Nebraska Aging of Accounts Payable

Description

How to fill out Aging Of Accounts Payable?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a broad selection of legal document templates that you can download or print.

While using the site, you will find thousands of forms for business and personal purposes, categorized by groups, states, or keywords.

You can access the latest versions of forms like the Nebraska Aging of Accounts Payable in just seconds.

Read the form description to confirm that you have chosen the right form.

If the form does not meet your requirements, use the Search field at the top of the page to find the one that does.

- If you have a subscription, sign in to obtain the Nebraska Aging of Accounts Payable from the US Legal Forms database.

- The Download button will appear on each form you view.

- You can find all previously downloaded forms in the My documents section of your account.

- If you are using US Legal Forms for the first time, here are simple steps to get you started.

- Ensure that you have selected the correct form for your city/state.

- Click the Preview button to review the content of the form.

Form popularity

FAQ

To calculate the average age of accounts payable, divide the total accounts payable by the average daily purchases and multiply the result by the number of days in the period analyzed. This calculation provides valuable insight into a company's payment behavior. Tools and resources available through US Legal Forms can assist in tracking Nebraska Aging of Accounts Payable efficiently.

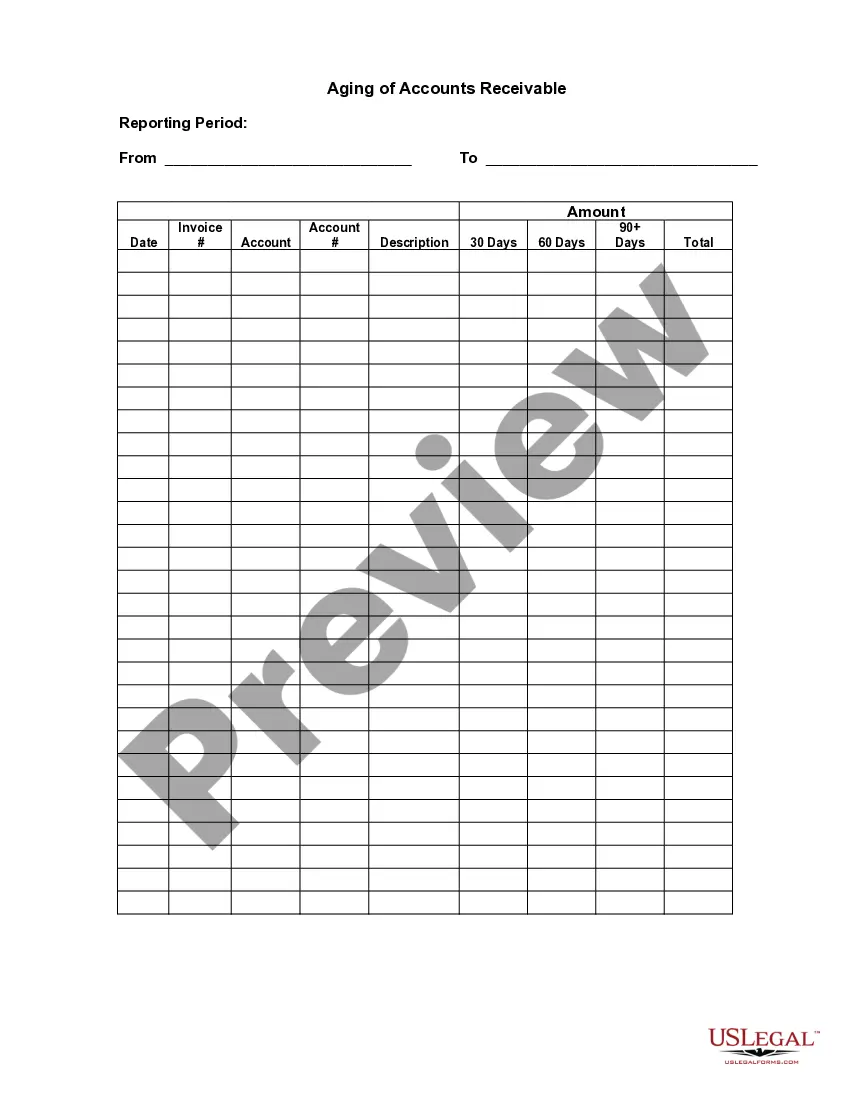

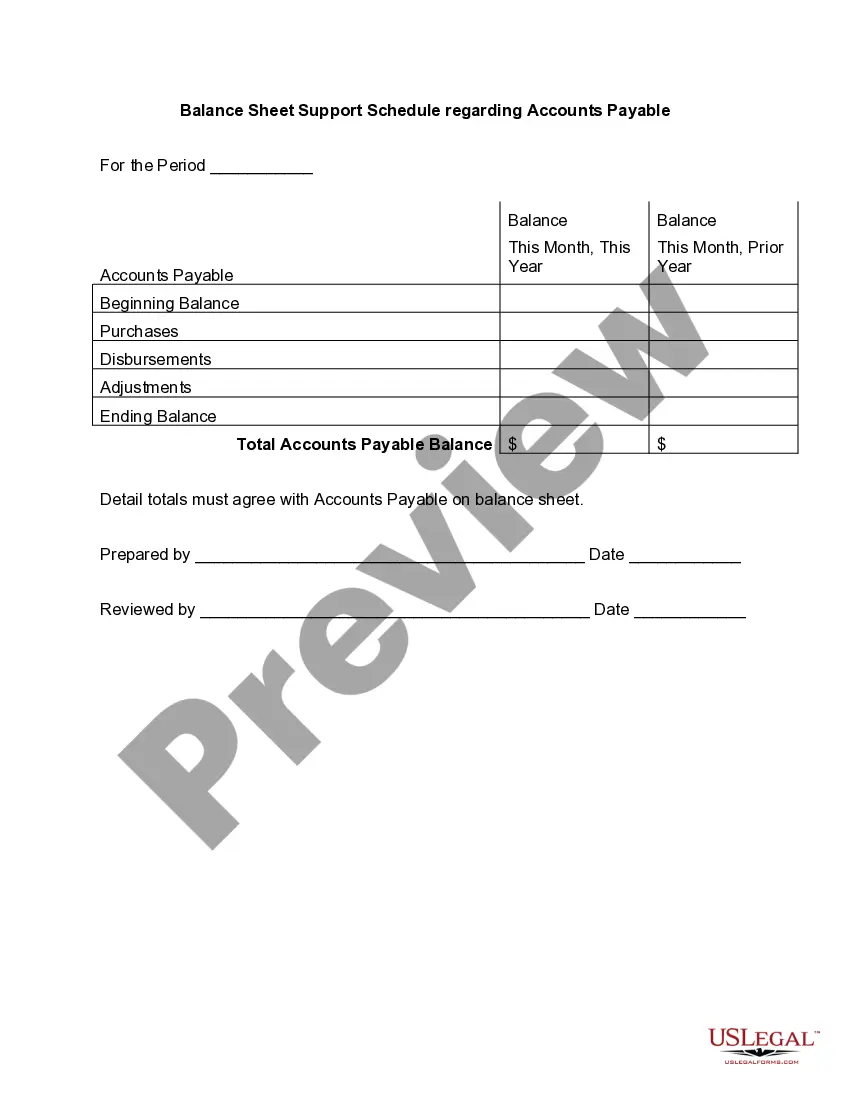

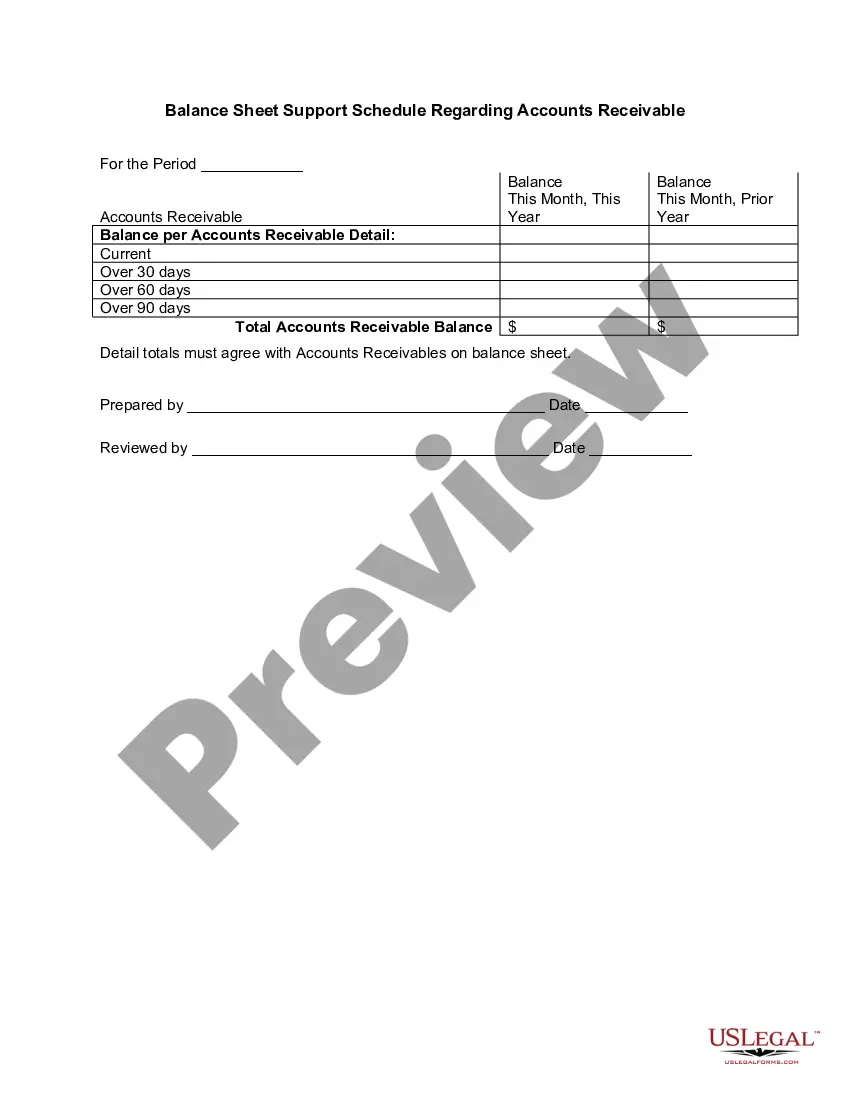

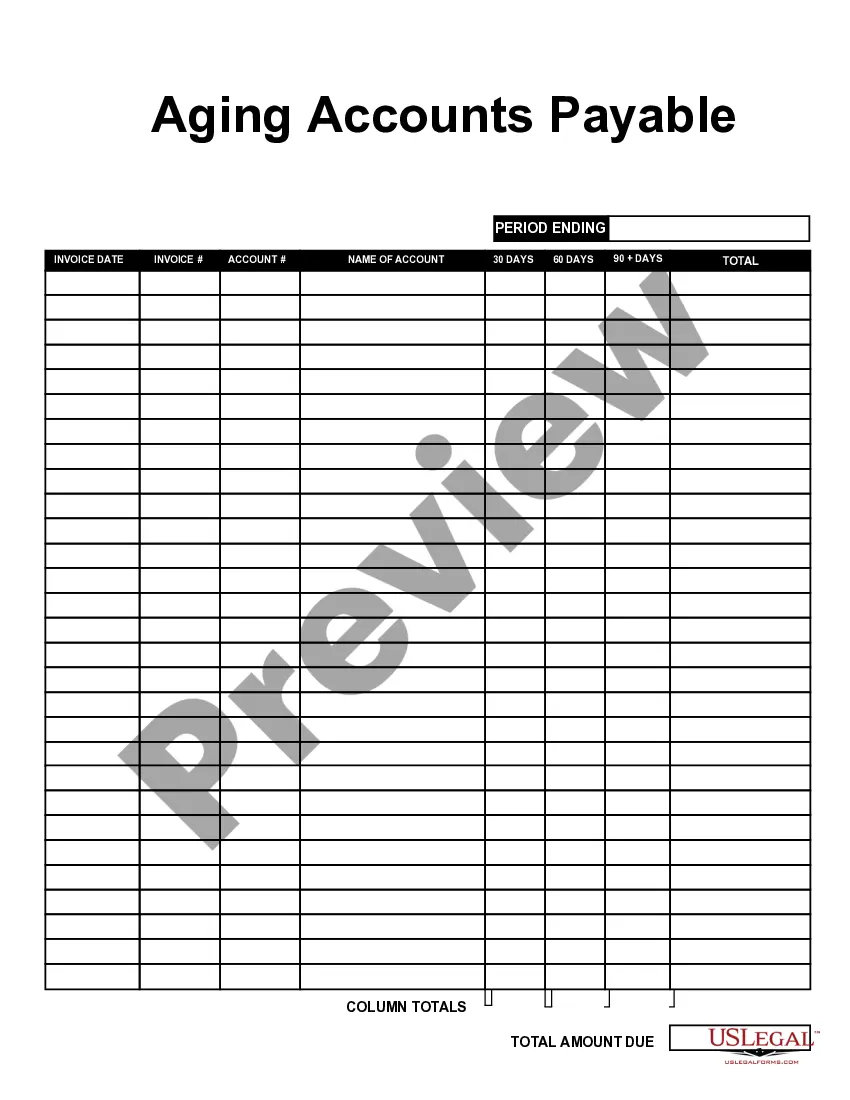

The aging schedule of accounts payable presents a detailed breakdown of all outstanding invoices categorized by their due dates. This schedule assists businesses in organizing their payment obligations effectively. Utilizing features from platforms like US Legal Forms can simplify the creation of an aging schedule, ensuring you stay on top of Nebraska Aging of Accounts Payable.

To do aging of accounts payable, first create an inventory of your unpaid invoices. Classify these invoices based on their due dates by determining how long each invoice has been outstanding. This aging analysis aids in prioritizing payments and understanding your financial standing. Many users find that using US Legal Forms can assist in efficiently managing this process.

Calculating accounts payable aging involves categorizing unpaid invoices by their due dates. Begin by listing your outstanding invoices and their respective due dates. Then, count the days past due for each invoice, grouping them into time frames such as current, 30 days overdue, and beyond. This method provides clear insights into your liabilities and can enhance your decision-making regarding payments.

Yes, Nebraska requires mandatory withholding for state income tax if you are an employer. Understanding these obligations is important for managing your overall tax strategy, particularly regarding Nebraska Aging of Accounts Payable. If you need assistance with forms and compliance, platforms like USLegalForms can offer valuable resources to navigate these regulations.

You should put your permanent residential address or your business address on your tax return. If it relates to Nebraska Aging of Accounts Payable, ensure all details are accurate for proper identification and processing. This accuracy helps the Nebraska Department of Revenue reach you if they have any questions about your return.

You should send your Nebraska state taxes to the Nebraska Department of Revenue at P.O. Box 94818, Lincoln, NE 68509-4818. Using this address helps ensure that your payment and tax documents are handled correctly, which is especially important when you manage items like Nebraska Aging of Accounts Payable. Always double-check that you are using the correct address for your specific tax situation.

Generally, you do not need to attach your federal return to your Nebraska return. However, keeping your federal return handy for reference is wise, especially in matters related to Nebraska Aging of Accounts Payable. Make sure to follow the Nebraska Department of Revenue guidelines to ensure you meet all requirements.

Your amended Nebraska tax return should be sent to P.O. Box 94818, Lincoln, NE 68509-4818. It is important to use this address for efficient processing of your return, particularly when addressing matters related to Nebraska Aging of Accounts Payable. Double-check your paperwork before mailing to avoid any delays.

You should mail your amended Nebraska state tax return to the Nebraska Department of Revenue at P.O. Box 94818, Lincoln, NE 68509-4818. Using the correct address is crucial, especially when dealing with issues like Nebraska Aging of Accounts Payable. Ensure your return is complete and includes your payment, if applicable, for timely processing.