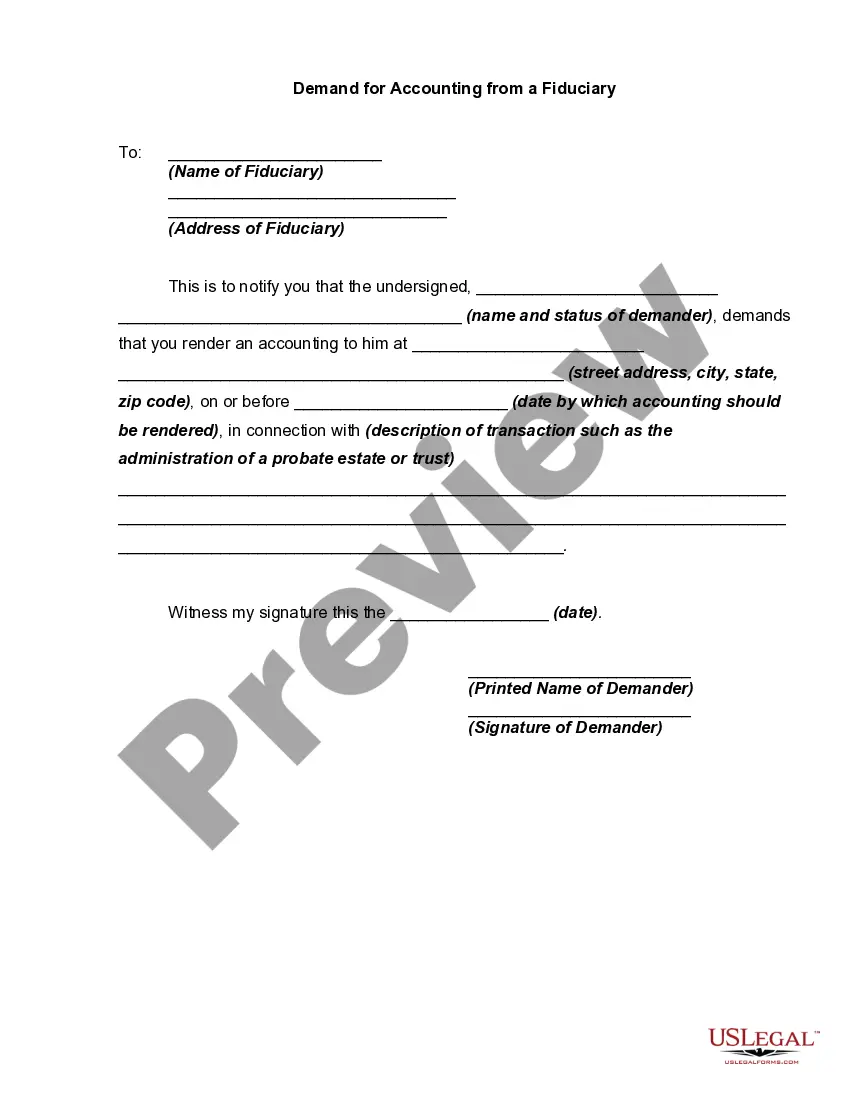

Sometimes, a prior demand by a potential plaintiff for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Nebraska Demand for Accounting from a Fiduciary: Understanding the Process and Types In Nebraska, a demand for accounting from a fiduciary is a legal request made by a beneficiary or interested party to obtain a detailed report of the fiduciary's financial transactions and activities. This demand aims to ensure transparency and accountability within fiduciary relationships, which commonly include trustees, executors, agents, or guardians. When someone is appointed to act as a fiduciary, they are entrusted with managing and administering assets or property on behalf of another party, known as the beneficiary. Fiduciaries have a legal obligation to act in the best interests of the beneficiary, exercising prudence and avoiding any conflicts of interest. Types of Nebraska Demand for Accounting from a Fiduciary: 1. Trust Accounting Demand: This type of demand is related to trusts, which are legal arrangements where one party holds assets for the benefit of another. Beneficiaries of a trust have the right to request an accounting from the trustee, seeking information on all income, expenses, distributions, assets, and changes in the trust's financial position. 2. Estate Accounting Demand: In cases involving a deceased person's estate, interested parties such as heirs or beneficiaries can demand an accounting from the estate's executor or personal representative. This request is crucial to ensure that all financial matters, including debts, assets, income, and expenses, are meticulously recorded and accurately distributed in line with the decedent's intentions and applicable laws. 3. Power of Attorney Accounting Demand: When a person grants someone a Power of Attorney (POA) to manage their financial affairs, the principal or interested parties can require an accounting from the designated agent. This demand serves as a protective measure against potential abuse or negligence, ensuring that the agent operates within the scope of authority and accounts for all financial transactions carried out on behalf of the principal. The demand for accounting sets in motion a legal process where the fiduciary must provide a comprehensive report, typically including financial statements, bank statements, investment records, receipts, and any other relevant documentation. The fiduciary must present a clear and accurate overview of their financial activities, demonstrating the proper management and preservation of the beneficiary's assets. In Nebraska, the demand for accounting from a fiduciary must comply with specific legal requirements, including deadlines for response, notification methods, and the scope of information requested. Should the fiduciary fail to comply with the demand, interested parties can pursue legal action to compel the fiduciary to provide the necessary documentation or to seek removal from their role if wrongdoing or negligence is suspected. Overall, the demand for accounting from a fiduciary in Nebraska ensures transparency, accountability, and protection of beneficiaries' interests. It provides a vital mechanism for beneficiaries to verify the fiduciary's actions, confirm their compliance with legal responsibilities, and identify any potential breach of duty.