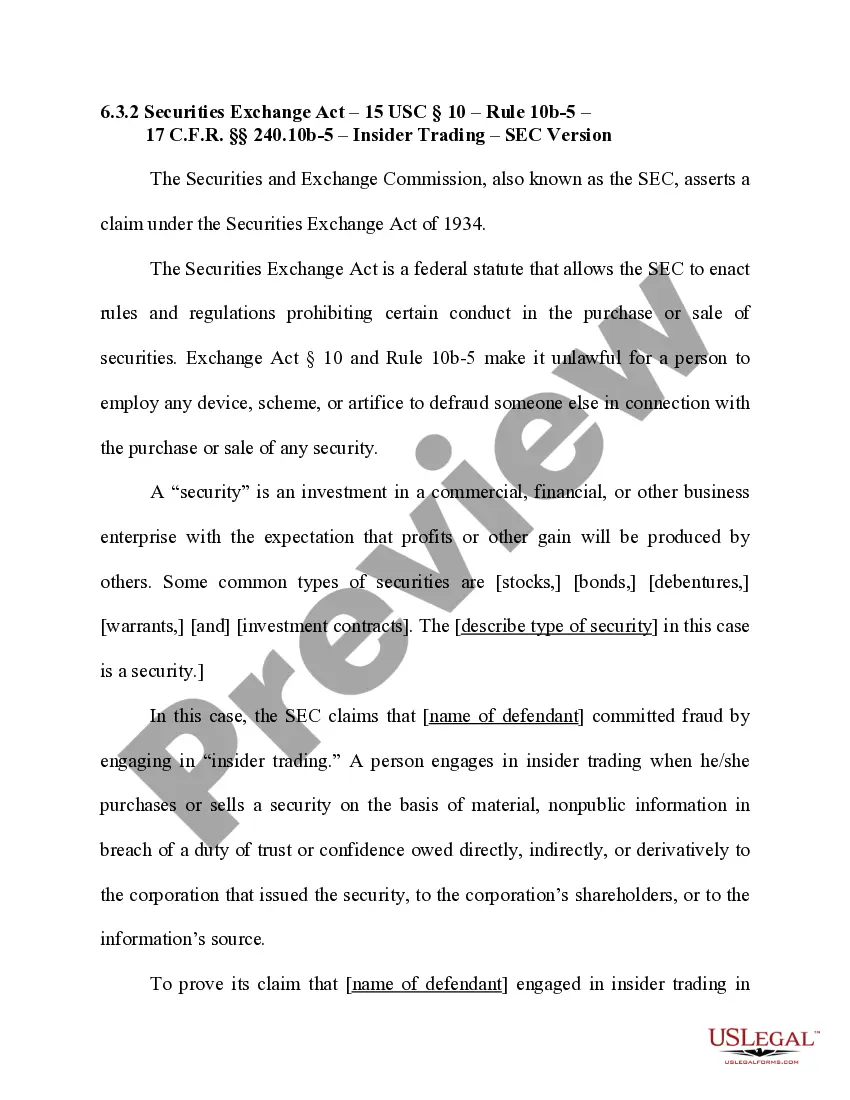

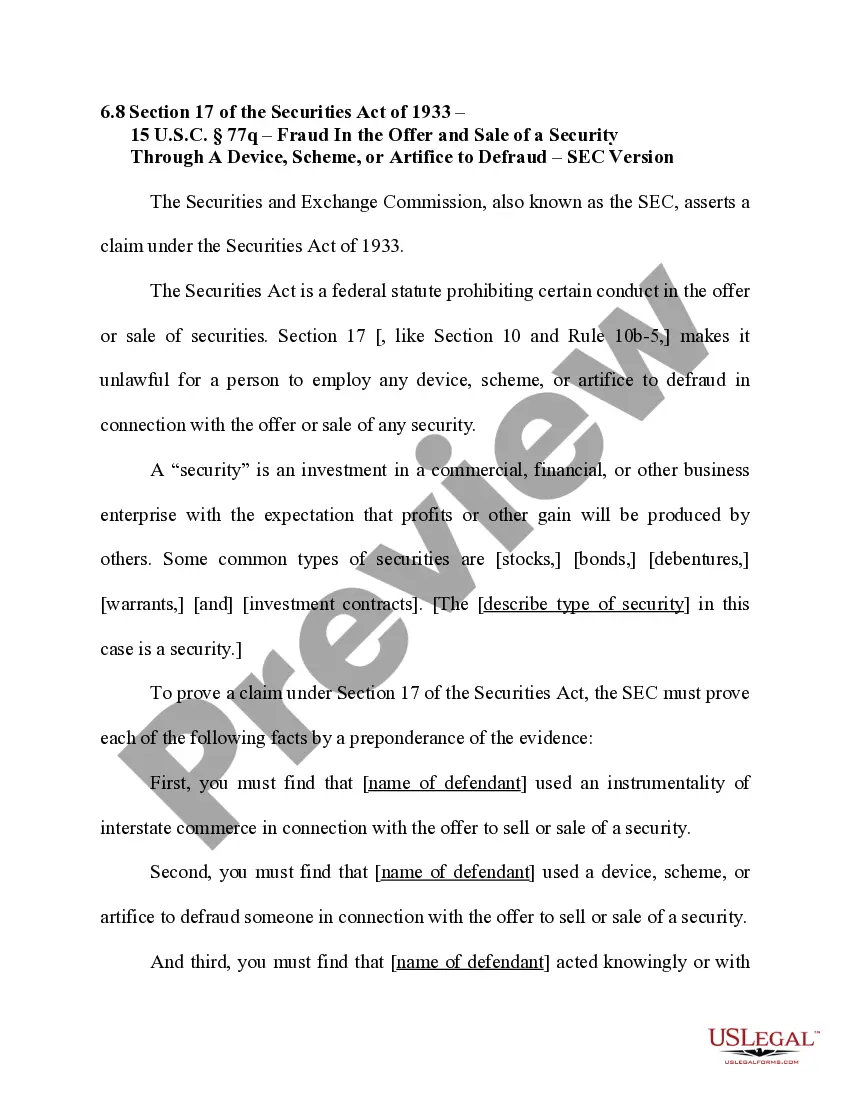

North Dakota Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading

Description

How to fill out Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading?

You can spend time on the Internet attempting to find the authorized papers web template that meets the federal and state demands you need. US Legal Forms gives a huge number of authorized types which are reviewed by pros. You can actually download or produce the North Dakota Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading from our support.

If you already possess a US Legal Forms accounts, you can log in and click on the Obtain button. After that, you can full, modify, produce, or indication the North Dakota Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading. Each authorized papers web template you acquire is the one you have eternally. To have an additional backup of the purchased form, proceed to the My Forms tab and click on the related button.

If you work with the US Legal Forms web site the first time, stick to the straightforward directions under:

- Initial, make certain you have selected the proper papers web template to the area/town of your choice. See the form information to ensure you have picked out the correct form. If available, make use of the Preview button to appear throughout the papers web template too.

- If you want to get an additional edition of the form, make use of the Lookup discipline to discover the web template that fits your needs and demands.

- Once you have identified the web template you desire, click on Acquire now to move forward.

- Find the costs prepare you desire, type your references, and register for your account on US Legal Forms.

- Full the transaction. You should use your charge card or PayPal accounts to pay for the authorized form.

- Find the file format of the papers and download it in your system.

- Make adjustments in your papers if needed. You can full, modify and indication and produce North Dakota Jury Instruction - 4.4.1 Rule 10(b) - 5(a) Device, Scheme Or Artifice To Defraud Insider Trading.

Obtain and produce a huge number of papers web templates making use of the US Legal Forms site, which provides the greatest selection of authorized types. Use professional and state-distinct web templates to tackle your organization or person requires.

Form popularity

FAQ

The judge reads the instructions to the jury. This is commonly referred to as the judge's charge to the jury. In giving the instructions, the judge will state the issues in the case and define any terms or words that may not be familiar to the jurors.

Another example of reasonable doubt in a DUI case is if the arresting officer failed to follow proper procedure or they didn't have probable cause. If the defense can demonstrate that there were flaws or any form of negligence in the arrest, this may be enough to cast reasonable doubt on the guilt of the accused.

(1) Members of the jury, now it is time for me to instruct you about the law you must follow in deciding this case. (2) I will start by explaining your duties and the general rules that apply in every criminal case. (3) Then I will explain the elements of the crimes that the defendant is accused of committing.

Jury instructions should ideally be brief, concise, non-repetitive, relevant to the case's details, understandable to the average juror, and should correctly state the law without misleading the jury or inviting unnecessary speculation.

The instructions are intended to describe trial procedures and duties in a manner that makes the legal process comprehensible to jurors, and to correctly state the law so that the jurors can apply it to the facts as they determine them to be.

Model Jury Instruction - A form jury instruction usually approved by a state bar association or similar group regarding matters arising in a typical case. Courts usually accept model jury instructions as authoritative.

It is not required that the government prove guilt beyond all possible doubt. A reasonable doubt is a doubt based upon reason and common sense and is not based purely on speculation. It may arise from a careful and impartial consideration of all the evidence, or from lack of evidence.

Not all circuits have published jury instructions: the Second and Fourth Circuits do not. The United States Court of Appeals for the Federal Circuit is a unique court in that it has nationwide jurisdiction in a variety of subject areas. Appeals are heard by panels comprised of three judges.

In a criminal case, the prosecution bears the burden of proving that the defendant is guilty beyond all reasonable doubt. This means that the prosecution must convince the jury that there is no other reasonable explanation that can come from the evidence presented at trial.

Reasonable doubt is insufficient evidence that prevents a judge or jury from convicting a defendant of a crime. If it cannot be proved without a doubt that a defendant in a criminal case is guilty, then that person should not be convicted.