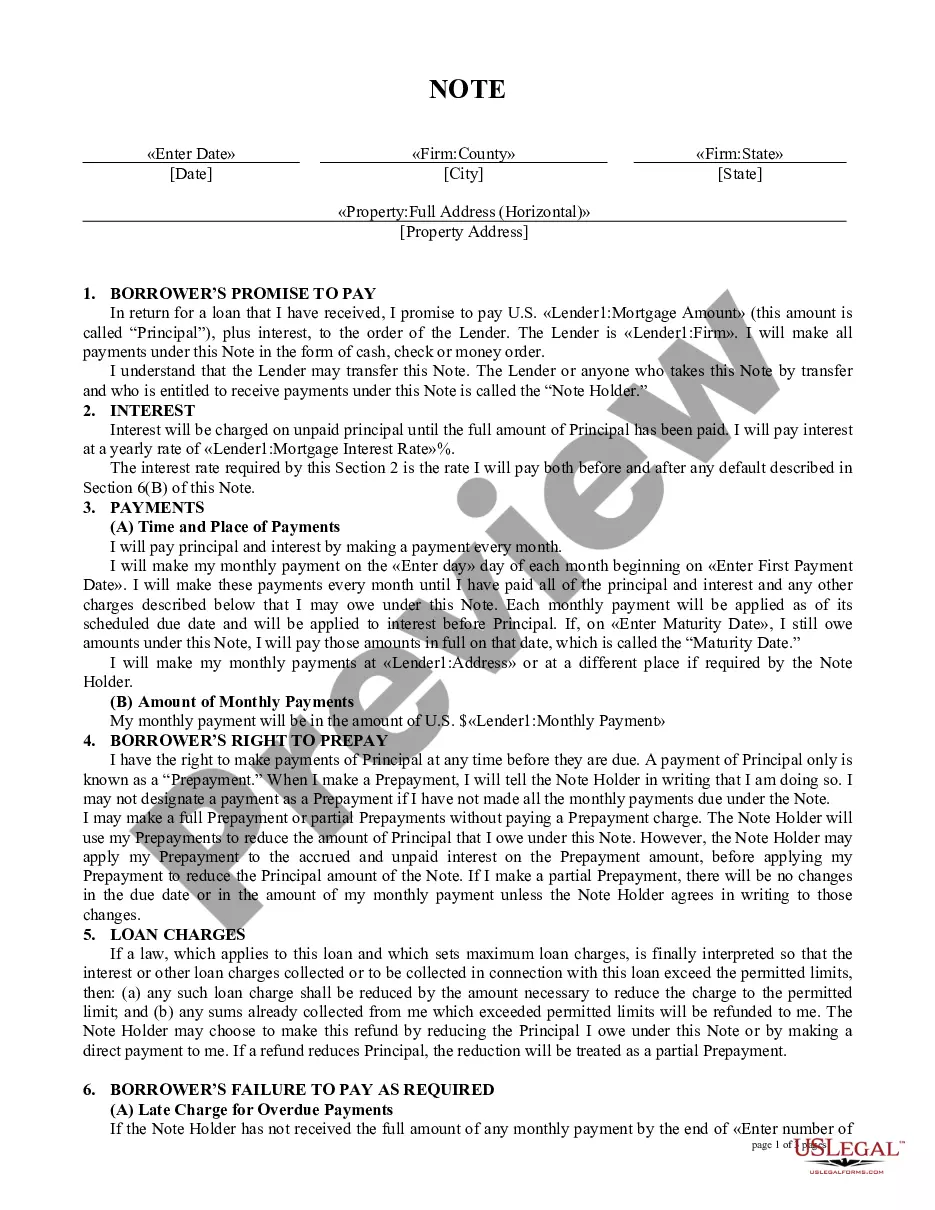

Nebraska Adjustable Rate Rider - Variable Rate Note

State:

Multi-State

Control #:

US-01828

Format:

Word;

Rich Text

Instant download

Description

Adjustable Rate Rider - Variable Rate Note: An Adjustable Rate Ride is a note which contains provisions allowing for the changes in interest rates every year. If the interest rate increases, the Borrower's monthly payments will be higher. If the interest rate decreases, the Borrower's monthy payments will be lower. This form is available in both Word and Rich Text formats.

Free preview

How to fill out Adjustable Rate Rider - Variable Rate Note?

If you wish to finalize, obtain, or print sanctioned document templates, utilize US Legal Forms, the most extensive collection of legal forms available online.

Leverage the website's straightforward and user-friendly search to find the documents you require.

Various templates for business and personal purposes are organized by categories and regions, or keywords.

Step 4. Once you have found the form you need, click the Purchase now button. Choose the payment plan you prefer and enter your information to register for the account.

Step 5. Complete the transaction. You can use your Visa or Mastercard or PayPal account to finalize the payment.

- Employ US Legal Forms to locate the Nebraska Adjustable Rate Rider - Variable Rate Note in just a few clicks.

- If you are already a US Legal Forms user, sign in to your account and click the Download button to obtain the Nebraska Adjustable Rate Rider - Variable Rate Note.

- Additionally, you can access forms you previously downloaded in the My documents section of your account.

- If this is your first time using US Legal Forms, follow the instructions below.

- Step 1. Ensure you have selected the form for the correct region/country.

- Step 2. Utilize the Review option to examine the form's details. Be sure to read the description.

- Step 3. If you are not satisfied with the form, use the Search section at the top of the screen to find alternative versions of the legal form template.