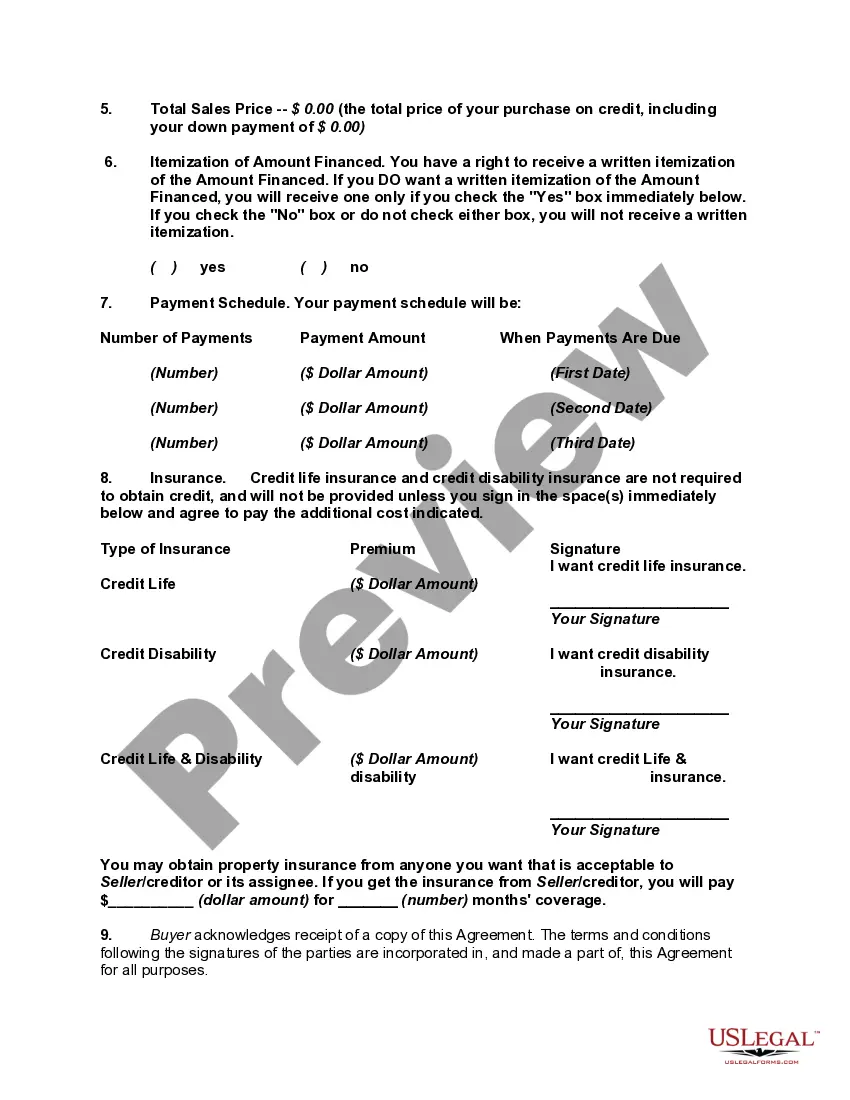

Disclosure of credit terms should have the content and form required under the federal Truth in Lending Act (15 U.S.C.A. §§ 1601 et seq.) and applicable regulations (Regulation Z, 12 C.F.R. § 226), and under state consumer credit laws to the extent that they differ from the federal Act. In connection with specified installment sales and other consumer credit transactions, these enactments require written disclosure and advice as to finance charges, annual percentage rates and other matters relating to credit. Under the federal Act, the disclosures may be set forth in the contract document itself or in a separate statement or statements.

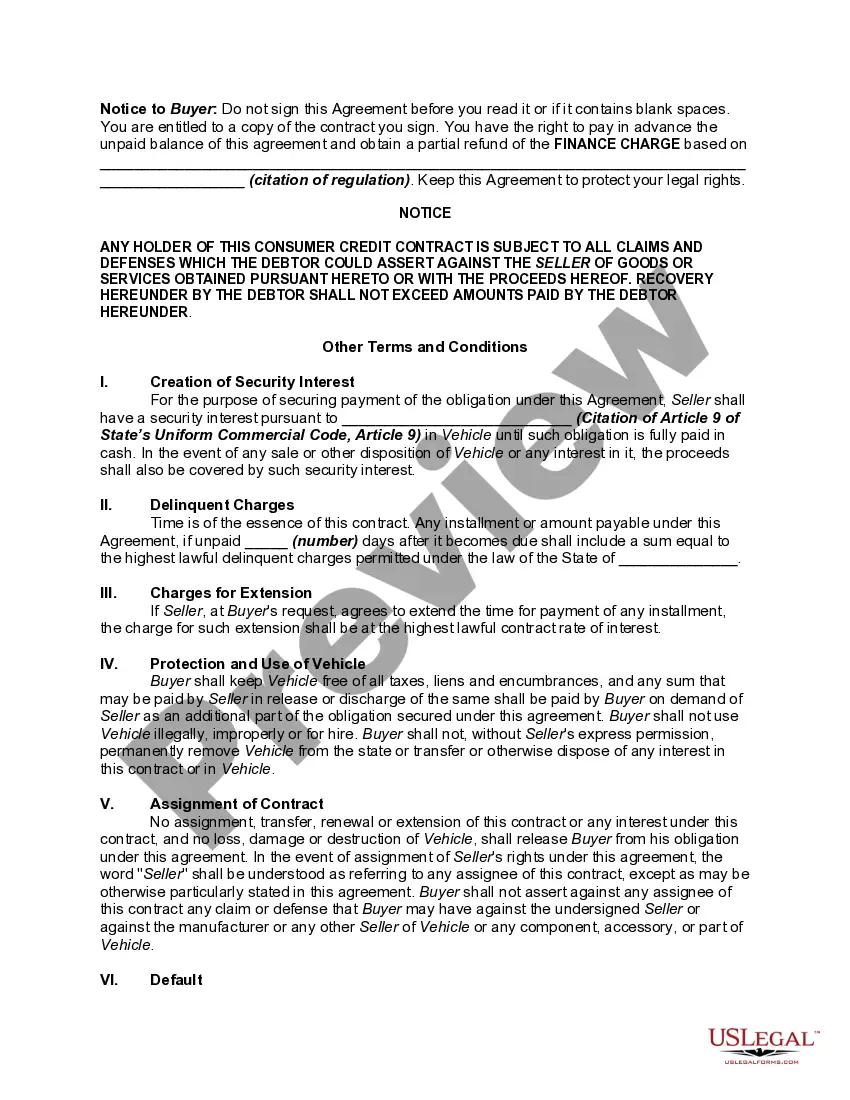

A federal notice regarding preservation of the consumer's claims and defenses is required on all consumer credit contracts by Federal Trade Commission regulation. 16 C.F.R. § 433.2. The notice must appear in 10-point bold type or print and must be worded as set forth in the above form.

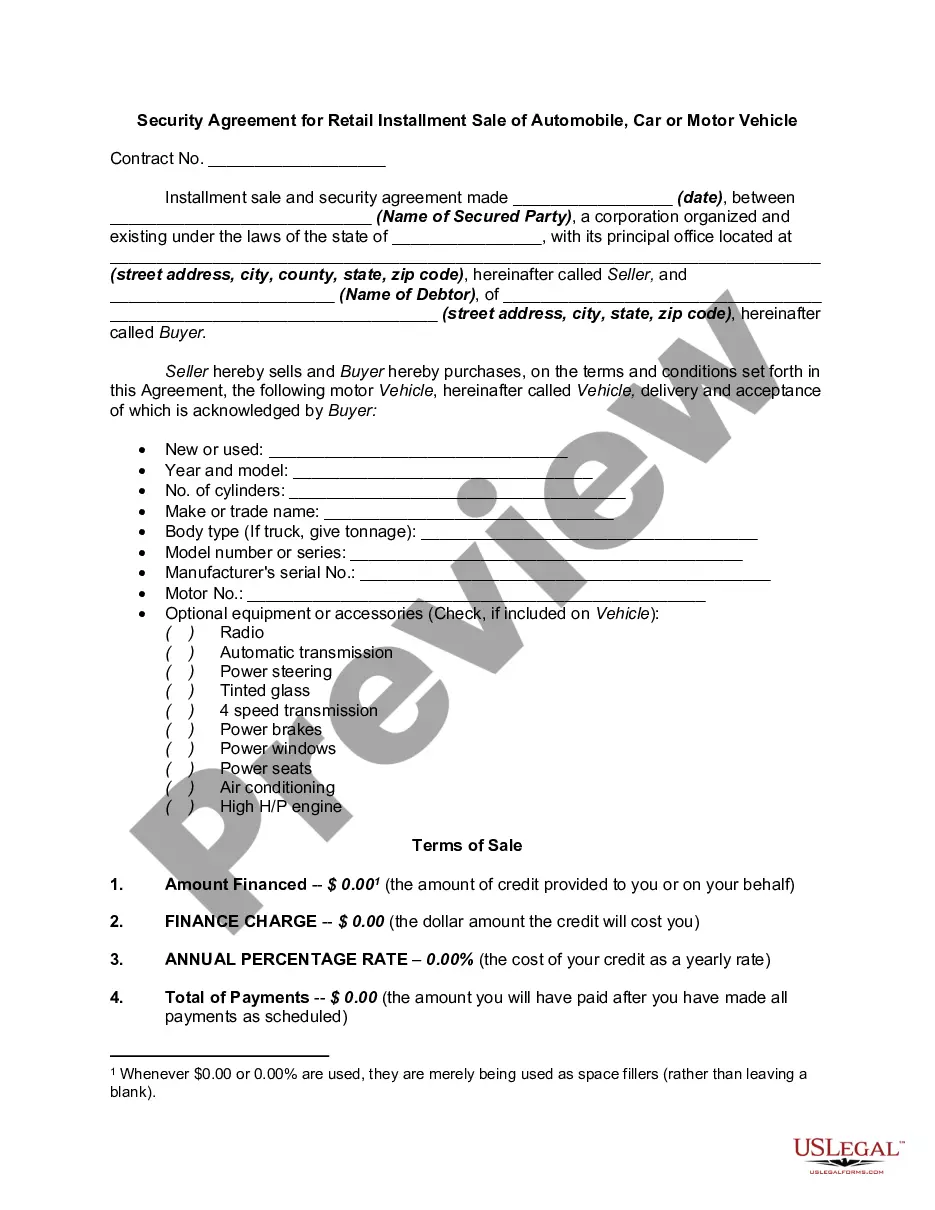

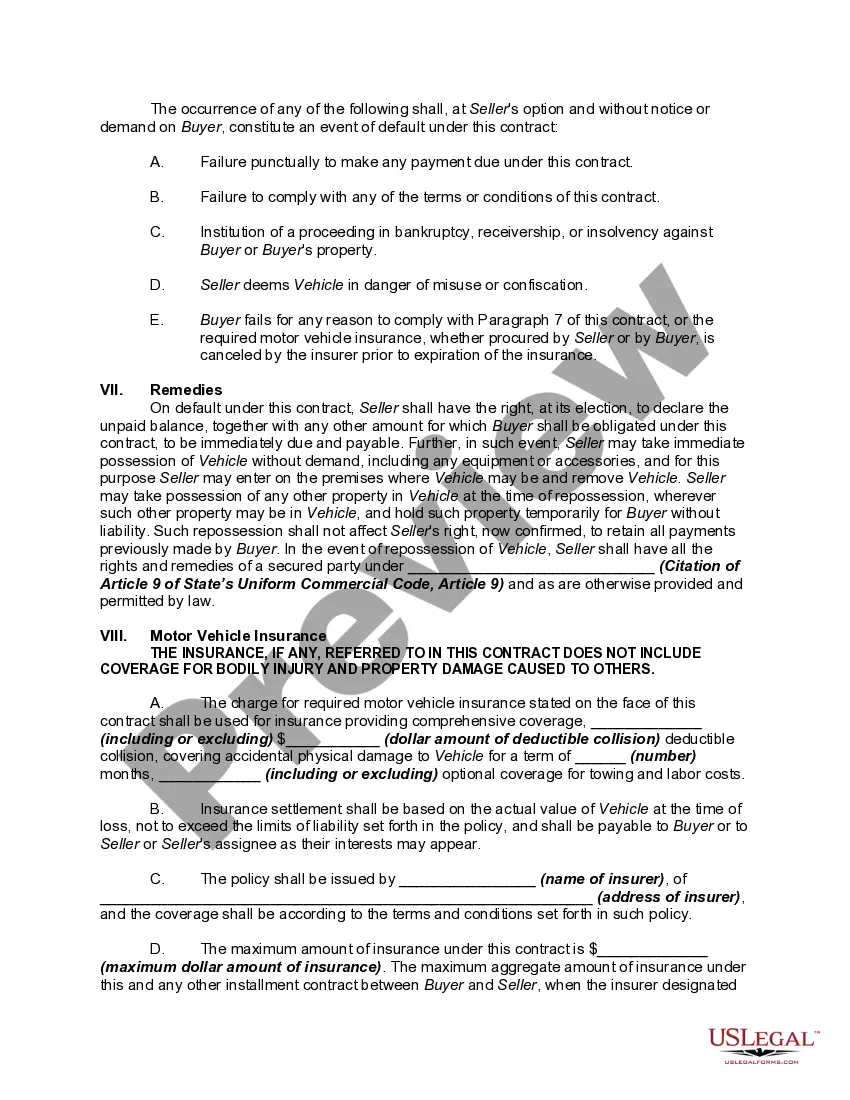

Nebraska Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle is a legally binding document that establishes a lien against a vehicle, ensuring the repayment of a loan or credit extended for its purchase. This agreement protects the rights of both the lender and the buyer by outlining clear terms and conditions of the transaction. Keywords: Nebraska Security Agreement, Retail Installment Sale, Automobile, Car, Motor Vehicle, Lien, Loan, Credit, Purchase, Repayment, Terms, Conditions. Different types of Nebraska Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle may include: 1. Individual Buyer Agreement: This type of agreement is executed between an individual buyer and the lender, commonly a financial institution. It outlines the obligations and responsibilities of the buyer to repay the loan amount within the specified timeframe. 2. Dealer Financing Agreement: This type of agreement is entered into between a car dealer and the buyer. Here, the car dealer finances the purchase directly, offering the convenience of obtaining financing at the point of sale. 3. Secured Loan Agreement: This agreement is used when the vehicle serves as collateral for a loan. The lender retains the right to repossess the vehicle if the borrower fails to make timely payments. 4. Lease Agreement: In some cases, the Nebraska Security Agreement may also cover lease arrangements. This agreement permits the lessee to use the vehicle for a predetermined period in exchange for regular payments, while the lessor maintains ownership. 5. Subordination Agreement: A subordination agreement is sometimes necessary when multiple parties have an interest in the vehicle. It clarifies the priority of the Nebraska Security Agreement and ensures that the rights of all parties involved are properly defined. 6. Refinancing Agreement: This type of agreement is relevant when the primary loan is refinanced to take advantage of better interest rates or improved terms. It establishes a revised security agreement between the new lender and the borrower. Nebraska Security Agreement for Retail Installment Sale of Automobile, Car or Motor Vehicle is a crucial legal document that protects the interests of all parties involved in financing or purchasing a vehicle in Nebraska. Ensuring that the agreement is properly drafted and executed is essential for a smooth and secure transaction.