Gift taxes are taxes that supplement the Estate Tax. Gift taxes are placed on gifts given away to any person while you are still living, so that you may not avoid estate taxes by making gifts of your estate. You may give up to $12,000 a year in cash or assets to an unlimited number of people each year without incurring gift tax liability, but the gifts must have no conditions attached. Married couples can give, as a couple, a $24,000 gift per year to as many people as they want. Under federal tax law, gifts totaling more than $12,000 to one person in one year are considered a taxable gift and generate a potential gift tax. It does not matter if you give one $13,000 gift or 13 gifts of $1,000 each, or one gift of $12,000 and a "birthday gift" of $1,000.

Gifts beyond the $12,000 limit (there is an exception for gifts that are directly paid by the gift giver for tuition and medical expenses) are considered "taxable gifts." Taxable gifts create liability for a gift tax. But gift tax is not due to be paid until you give away over $1,000,000 in your lifetime.

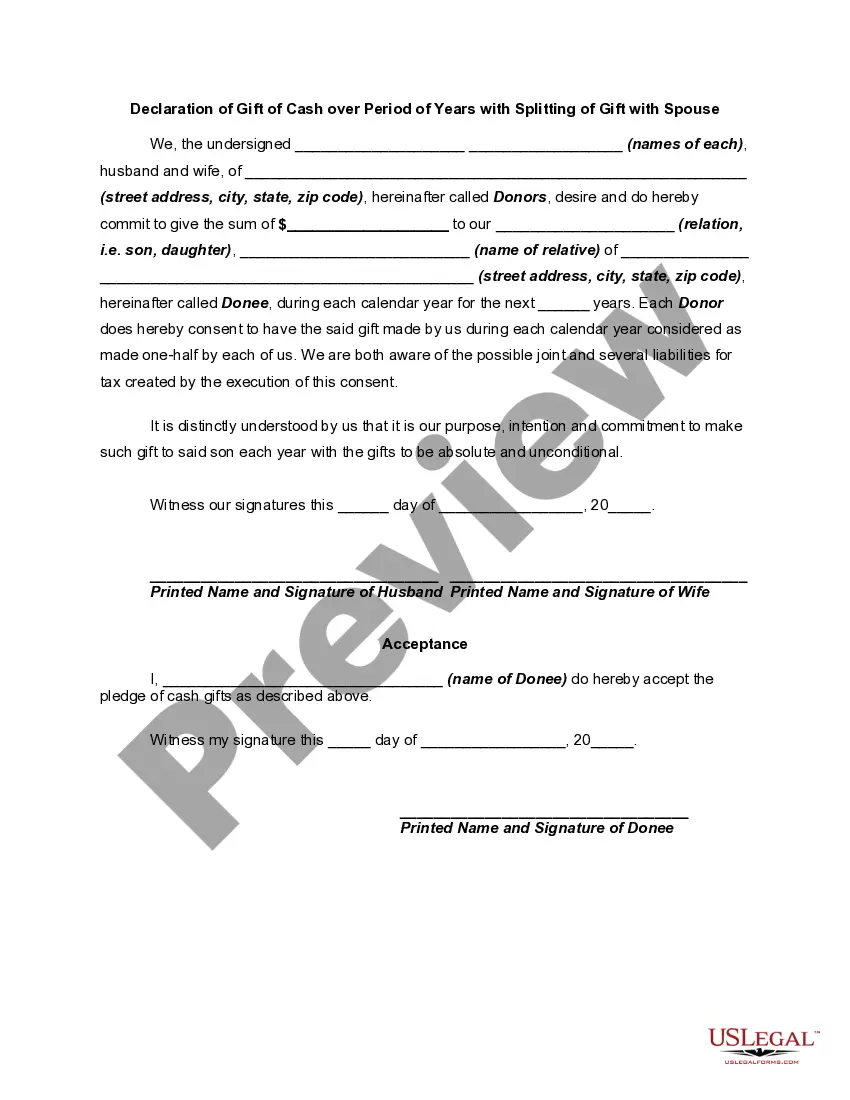

The North Dakota Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document that allows an individual in North Dakota to declare and gift cash over a specified period while also splitting the gift with their spouse. This declaration ensures that the gift is properly documented and that both the individual and their spouse are involved in the gifting process. Key elements of the North Dakota Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse include: 1. Gift Amount: The declaration specifies the amount of cash that the individual intends to gift over the designated period. This amount can vary based on the individual's personal preferences and financial capabilities. 2. Duration: The declaration outlines the period over which the cash gift will be made. It can be a fixed number of years or any other specified time frame agreed upon by the individual and their spouse. 3. Splitting of Gift: The declaration includes provisions for splitting the gift between the individual making the declaration and their spouse. This ensures that both parties are involved in the gifting process and have a share in the gift. 4. Tax Implications: The declaration may also address any potential tax implications associated with the gift. It is important to consult a tax advisor or attorney to understand the tax consequences and any applicable exemptions or regulations. Types of North Dakota Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse: 1. Revocable Declaration: This type of declaration allows the individual to modify or revoke the gift at any point before completion of the specified period. It provides flexibility and allows for adjustments based on changing circumstances. 2. Irrevocable Declaration: In contrast to the revocable declaration, an irrevocable declaration cannot be modified or revoked once it is made. This type of declaration ensures that the gift remains intact and cannot be changed. 3. Conditional Declaration: A conditional declaration sets certain conditions or requirements that must be met for the gift to be completed or split between the individual and their spouse. These conditions may include events such as the completion of a specific project or the attainment of a particular milestone. 4. Testamentary Declaration: This type of declaration is included in a person's will and takes effect upon their death. It allows the individual to include provisions for gifting cash over a specified period of time, with the splitting of the gift with their spouse. A proper North Dakota Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse provides a legal framework to ensure the smooth and transparent execution of the gift-giving process, while considering the individuals' and their spouse's interests.The North Dakota Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document that allows an individual in North Dakota to declare and gift cash over a specified period while also splitting the gift with their spouse. This declaration ensures that the gift is properly documented and that both the individual and their spouse are involved in the gifting process. Key elements of the North Dakota Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse include: 1. Gift Amount: The declaration specifies the amount of cash that the individual intends to gift over the designated period. This amount can vary based on the individual's personal preferences and financial capabilities. 2. Duration: The declaration outlines the period over which the cash gift will be made. It can be a fixed number of years or any other specified time frame agreed upon by the individual and their spouse. 3. Splitting of Gift: The declaration includes provisions for splitting the gift between the individual making the declaration and their spouse. This ensures that both parties are involved in the gifting process and have a share in the gift. 4. Tax Implications: The declaration may also address any potential tax implications associated with the gift. It is important to consult a tax advisor or attorney to understand the tax consequences and any applicable exemptions or regulations. Types of North Dakota Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse: 1. Revocable Declaration: This type of declaration allows the individual to modify or revoke the gift at any point before completion of the specified period. It provides flexibility and allows for adjustments based on changing circumstances. 2. Irrevocable Declaration: In contrast to the revocable declaration, an irrevocable declaration cannot be modified or revoked once it is made. This type of declaration ensures that the gift remains intact and cannot be changed. 3. Conditional Declaration: A conditional declaration sets certain conditions or requirements that must be met for the gift to be completed or split between the individual and their spouse. These conditions may include events such as the completion of a specific project or the attainment of a particular milestone. 4. Testamentary Declaration: This type of declaration is included in a person's will and takes effect upon their death. It allows the individual to include provisions for gifting cash over a specified period of time, with the splitting of the gift with their spouse. A proper North Dakota Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse provides a legal framework to ensure the smooth and transparent execution of the gift-giving process, while considering the individuals' and their spouse's interests.