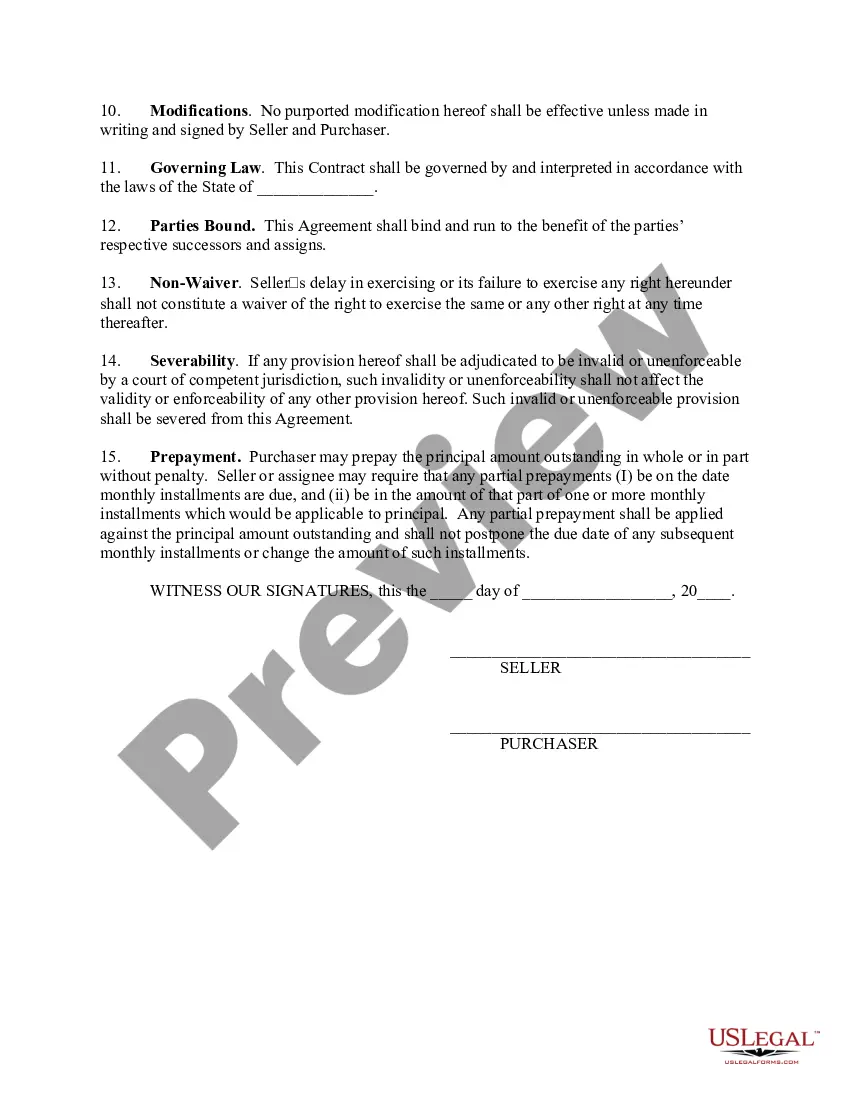

A retail installment agreement is an agreement signed by the Purchaser involving a finance charge and providing for the sale of goods or services. Federal and some State Laws (Consumer Credit Protection Acts) require the disclosure of what the Purchaser is being charged for the credit he/she is receiving. These disclosures include such things as the amount being financed; finance charges; the annual percentage rate; and the number of payments and when due. However, such disclosures are usually only required when a person regularly extends consumer credit (e.g. more than 25 times in the preceding calendar year).

This form is for a casual seller who does not enter into such transactions on a regular basis. It can also be used in commercial transactions (e.g., credit that is not being extended primarily for personal, family, or household purposes).

The Purchaser in this form grants the Seller a security interest in the collateral being sold. A security interest is an interest in personal property or fixtures that secures payment or performance of an obligation. The Seller requires the Purchaser to secure the obligation with the personal property being purchased so that if the Purchaser does not pay as promised, the Purchaser can take the collateral back, sell it, and apply the proceeds against the unpaid obligation of the Purchaser.

The Nebraska Retail Installment Contract or Agreement is a legal document that establishes the terms and conditions of a retail sale transaction between a buyer and a seller in the state of Nebraska. This agreement is commonly used in retail financing situations where the buyer agrees to purchase goods or services from the seller and pay for them in installments over a set period of time. The Nebraska Retail Installment Contract or Agreement encompasses various essential details, including the identification of the buyer and seller, a detailed description of the items or services being purchased, the purchase price, the total amount financed, the finance charge, the interest rate, the repayment schedule, and other pertinent terms and conditions. One notable feature of the Nebraska Retail Installment Contract or Agreement is the inclusion of a finance charge, which represents the cost of credit or the interest rate applied to the amount financed. This charge is regulated by the Nebraska Uniform Consumer Credit Code and must comply with the statutory limits set in place. There are different types of Nebraska Retail Installment Contracts or Agreements that may be tailored to specific retail transactions or industries. Some common variations include automobile retail installment contracts, electronics retail installment contracts, furniture retail installment contracts, and appliance retail installment contracts. These variations reflect the specific nature of the goods being financed and may have additional clauses that address particular considerations like warranty, return policy, or property insurance. Overall, the Nebraska Retail Installment Contract or Agreement serves as a legally binding agreement that protects the rights of both the buyer and seller in a retail financing transaction. It ensures transparency and clarity by outlining all essential terms and obligations, helping to avoid misunderstandings and promoting fair and responsible retail financing practices.