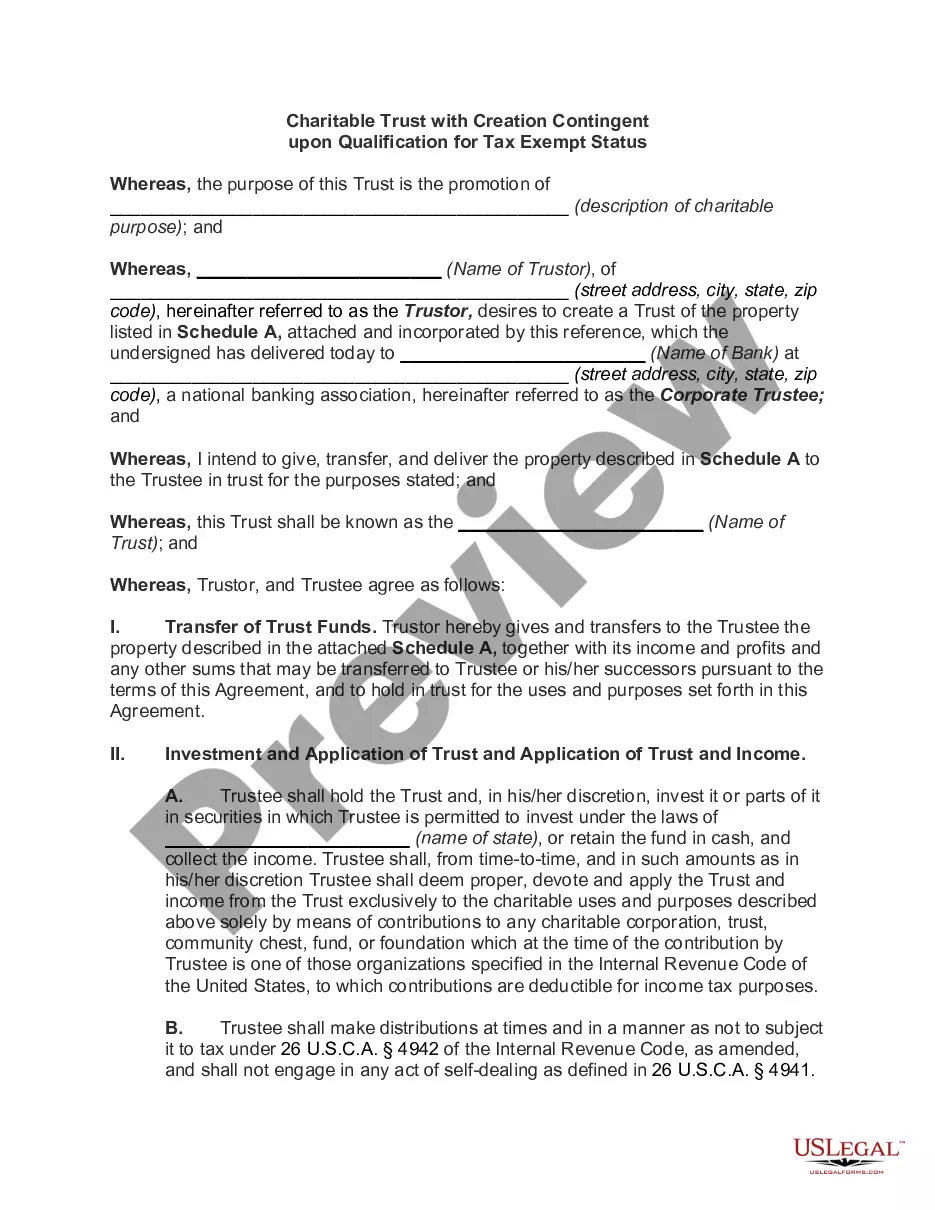

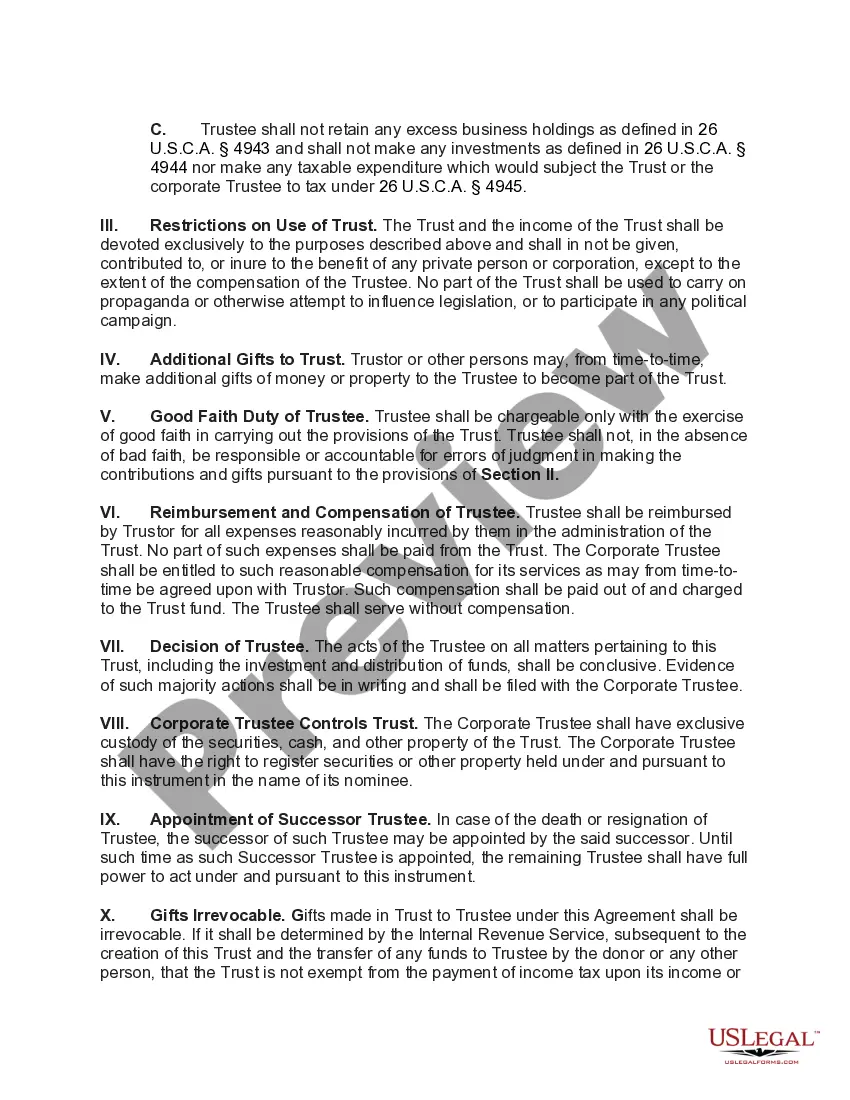

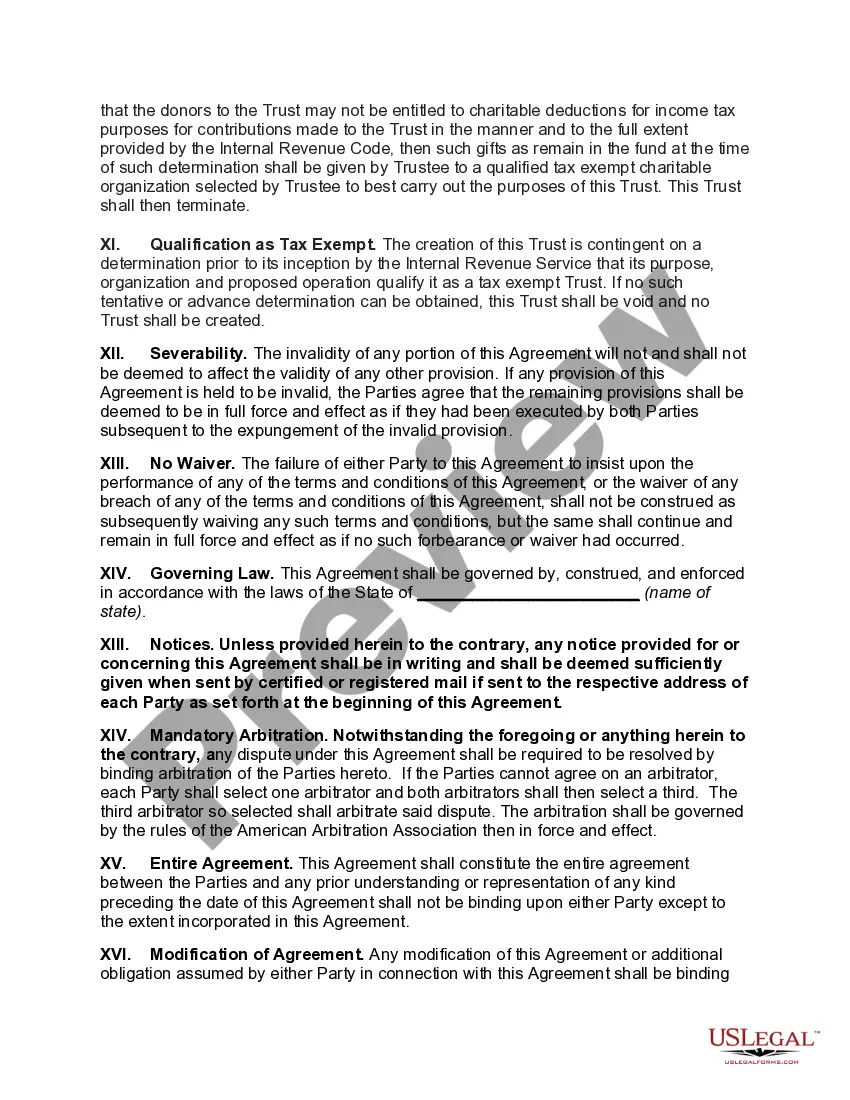

North Dakota Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status: A North Dakota Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status is a legal arrangement where a person or organization establishes a trust fund in North Dakota for charitable purposes. The creation of such a trust is contingent upon the trust qualifying for tax-exempt status from the Internal Revenue Service (IRS). By creating a North Dakota Charitable Trust with a requirement for tax-exempt status, the individual or organization aims to ensure that any income or assets placed in the trust are used exclusively for charitable purposes, ultimately benefiting the community or specific causes. To qualify for tax-exempt status, the trust must meet the eligibility criteria specified by the IRS. This typically involves adhering to specific guidelines and restrictions on the trust's purpose, activities, governance, and financial management. The IRS scrutinizes the trust's application to determine if it meets the requirements set forth in the Internal Revenue Code. There are different types of North Dakota Charitable Trusts created with the condition of qualifying for tax-exempt status. Some common types include: 1. Charitable Remainder Trust (CRT): A CRT allows the donor to provide for one or more beneficiaries while ultimately benefiting a charitable organization. This type of trust provides income payments to beneficiaries for a specific period or their lifetime before transferring the remaining assets to the charity. 2. Charitable Lead Trust (CLT): Unlike a CRT, a CLT provides income payments to a charitable organization during a predetermined period before the remainder is returned to the donor or designated beneficiaries. This allows individuals to support a charity while eventually passing appreciating assets to their loved ones. 3. Pooled Income Fund (PIF): A PIF combines funds from multiple donors into a single trust, managed by a charitable organization. Income generated from the pooled funds is distributed amongst the donors based on their contribution percentage. Upon the death of a donor, their share is transferred to the charity. 4. Donor-Advised Fund (DAF): A DAF enables donors to make charitable contributions to a sponsoring organization that manages the fund. The donor advises the organization on the distribution of funds to various charitable causes or organizations. 5. Private Foundation: Private foundations are independent entities created by an individual, family, or corporation. They provide grants and support charitable activities. To maintain tax-exempt status, private foundations must comply with strict rules regarding their charitable distributions and investments. Creating a North Dakota Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status ensures the trust's assets are utilized solely for charitable purposes and provides tax advantages to both the donor and the designated charitable organization. It is crucial to seek legal and financial advice to navigate the complexities of establishing such a trust and ensuring compliance with all IRS regulations.

North Dakota Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status

Description

How to fill out North Dakota Charitable Trust With Creation Contingent Upon Qualification For Tax Exempt Status?

US Legal Forms - one of the biggest libraries of lawful types in the USA - offers an array of lawful papers templates you may acquire or print. Using the website, you may get a large number of types for enterprise and person uses, categorized by categories, states, or search phrases.You can get the newest variations of types like the North Dakota Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status within minutes.

If you currently have a membership, log in and acquire North Dakota Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status in the US Legal Forms collection. The Download button can look on every kind you view. You have access to all in the past acquired types in the My Forms tab of the bank account.

If you wish to use US Legal Forms the first time, allow me to share simple instructions to help you get started:

- Be sure you have selected the right kind to your town/state. Click on the Review button to review the form`s information. Browse the kind information to actually have selected the appropriate kind.

- If the kind doesn`t suit your requirements, utilize the Lookup area on top of the screen to discover the the one that does.

- In case you are pleased with the form, verify your selection by simply clicking the Get now button. Then, select the pricing strategy you want and supply your credentials to register for an bank account.

- Approach the transaction. Use your Visa or Mastercard or PayPal bank account to complete the transaction.

- Select the file format and acquire the form on your own system.

- Make adjustments. Fill out, change and print and signal the acquired North Dakota Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status.

Each design you included in your bank account lacks an expiry time and it is yours eternally. So, in order to acquire or print one more duplicate, just go to the My Forms segment and click on the kind you require.

Get access to the North Dakota Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status with US Legal Forms, one of the most substantial collection of lawful papers templates. Use a large number of specialist and express-particular templates that meet up with your business or person needs and requirements.