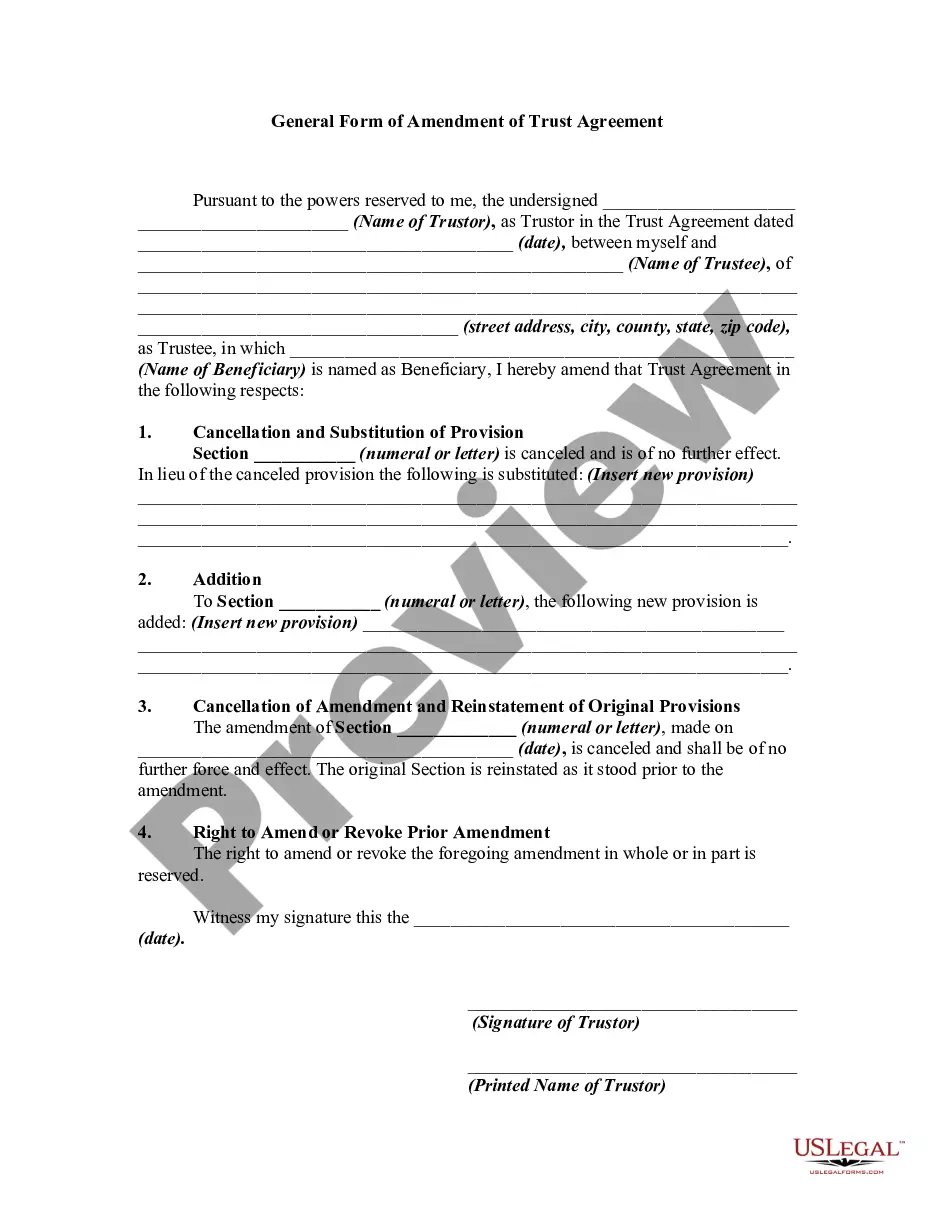

An A-B trust is a revocable living trust which divides into two trusts upon the death of the first spouse. This type of trust makes use of both the estate tax exemption ($3.5 million per person in 2009) and the marital deduction to make it so that no estate taxes are due upon the death of the first spouse. The B Trust is also known as the Bypass trust and it contains the amount of that years applicable exclusion amount. The A trust is the marital deduction trust which will typically contain both the surviving spouse's separate property and one half community property interests but also the residue of the deceased spouse's estate after the estate tax exemption has been utilized by the B trust. The use of an A-B trust ensures that both spouse's applicable exclusion amounts are effectively used, thereby doubling the amount of property which can pass to heirs free of Federal Estate Taxes.

North Dakota Marital Deduction Trust - Trust A and Bypass Trust B

Description

How to fill out Marital Deduction Trust - Trust A And Bypass Trust B?

Finding the correct legal document template can be a challenge.

Of course, there are numerous templates available online, but how do you locate the legal form you require.

Utilize the US Legal Forms website. The service offers a vast selection of templates, including the North Dakota Marital Deduction Trust - Trust A and Bypass Trust B, that you can utilize for business and personal needs.

You can view the form using the Review button and read the form description to confirm it is suitable for you.

- All of the forms are reviewed by professionals and comply with federal and state requirements.

- If you are currently registered, Log In to your account and click the Download button to get the North Dakota Marital Deduction Trust - Trust A and Bypass Trust B.

- Use your account to browse the legal forms you have previously ordered.

- Visit the My documents tab of your account to retrieve another copy of the document you need.

- If you are a new user of US Legal Forms, here are simple instructions that you can follow.

- First, ensure you have chosen the correct form for your specific region/area.

Form popularity

FAQ

Yes, a generation skipping trust typically needs to file a tax return. Like other trusts, it must report its income on Form 1041 if it generates taxable income. This filing requirement aligns with planning strategies that may include North Dakota Marital Deduction Trust - Trust A and Bypass Trust B to optimize tax outcomes across generations.

Yes, trusts often need to file tax returns. Generally, if the trust generates income, it is required to file Form 1041 with the IRS. Specifically, for a North Dakota Marital Deduction Trust - Trust A and Bypass Trust B, managing tax obligations properly is essential to maintain compliance and optimize benefits.

The key difference lies in how the trusts treat estate taxes and ownership of assets. A marital trust allows the surviving spouse to control the assets, deferring taxes until their death. In contrast, a bypass trust is designed to reduce estate taxes by allocating assets outside the surviving spouse's estate. Understanding these differences is vital when setting up your North Dakota Marital Deduction Trust - Trust A and Bypass Trust B, as each serves distinct purposes.

Yes, a bypass trust must file its own tax return if it generates income above a certain threshold. Unlike a marital trust, the assets in a bypass trust are not included in the surviving spouse’s estate. This can have significant tax implications both during the life of the trust and after the spouse's death. Understanding the requirements of a bypass trust is essential when managing your North Dakota Marital Deduction Trust - Trust A and Bypass Trust B.

One potential disadvantage of a marital trust is that, after the spouse’s death, the assets may be subject to estate taxes. This is because the assets are included in the survivor's estate. Additionally, the surviving spouse may have limited control over the trust assets, depending on how it is structured. Therefore, it is crucial to carefully consider these factors when utilizing the North Dakota Marital Deduction Trust - Trust A and Bypass Trust B.

A marital trust is a type of trust created to benefit a surviving spouse, allowing them to receive income from the trust during their lifetime. This arrangement defers estate taxes until the death of the surviving spouse, making it a key component of the North Dakota Marital Deduction Trust - Trust A and Bypass Trust B. It ensures that your spouse has financial security while also setting up a beneficial tax strategy.

While bypass trusts provide several benefits, there are also disadvantages to consider. One drawback is the potential complexity of managing the trust, which may require a professional trustee. Additionally, the North Dakota Marital Deduction Trust - Trust A and Bypass Trust B structure can lead to a more complicated estate plan, necessitating thorough documentation and ongoing management. It's important to weigh these factors for your unique financial situation.

Setting up a bypass trust involves a few important steps. First, you'll want to consult with an estate planning attorney who understands the North Dakota Marital Deduction Trust - Trust A and Bypass Trust B framework. The attorney will guide you through drafting a trust document, outlining the assets to be included, and naming a trustee. Once established, the trust must be funded, ensuring the intended assets are transferred into it for future management and distribution.

One key benefit of a bypass trust is its ability to minimize estate taxes for surviving heirs. By placing assets into a bypass trust, these assets are not included in the surviving spouse's estate, allowing for tax savings. Additionally, the North Dakota Marital Deduction Trust - Trust A and Bypass Trust B structure provides financial security and peace of mind, ensuring that loved ones receive their intended inheritances. This trust can also offer control over asset distribution across generations.

A bypass trust, often referred to as Trust B, is not the same as a marital trust or Trust A. While a marital trust allows assets to pass directly to a surviving spouse, a bypass trust bypasses the spouse, helping to protect assets from estate taxes. The North Dakota Marital Deduction Trust - Trust A and Bypass Trust B work together strategically to provide tax advantages and preserve wealth for heirs. Understanding these differences is crucial to making informed estate planning decisions.