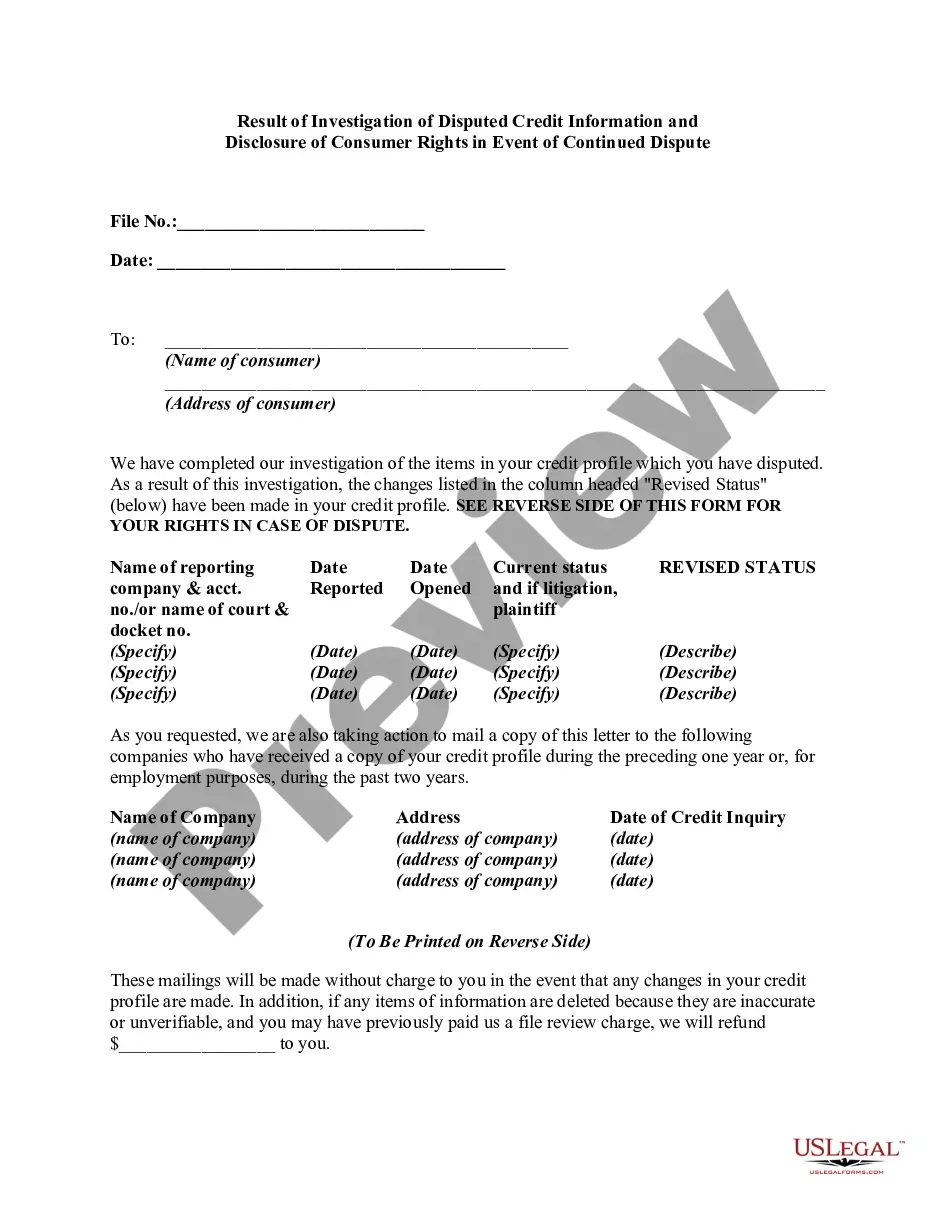

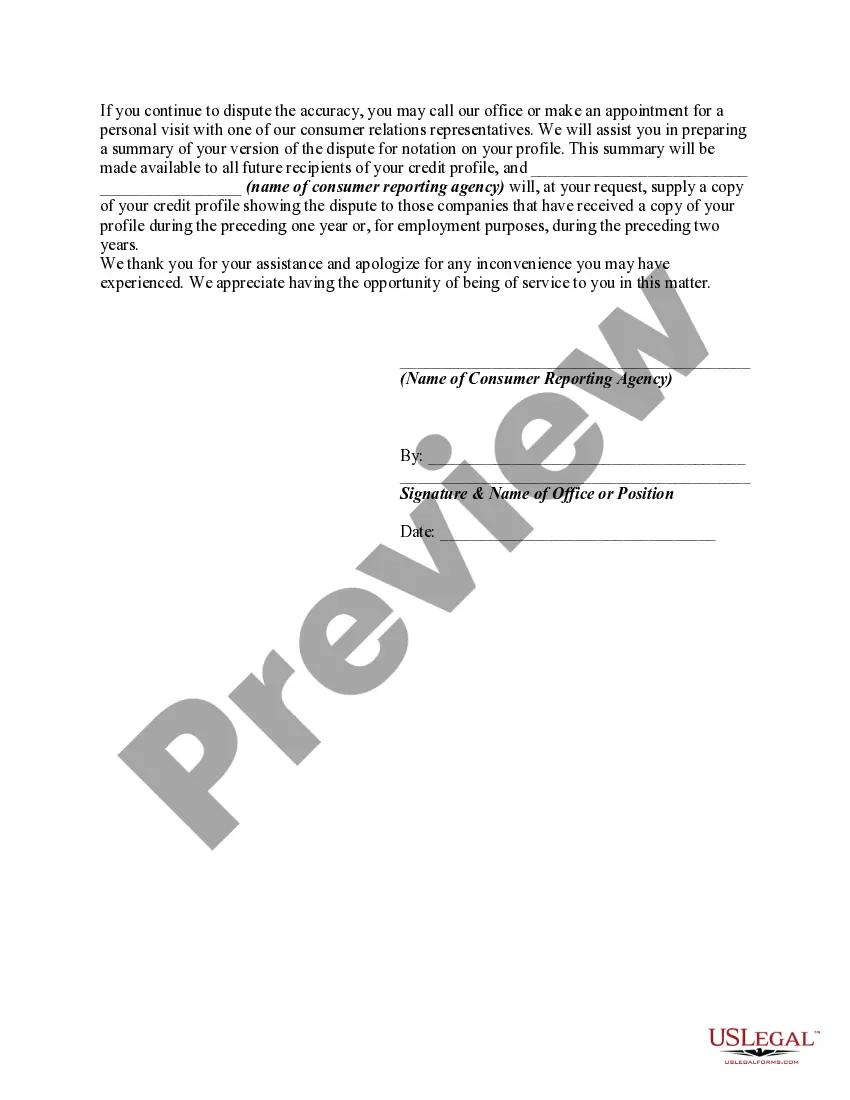

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

North Dakota Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute: When it comes to dealing with disputed credit information in North Dakota, it is crucial to understand the steps and consumer rights involved. The investigation of disputed credit information aims to determine the accuracy and legitimacy of the reported data. In this process, individuals have certain rights that must be protected. If you find errors or inconsistencies in your credit report, it is recommended to file a dispute with the credit reporting agencies (Crash) — Equifax, Experian, and TransUnion. Once the dispute is received, the Crash are obligated to conduct a thorough investigation. This investigation should be completed within 30 days, as stipulated by the Fair Credit Reporting Act (FCRA). During the investigation, the Crash will reach out to the information provider, such as lenders or collection agencies, to verify the accuracy of the disputed credit information. The information provider must also conduct an investigation and respond to the Crash. If they cannot verify the accuracy of the disputed information, it must be corrected or removed from your credit report. Additionally, if the information provider fails to respond to the Crash within the given timeframe, the disputed data should also be deleted. In the event that the investigation results in a change to your credit report, the Crash are required to provide you with a written notice. This notice should include the updated credit report and any actions taken. It is important to thoroughly review this document to ensure the corrections have been made properly. However, if the investigation does not produce the desired outcome or if the disputed information reappears on your credit report, you have the right to take further action. In such cases, you can submit a written statement explaining the nature of the dispute, which will be included in future credit reports. Additionally, you have the right to request the Crash to provide the statement to any recent recipients of your credit report. Different types of North Dakota Results of Investigation of Disputed Credit Information and Disclosure of Consumer Rights may include: 1. Successful Investigation: When the investigation reveals errors or inaccurate information, resulting in the correction or removal of the disputed credit data from your credit report. 2. Unresolved Dispute: If the investigation fails to produce the desired outcome, and the disputed credit information remains on your report without any modifications. 3. Reappearance of Disputed Information: Sometimes, even after a successful investigation, the disputed credit information may reappear on your credit report. This type of result requires further action and intervention to rectify the situation. 4. Additional Dispute Statement: In cases where the investigation does not produce the desired outcome, you have the right to submit a written statement explaining the nature of the dispute. This statement will be included in future credit reports to provide context for lenders and other recipients. Understanding your rights and the possible outcomes of a disputed credit information investigation is essential to maintain a fair and accurate credit history. Always monitor your credit report and promptly address any discrepancies to ensure your financial reputation remains intact.North Dakota Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute: When it comes to dealing with disputed credit information in North Dakota, it is crucial to understand the steps and consumer rights involved. The investigation of disputed credit information aims to determine the accuracy and legitimacy of the reported data. In this process, individuals have certain rights that must be protected. If you find errors or inconsistencies in your credit report, it is recommended to file a dispute with the credit reporting agencies (Crash) — Equifax, Experian, and TransUnion. Once the dispute is received, the Crash are obligated to conduct a thorough investigation. This investigation should be completed within 30 days, as stipulated by the Fair Credit Reporting Act (FCRA). During the investigation, the Crash will reach out to the information provider, such as lenders or collection agencies, to verify the accuracy of the disputed credit information. The information provider must also conduct an investigation and respond to the Crash. If they cannot verify the accuracy of the disputed information, it must be corrected or removed from your credit report. Additionally, if the information provider fails to respond to the Crash within the given timeframe, the disputed data should also be deleted. In the event that the investigation results in a change to your credit report, the Crash are required to provide you with a written notice. This notice should include the updated credit report and any actions taken. It is important to thoroughly review this document to ensure the corrections have been made properly. However, if the investigation does not produce the desired outcome or if the disputed information reappears on your credit report, you have the right to take further action. In such cases, you can submit a written statement explaining the nature of the dispute, which will be included in future credit reports. Additionally, you have the right to request the Crash to provide the statement to any recent recipients of your credit report. Different types of North Dakota Results of Investigation of Disputed Credit Information and Disclosure of Consumer Rights may include: 1. Successful Investigation: When the investigation reveals errors or inaccurate information, resulting in the correction or removal of the disputed credit data from your credit report. 2. Unresolved Dispute: If the investigation fails to produce the desired outcome, and the disputed credit information remains on your report without any modifications. 3. Reappearance of Disputed Information: Sometimes, even after a successful investigation, the disputed credit information may reappear on your credit report. This type of result requires further action and intervention to rectify the situation. 4. Additional Dispute Statement: In cases where the investigation does not produce the desired outcome, you have the right to submit a written statement explaining the nature of the dispute. This statement will be included in future credit reports to provide context for lenders and other recipients. Understanding your rights and the possible outcomes of a disputed credit information investigation is essential to maintain a fair and accurate credit history. Always monitor your credit report and promptly address any discrepancies to ensure your financial reputation remains intact.