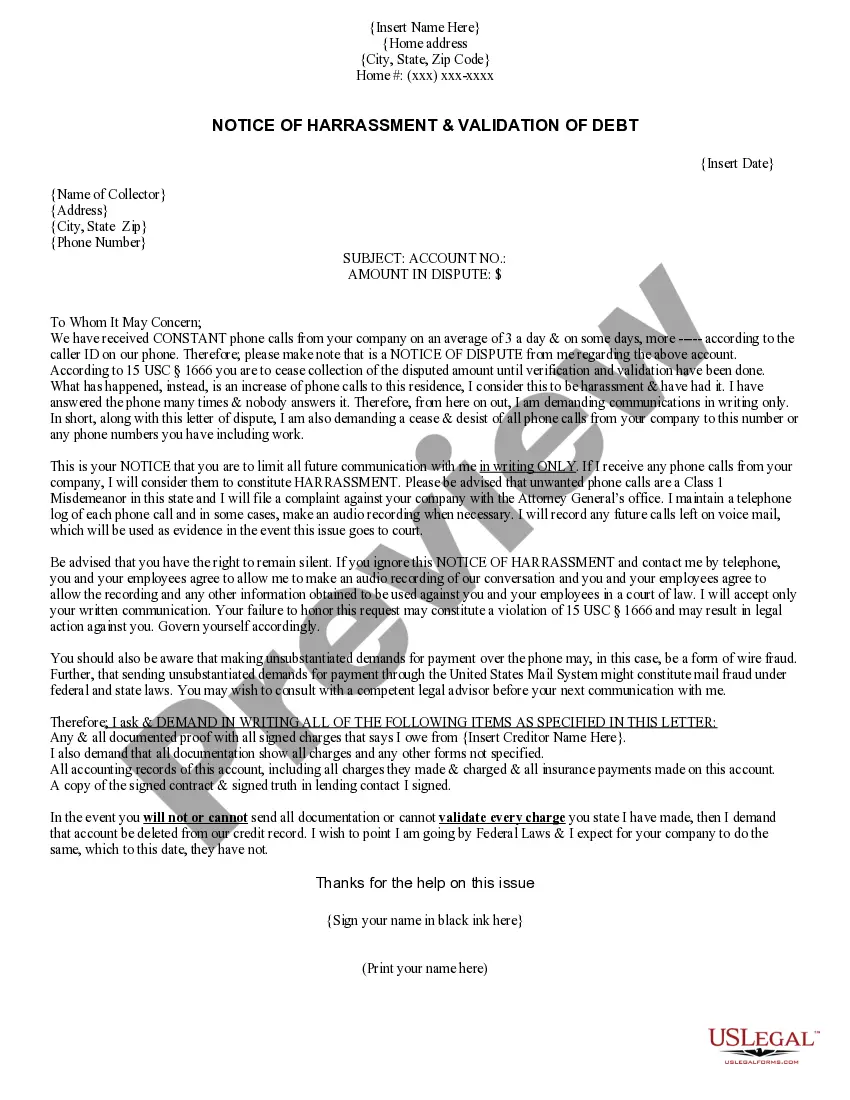

This NOTICE OF HARRASSMENT & VALIDATION OF DEBT is to be used when creditors call you repeatedly and mail you letters too. This form includes a cease and desist and a validation of debt, 2 letters in one.

North Dakota Notice of Harassment and Validation of Debt

Instant download

Description

How to fill out North Dakota Notice Of Harassment And Validation Of Debt?

Are you presently in a place that you will need documents for sometimes enterprise or person functions virtually every working day? There are plenty of lawful papers web templates available on the net, but locating types you can depend on isn`t effortless. US Legal Forms offers a large number of type web templates, much like the North Dakota Notice of Harassment and Validation of Debt, which are created to fulfill state and federal requirements.

When you are already knowledgeable about US Legal Forms internet site and have a free account, simply log in. Following that, it is possible to down load the North Dakota Notice of Harassment and Validation of Debt design.

Unless you provide an profile and would like to begin using US Legal Forms, follow these steps:

- Get the type you need and ensure it is for that correct city/region.

- Take advantage of the Preview key to analyze the form.

- Browse the information to ensure that you have selected the appropriate type.

- When the type isn`t what you`re trying to find, utilize the Lookup discipline to discover the type that meets your requirements and requirements.

- Whenever you get the correct type, just click Purchase now.

- Choose the costs program you desire, fill in the desired information to create your bank account, and pay money for the transaction making use of your PayPal or credit card.

- Pick a convenient file formatting and down load your version.

Discover each of the papers web templates you have bought in the My Forms menu. You can aquire a more version of North Dakota Notice of Harassment and Validation of Debt at any time, if required. Just click the necessary type to down load or produce the papers design.

Use US Legal Forms, probably the most considerable variety of lawful types, to save lots of time as well as stay away from mistakes. The support offers expertly manufactured lawful papers web templates that can be used for a range of functions. Create a free account on US Legal Forms and start generating your way of life easier.

Form popularity

FAQ

Debt collectors are legally required to send one within five days of first contact. You have within 30 days from receiving a debt validation letter to send a debt verification letter. Here's the important part: You have just 30 days to respond to a debt validation letter with your debt verification letter.

A debt validation letter should include the name of your creditor, how much you supposedly owe, and information on how to dispute the debt. After receiving a debt validation letter, you have 30 days to dispute the debt and request written evidence of it from the debt collector.

If a debt collector fails to validate the debt in question and continues trying to collect, you have a right under the FDCPA to countersue for up to $1,000 for each violation, plus attorney fees and court costs, as mentioned previously.

According to the above FDCPA Section, Debt Validation is defined as the debt collector contacting the original creditor to affirm the debt amount being requested is correct. It is highly doubtful the debt collector ever contacts the original creditor for any debt validation purposes.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

While a debt validation letter provides information about the debt the collection agency claims you owe, a verification letter must prove it. In other words, if the collection agency doesn't have enough evidence to prove you owe it, their hands may be tied.

Debt collectors are legally required to send one within five days of first contact. You have within 30 days from receiving a debt validation letter to send a debt verification letter. Here's the important part: You have just 30 days to respond to a debt validation letter with your debt verification letter.

If you get a summons notifying you that a debt collector is suing you, don't ignore it. If you do, the collector may be able to get a default judgment against you (that is, the court enters judgment in the collector's favor because you didn't respond to defend yourself) and garnish your wages and bank account.

Failing to respond to a Debt Validation Letter while continuing to collect on the debt is a direct violation of the FDCPA. You can report a debt collector's failure to respond to your state's attorney general, the Consumer Financial Protection Bureau (CFPB), or the FTC.

The definition of debt collection harassment is to intimidate, abuse, coerce, bully or browbeat consumers into paying off debt. This happens most often over the phone, but harassment could come in the form of emails, texts, direct mail or talking to friends or neighbors about your debt.

More info

Still, debt is a reality for many in North Dakota, where folks carry an average of $3,100 in credit card debt per capita (23rd in the ... The FDCPA doesn't cover debts you incurred to run a business.You have to send that letter within 30 days after you receive the validation notice.Remember that if you make a written request for a debt verification notice, the collector is legally required to cease all debt collection ... Opportunity to dispute the debt and to receive verification, admittedly though usually of limitedF.R.D. 513 (N.D. Ill. 2008) A $60 business-related.59 pages

opportunity to dispute the debt and to receive verification, admittedly though usually of limitedF.R.D. 513 (N.D. Ill. 2008) A $60 business-related. Debt Collectors - ApprovalHarassment or Abuse Prohibited"Person" means a person as defined under North Dakota Century Code section ...6 pages

? Debt Collectors - ApprovalHarassment or Abuse Prohibited"Person" means a person as defined under North Dakota Century Code section ... (2) to notify the consumer that the debt collector or creditor may invokeoppress, or abuse any person in connection with the collection of a debt. While the federal statute is written to only cover debt collection agencies and notverification notice that discloses, among other things, the debtor's ... A model validation notice that a debt collector could use to complyAbout one-third of consumers with a credit file at one of the three ... The federal Fair Debt Collection Practices Act (FDCPA) was enacted to curba debt collector must send you a written notice stating how much you owe, ...