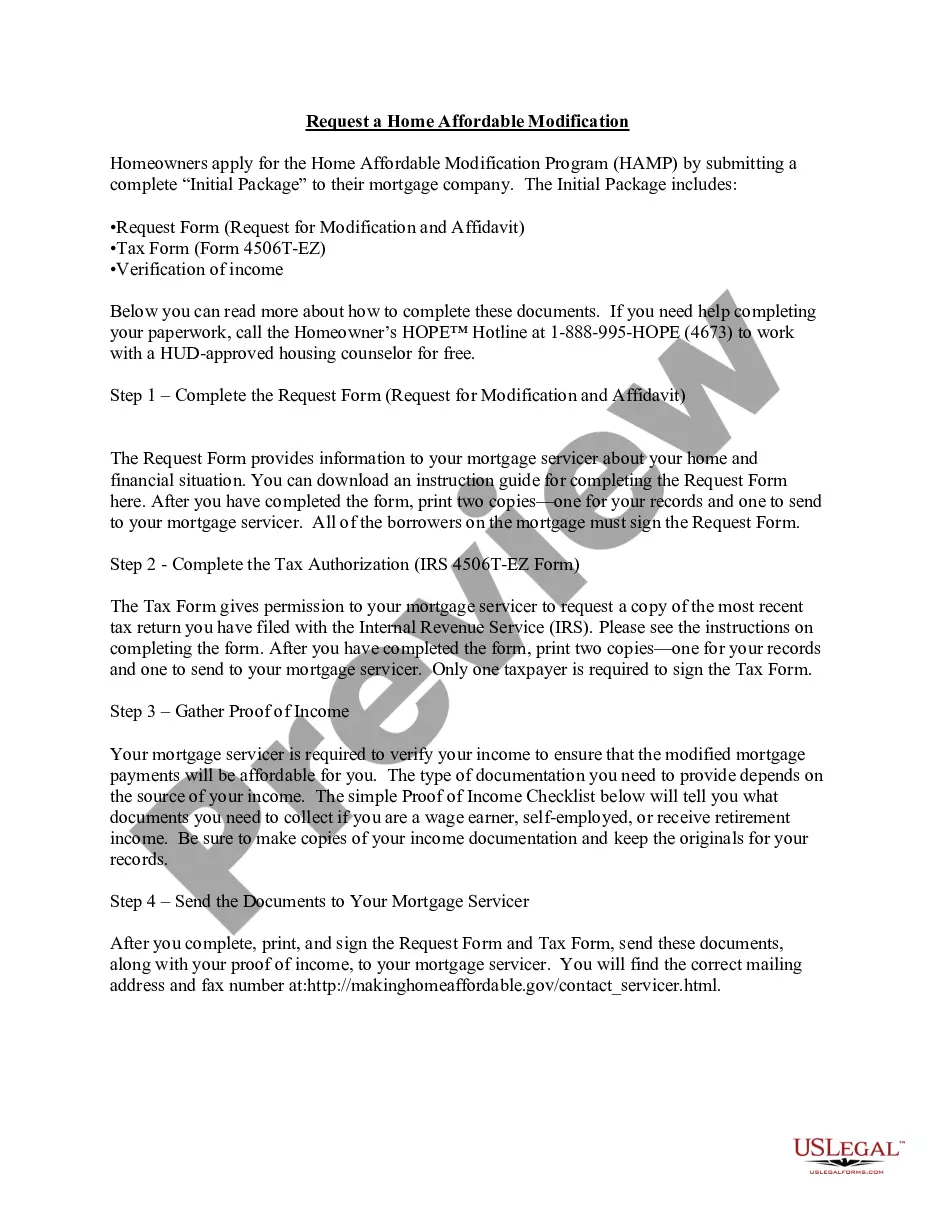

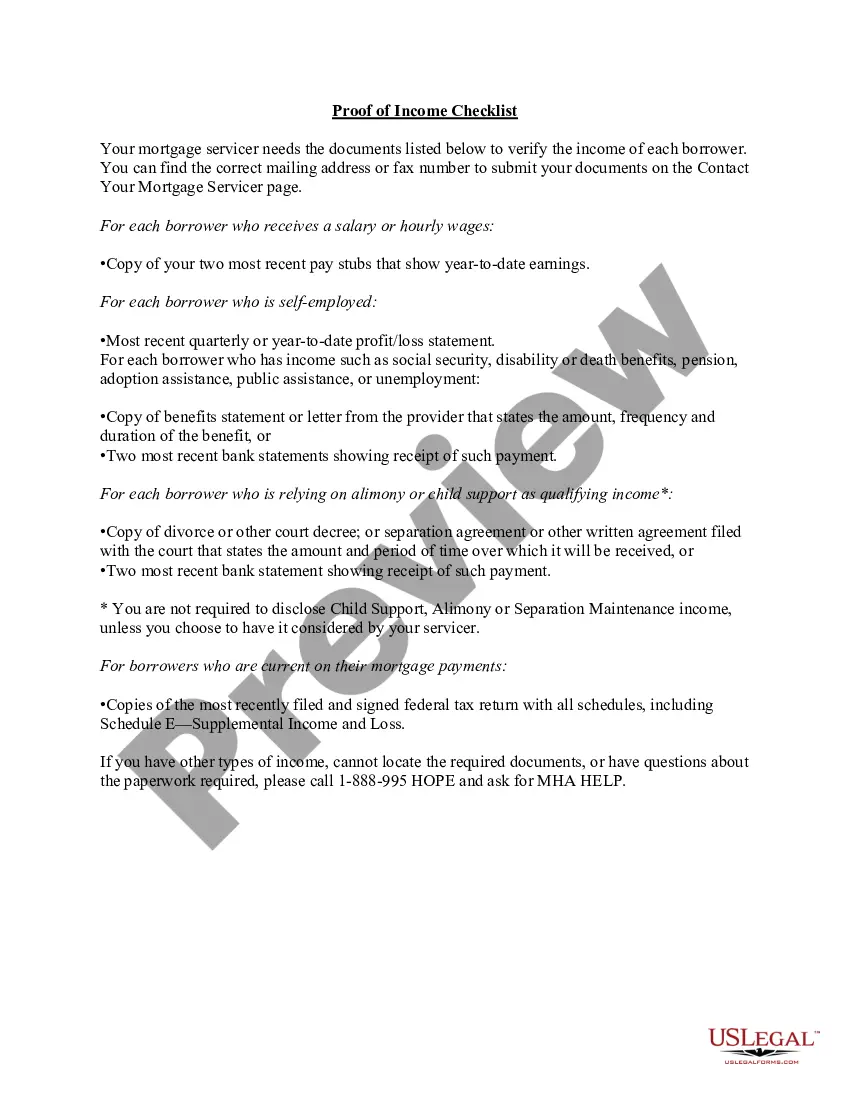

North Dakota How to Request a Home Affordable Modification Guide

Description

How to fill out North Dakota How To Request A Home Affordable Modification Guide?

Have you been in a position where you will need documents for both company or personal reasons almost every time? There are a variety of authorized file themes available on the Internet, but discovering ones you can trust is not simple. US Legal Forms provides a large number of develop themes, much like the North Dakota How to Request a Home Affordable Modification Guide, that happen to be composed to meet state and federal requirements.

In case you are currently knowledgeable about US Legal Forms web site and get an account, just log in. Following that, it is possible to download the North Dakota How to Request a Home Affordable Modification Guide format.

If you do not provide an account and need to start using US Legal Forms, abide by these steps:

- Find the develop you need and ensure it is for that proper city/county.

- Utilize the Review option to analyze the form.

- Read the explanation to ensure that you have chosen the right develop.

- When the develop is not what you are trying to find, make use of the Lookup discipline to discover the develop that fits your needs and requirements.

- If you discover the proper develop, just click Get now.

- Pick the prices strategy you want, submit the necessary information to produce your bank account, and purchase the order with your PayPal or bank card.

- Select a hassle-free document formatting and download your version.

Find every one of the file themes you possess purchased in the My Forms menu. You can obtain a more version of North Dakota How to Request a Home Affordable Modification Guide at any time, if possible. Just click on the necessary develop to download or produce the file format.

Use US Legal Forms, probably the most extensive assortment of authorized forms, to save lots of some time and steer clear of mistakes. The support provides professionally made authorized file themes that can be used for a selection of reasons. Generate an account on US Legal Forms and commence generating your life a little easier.

Form popularity

FAQ

Tips for Getting a Mortgage Modification ApprovedApply as soon as you can.Pay attention to detail.Send in all items requested by your loan servicers.Hold on to all information provided by your servicer.Put together a new monthly budget.Write a hardship letter and put careful thought into it.More items...?

Second Lien Modification Program or (2MP) was developed by U.S. Treasury Department to help homeowners with the second mortgage on their property who already modified their first mortgage with the Home Affordable Modification Program (HAMP) but continue to face financial difficulties.

FHA-Home Affordable Modification Program (FHA-HAMP) Allows homeowners to modify their FHA-insured mortgages to reduce monthly mortgage payments and avoid foreclosure.

The loan modification process can be complicated and difficult. Most homeowners are denied a few times before they are finally approved. Often, the denials are legitimate--because the process is confusing, many homeowners don't do it correctly.

A property became eligible if the analysis showed a lender or investor currently holding the loan would make more money by modifying the loan rather than foreclosing. Other than the requirement that a homeowner prove financial hardship, the home had to be habitable and have an unpaid principal balance under $729,750.

The loan modification process typically takes 6 to 9 months, depending on your lender.

Why are only 20% of homeowners who apply getting approval for loan modifications? It's a staggering statistic, so lets look at why banks are denying this process in today's market.

Modified HAMP Rules HAMP Tier 2 guidelines expanded eligibility to more homeowners than HAMP Tier 1 guidelines. HAMP Tier 2 allows non-owner occupant properties; therefore, a borrower can modify a rental property or a vacant home as long as the borrower intends to rent it.

Eligibility requirements for mortgage modifications vary from lender to lender, but you typically must: Be at least one regular mortgage payment behind or show that missing a payment is imminent.

Loan modification is when a lender agrees to alter the terms of a homeowner's existing loan to help them avoid default and keep their house during times of financial hardship. The goal of a mortgage loan modification is to reduce the borrower's payments so they can afford their loan month-to-month.