This form is a business type form that is formatted to allow you to complete the form using Adobe Acrobat or Word. The word files have been formatted to allow completion by entry into fields. Some of the forms under this category are rather simple while others are more complex. The formatting is worth the small cost.

North Dakota Balance Sheet Deposits

Category:

State:

Multi-State

Control #:

US-122-AZ

Format:

Word;

PDF;

Rich Text

Instant download

Description

How to fill out Balance Sheet Deposits?

You can invest hours online searching for the legal document template that satisfies the state and federal requirements you desire.

US Legal Forms offers a vast array of legal forms that are reviewed by professionals.

It is easy to download or print the North Dakota Balance Sheet Deposits from your service.

If you wish to locate another version of your form, use the Search section to find the template that meets your needs and desires. Once you have found the template you want, click Buy now to proceed. Choose the pricing plan you prefer, enter your credentials, and create an account on US Legal Forms. Complete the purchase. You can use your credit card or PayPal account to acquire the legal form. Select the format of your document and download it to your device. Make changes to your document if necessary. You can complete, amend, sign, and print the North Dakota Balance Sheet Deposits. Obtain and print numerous document templates using the US Legal Forms site, which provides the most comprehensive collection of legal forms. Utilize professional and state-specific templates to address your business or personal requirements.

- If you already have a US Legal Forms account, you can Log In and click on the Download button.

- After that, you can complete, modify, print, or sign the North Dakota Balance Sheet Deposits.

- Every legal document template you receive is yours permanently.

- To obtain an additional copy of a purchased form, navigate to the My documents tab and click on the relevant button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the appropriate document template for the state/city of your choice.

- Check the form description to confirm you have chosen the correct form.

- If available, use the Preview button to review the document template as well.

Form popularity

FAQ

The short answer is yes a term deposit is, indeed, an asset. Regardless that the funds are locked away for a fixed period, when it comes to the balance sheet, it's considered an asset.

Deposits as AssetsWhen a business places a security deposit that is, it gives someone else money to hold against possible future charges the deposit is listed as an asset on its balance sheet.

The deposit itself is a liability owed by the bank to the depositor. Bank deposits refer to this liability rather than to the actual funds that have been deposited. When someone opens a bank account and makes a cash deposit, he surrenders the legal title to the cash, and it becomes an asset of the bank.

An Inside Look at Bank of America Corporation (BAC) It may appear counterintuitive that the deposits are in red and loans are in green. However, for a bank, a deposit is a liability on its balance sheet whereas loans are assets because the bank pays depositors interest, but earns interest income from loans.

Fixed deposit that is for a term of one year is termed as current asset, while fixed deposit having a term of more than one year is non-current asset. Also read: Intangible Assets.

Cash, stocks, bonds, mutual funds, and bank deposits are all are examples of financial assets.

Deposits is a current liability account in the general ledger, in which is stored the amount of funds paid by customers in advance of a product or service delivery. These funds are essentially down payments.

Deposit Assets means cash, Short-Term Money Market Instruments and U.S.

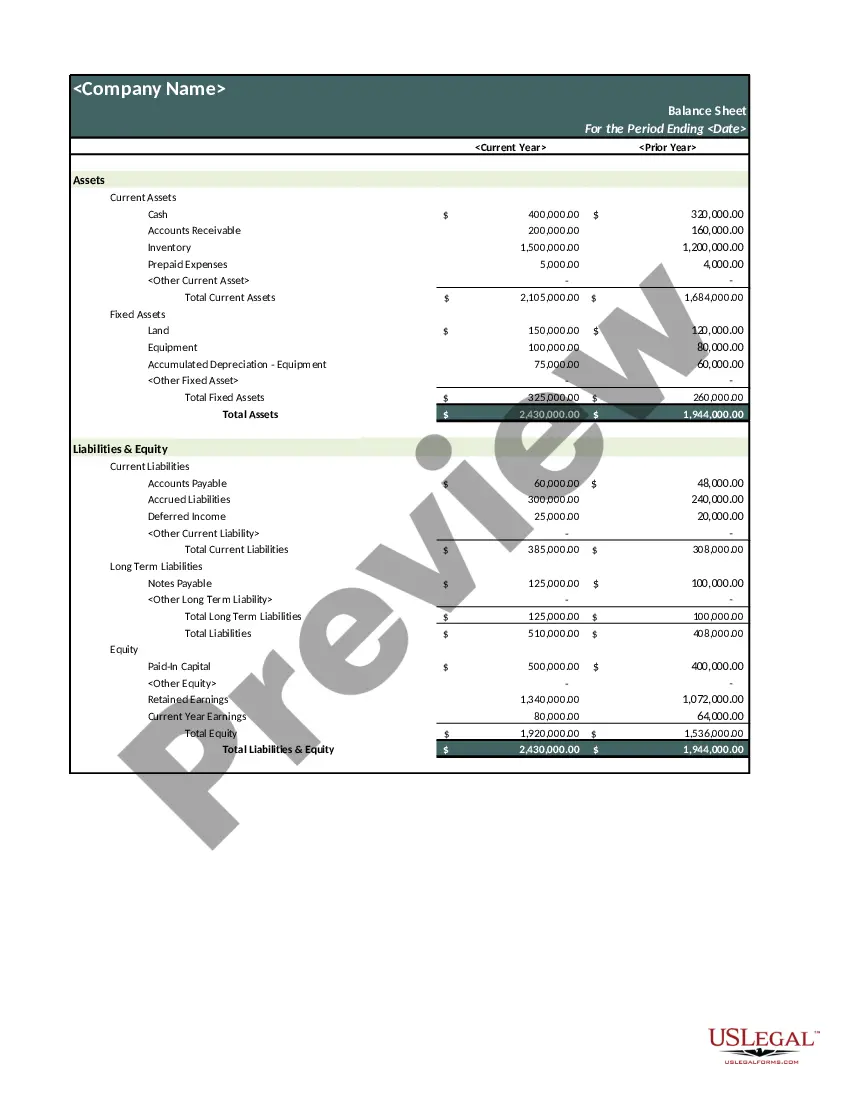

The volume of business of a bank is included in its balance sheet for both assets (lending) and liabilities (customer deposits or other financial instruments).

The short answer is yes a term deposit is, indeed, an asset. Regardless that the funds are locked away for a fixed period, when it comes to the balance sheet, it's considered an asset.