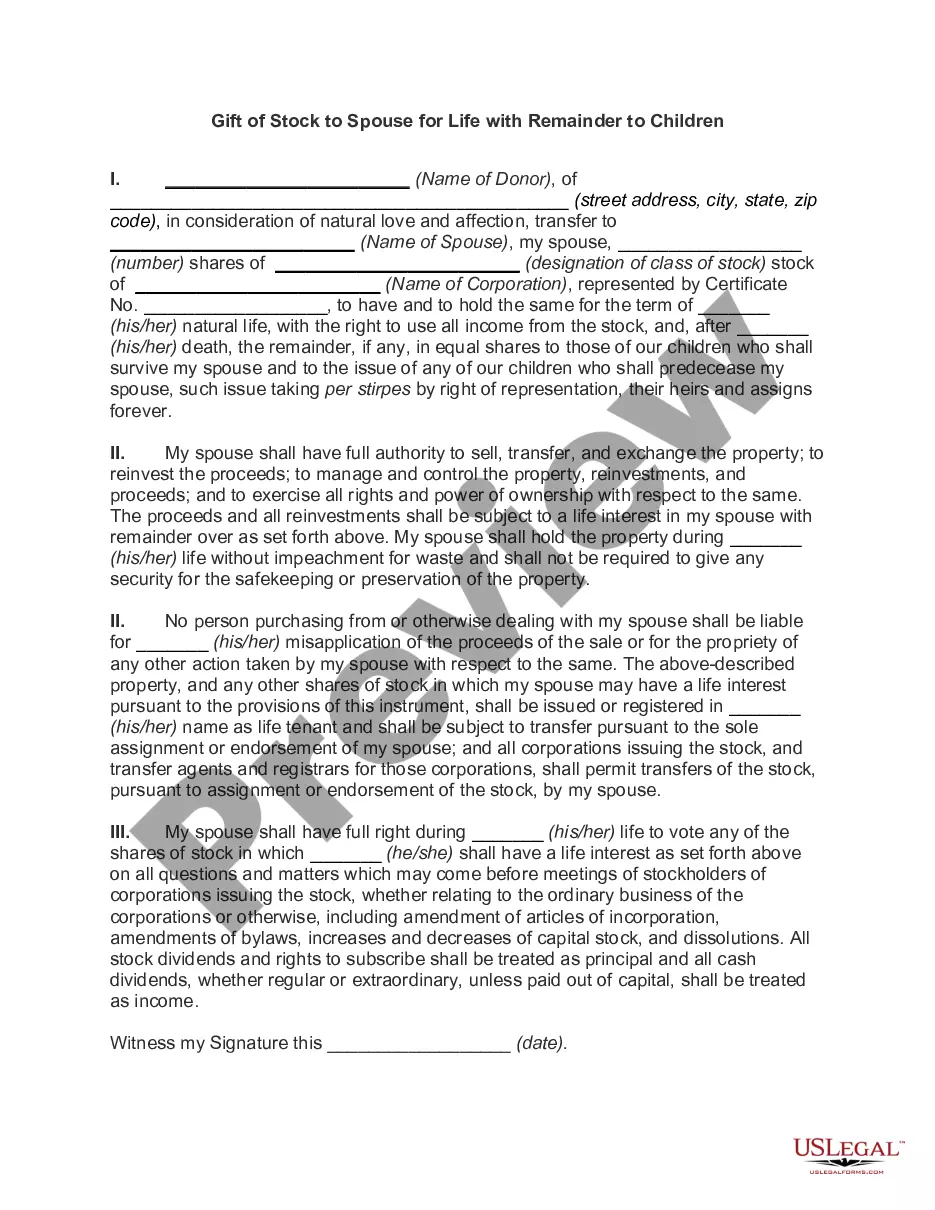

North Dakota Gift of Stock to Spouse for Life with Remainder to Children is a type of estate planning arrangement that allows an individual to transfer ownership of stock assets to their spouse for their lifetime, while ensuring that the remaining stock is passed on to their children upon the spouse's death. This arrangement offers potential tax benefits and flexibility in managing an individual's estate. Key benefits of a North Dakota Gift of Stock to Spouse for Life with Remainder to Children include: 1. Estate Tax Reduction: By transferring the stock assets to a spouse, the initial value of the stock is excluded from the individual's taxable estate, potentially reducing estate taxes. 2. Lifetime Use: The spouse who receives the stock has the right to use and benefit from it during their lifetime, while still having the comfort of knowing that the remaining stock will pass to the children. 3. Capital Gains Tax Savings: When the spouse eventually transfers the stock to the children, the cost basis for capital gains tax purposes is "stepped-up" to the value of the stock on the spouse's date of death, potentially reducing the tax liability on any gains. 4. Control: The individual creating the gift retains control over the stock assets during their lifetime, and can still manage or make changes to the stocks as they deem appropriate. It's important to note that there are various types of North Dakota Gift of Stock to Spouse for Life with Remainder to Children arrangements, each with their own specifics and features. Some common variations include: 1. Charitable Remainder Trust (CRT): An individual can establish a CRT, where the remainder interest in the stock assets will pass to a qualified charity upon the spouse's death. This can provide additional tax benefits, such as income tax deductions, while supporting charitable causes. 2. Qualified Terminable Interest Property (TIP) Trust: This type of trust allows the creator to provide for their spouse while ensuring that the remaining stock assets will pass to their children. It offers flexibility and control over the distribution of assets, while potentially reducing estate taxes. 3. Testamentary Trust: In this arrangement, the gift of stock to the spouse is provided through instructions in the individual's Last Will and Testament. The testamentary trust is created upon the individual's death and allows for the management and distribution of the stock assets. 4. Irrevocable Life Insurance Trust (IIT): While not directly related to stock assets, an IIT can be utilized in combination with the North Dakota Gift of Stock to Spouse for Life with Remainder to Children to provide liquidity for payment of estate taxes or supplement the inheritance of children. Overall, a North Dakota Gift of Stock to Spouse for Life with Remainder to Children arrangement is a strategic and flexible estate planning tool that can provide financial security for both a spouse and children, while minimizing potential tax liabilities. It is essential to consult with an experienced estate planning attorney or financial advisor to determine the best approach based on individual circumstances.

North Dakota Gift of Stock to Spouse for Life with Remainder to Children

Description

How to fill out North Dakota Gift Of Stock To Spouse For Life With Remainder To Children?

You can spend hours on the Internet trying to find the authorized record template that suits the state and federal needs you will need. US Legal Forms offers thousands of authorized types that happen to be reviewed by pros. It is simple to download or print the North Dakota Gift of Stock to Spouse for Life with Remainder to Children from our assistance.

If you already possess a US Legal Forms accounts, you may log in and then click the Down load button. Following that, you may full, revise, print, or indication the North Dakota Gift of Stock to Spouse for Life with Remainder to Children. Each authorized record template you purchase is yours for a long time. To acquire one more copy of the acquired form, go to the My Forms tab and then click the corresponding button.

If you are using the US Legal Forms site the very first time, adhere to the straightforward guidelines beneath:

- First, be sure that you have chosen the best record template for your area/metropolis of your choice. Read the form outline to ensure you have picked out the correct form. If available, utilize the Review button to look with the record template also.

- If you would like locate one more model from the form, utilize the Look for industry to discover the template that suits you and needs.

- Once you have identified the template you want, simply click Purchase now to proceed.

- Find the pricing strategy you want, key in your qualifications, and register for a free account on US Legal Forms.

- Comprehensive the financial transaction. You can use your charge card or PayPal accounts to pay for the authorized form.

- Find the file format from the record and download it to the device.

- Make alterations to the record if necessary. You can full, revise and indication and print North Dakota Gift of Stock to Spouse for Life with Remainder to Children.

Down load and print thousands of record templates making use of the US Legal Forms website, which provides the greatest assortment of authorized types. Use specialist and express-particular templates to handle your small business or individual demands.

Form popularity

FAQ

Gift Tax. North Dakota does not have a gift tax.

According to federal tax law, if an individual makes a gift of property within 3 years of the date of their death, the value of that gift is included in the value of their gross estate. The gross estate is the dollar value of their estate at the time of their death.

Exclusions. The annual exclusion for gifts is $11,000 (2004-2005), $12,000 (2006-2008), $13,000 (2009-2012) and $14,000 (2013-2017). In 2018, 2019, 2020, and 2021, the annual exclusion is $15,000. In 2022, the annual exclusion is $16,000.

The three-year rule prevents individuals from gifting assets to their descendants or other parties once death is imminent in an attempt to avoid estate taxes.

If there is a spouse and a child or grandchild, the spouse inherits all of the community property and one-half of the separate property. If there is a spouse and multiple children, the spouse inherits all of the community property and one-third of the separate property.

Yes, inheritor is someone other than decedent's spouse, descendant, descendant's spouse, ancestor, stepchild, stepparent or sibling. Washington, D.C. California, Florida, Virginia, and Wisconsin do not have estate, gift or inheritance tax.

The three-year rule states that assets gifted within three years of a person's death must be included in the value of their estate for tax purposes. The three-year rule states that assets gifted within three years of a person's death must be included in the value of their estate for tax purposes.

Under federal tax law, estate holders are permitted to give away up to $14,000 a year per person tax-free. When a married couple makes a gift, the exclusion increases to $28,000. The gift can take any form, cash, an interest in property, or even a business.

Goods that are subject to sales tax in North Dakota include physical property, like furniture, home appliances, and motor vehicles. Prescription medicine, groceries, and gasoline are all tax-exempt.

According to federal tax law, if an individual makes a gift of property within 3 years of the date of their death, the value of that gift is included in the value of their gross estate. The gross estate is the dollar value of their estate at the time of their death.