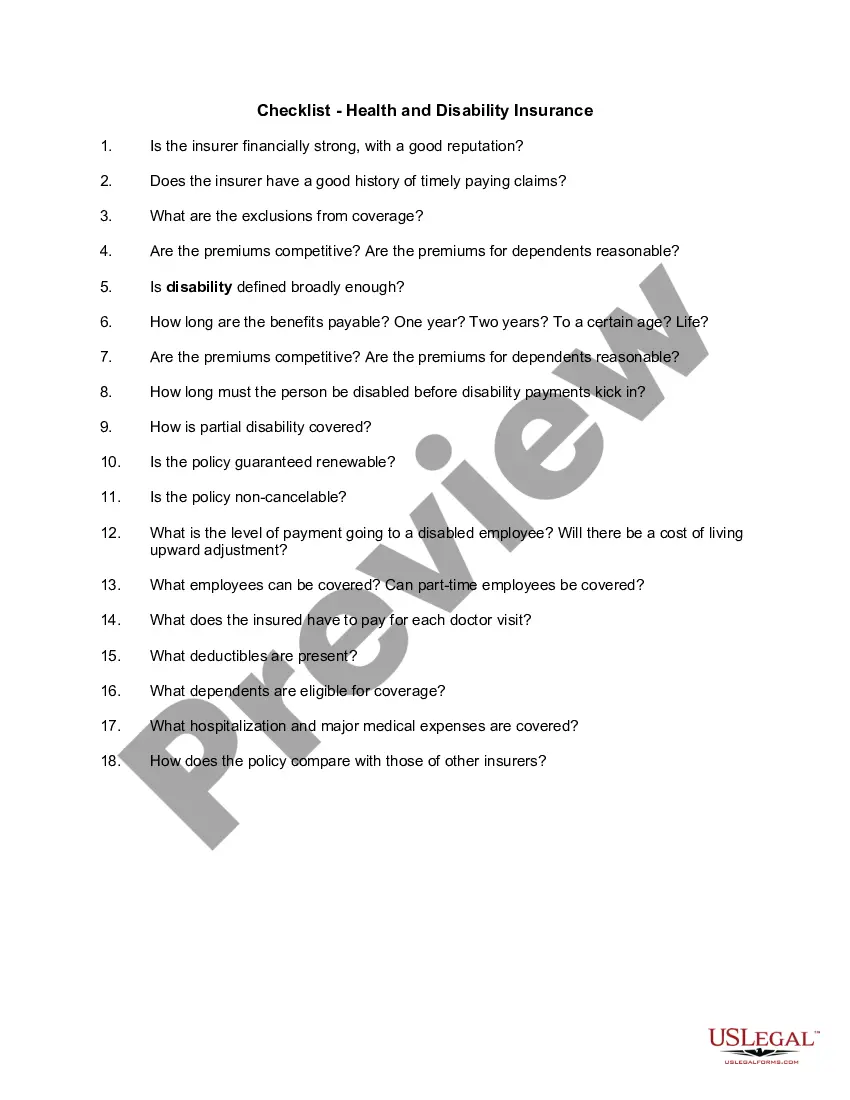

North Dakota Checklist — Health and Disability Insurance When it comes to safeguarding your health and protecting against unforeseen circumstances, having comprehensive health and disability insurance is crucial. In North Dakota, there are several important factors to consider while searching for an insurance plan that suits your specific needs and requirements. This comprehensive checklist will guide you through the key aspects to consider when exploring health and disability insurance options in North Dakota. 1. Evaluate your healthcare needs: Before diving into the insurance options available, it's essential to thoroughly assess your healthcare needs. Consider factors such as pre-existing conditions, medications, preferred doctors or specialists, and any potential anticipated medical expenses. 2. Coverage options: North Dakota provides various health insurance options to cater to different individuals and families. These include individual and family plans, group coverage through employers, Medicaid for those qualifying on income basis, and the Children's Health Insurance Program (CHIP) for children from low-income families. 3. Network of Providers: Look into the insurance networks available in North Dakota and check if your preferred healthcare providers, hospitals, and specialists are included. Ensure that the plan offers ample options in your local area as well as neighboring regions if you often need to travel for medical care. 4. Coverage for pre-existing conditions: It's crucial to check if the insurance plan you're considering adequately covers any pre-existing conditions you may have. North Dakota follows federal regulations, ensuring that pre-existing conditions are covered in all health insurance plans. 5. Prescription medication coverage: Take into account your regular prescription medications and ensure the insurance plan provides adequate coverage for them. Evaluate co-pays, preferred pharmacies, and any limitations or exclusions that may apply. 6. Out-of-pocket costs: Carefully review and compare deductibles, co-payments, and coinsurance rates across different insurance plans. Assess how these out-of-pocket costs may add up over time and determine which plan provides the most reasonable cost-sharing options for you. 7. Disability insurance options: In addition to health insurance, consider disability insurance coverage to protect your income in the event of a disabling illness or injury. Disability insurance safeguards your financial stability by providing a percentage of your income if you are unable to work due to disability. 8. Supplemental insurance coverage: Depending on your specific needs, you may want to consider supplemental insurance coverage, such as dental, vision, or long-term care insurance. Evaluate your long-term goals and any potential gaps in coverage to determine if additional policies are necessary. 9. Check insurer ratings: Before finalizing an insurance provider, research their financial stability and customer satisfaction ratings. This will help ensure the company is reliable, has a strong track record, and provides excellent customer service. By following this North Dakota Checklist for Health and Disability Insurance, you can make an informed decision and select a plan that best fits your healthcare needs and financial situation. Remember to regularly review and update your coverage as your circumstances evolve to ensure ongoing protection and peace of mind.

North Dakota Checklist - Health and Disability Insurance

Description

How to fill out North Dakota Checklist - Health And Disability Insurance?

US Legal Forms - among the largest libraries of lawful forms in the USA - provides a wide array of lawful document layouts you are able to download or print out. Making use of the web site, you will get a large number of forms for business and individual uses, sorted by types, states, or key phrases.You will discover the newest variations of forms such as the North Dakota Checklist - Health and Disability Insurance in seconds.

If you currently have a registration, log in and download North Dakota Checklist - Health and Disability Insurance from the US Legal Forms library. The Down load option will show up on every single form you perspective. You have access to all earlier acquired forms from the My Forms tab of the bank account.

If you wish to use US Legal Forms the first time, here are easy recommendations to help you started out:

- Make sure you have picked out the right form to your town/region. Click on the Review option to analyze the form`s information. Browse the form description to actually have selected the proper form.

- When the form does not fit your specifications, use the Search field near the top of the display to find the one that does.

- When you are happy with the shape, confirm your decision by simply clicking the Acquire now option. Then, opt for the rates plan you favor and provide your accreditations to sign up for an bank account.

- Process the transaction. Make use of bank card or PayPal bank account to perform the transaction.

- Find the file format and download the shape on your own device.

- Make modifications. Load, revise and print out and sign the acquired North Dakota Checklist - Health and Disability Insurance.

Every design you put into your account lacks an expiration day and is also your own property forever. So, if you wish to download or print out yet another backup, just go to the My Forms portion and click around the form you want.

Obtain access to the North Dakota Checklist - Health and Disability Insurance with US Legal Forms, by far the most substantial library of lawful document layouts. Use a large number of expert and status-certain layouts that fulfill your company or individual requirements and specifications.