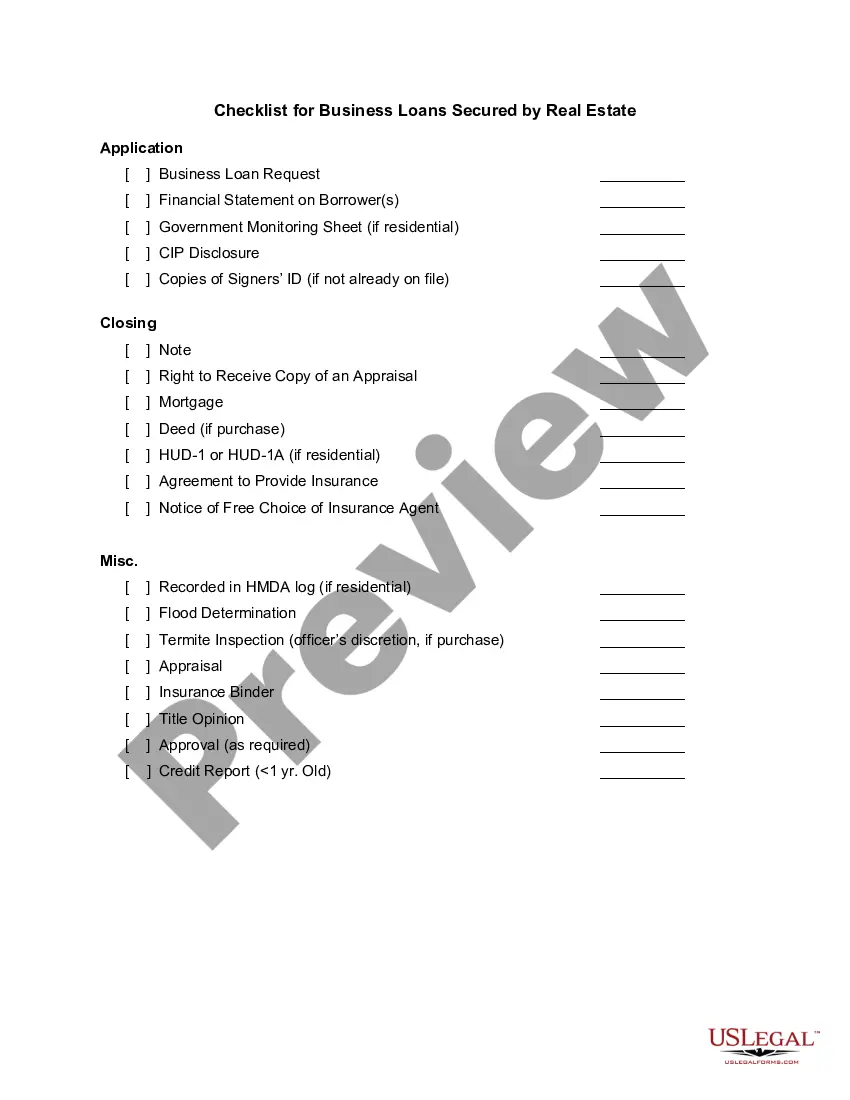

Nebraska Checklist for Business Loans Secured by Real Estate: Overview, Criteria, and Types Nebraska offers various types of business loans secured by real estate to support local businesses. To ensure a successful loan application process, it is crucial to adhere to the specific checklist provided by the state. Understanding the requirements and preparing the necessary documents is essential for securing these loans. Below is a detailed description of the Nebraska Checklist for Business Loans Secured by Real Estate, along with the different types available. 1. Loan Criteria: — Eligibility: Businesses must be located in Nebraska or planning to establish operations in the state. — Real Estate Collateral: The loan must be secured by commercial or industrial property owned or being purchased by the business. — Business Plan: Applicants are required to submit a comprehensive business plan detailing their operations, financial projections, and future growth strategies. — Financial Statements: Proof of both personal and business financial stability is required, including income statements, balance sheets, and cash flow forecasts. — Credit History: A credit report for both the business and owners should be provided to demonstrate good creditworthiness. — Owner's Contribution: Lenders typically expect business owners to invest a certain percentage of their funds into the project. 2. Types of Nebraska Business Loans Secured by Real Estate: a. Small Business Administration (SBA) Loans: SBA offers multiple loan programs for businesses, including the SBA 7(a) Loan, SBA 504 Loan, and SBA Microloan. These loans provide long-term, low-interest financing options for real estate purchases, renovation, construction, or refinancing. b. Commercial Real Estate Loans: This type of loan is specifically designed for businesses requiring substantial funding for purchasing or refinancing commercial properties, such as office buildings, retail spaces, or warehouses. c. Construction Loans: Businesses planning to construct new facilities or renovate existing ones can opt for construction loans secured by real estate. These loans cover the costs of land acquisition, architecture, construction, and other related expenses. d. Bridge Loans: Bridge loans are suitable for businesses looking to acquire or upgrade property promptly. These short-term loans bridge the financing gap until more permanent financing can be secured. By adhering to Nebraska's checklist for business loans secured by real estate, businesses can maximize their chances of obtaining the necessary funding for expansion, development, or operational needs. It is important to research and understand the specific requirements for each type of loan to select the most appropriate option for your business. Seek guidance from professional consultants or financial institutions to ensure a smooth loan application process.

Nebraska Checklist for Business Loans Secured by Real Estate

Description

How to fill out Nebraska Checklist For Business Loans Secured By Real Estate?

Have you been in a situation where you need files for either business or person uses virtually every day? There are tons of lawful record templates accessible on the Internet, but getting versions you can rely isn`t simple. US Legal Forms provides thousands of develop templates, such as the Nebraska Checklist for Business Loans Secured by Real Estate, that happen to be published to meet federal and state needs.

Should you be currently acquainted with US Legal Forms web site and get an account, simply log in. Following that, you may down load the Nebraska Checklist for Business Loans Secured by Real Estate format.

Unless you offer an profile and wish to start using US Legal Forms, adopt these measures:

- Discover the develop you want and make sure it is to the appropriate metropolis/county.

- Make use of the Preview key to examine the shape.

- Browse the description to actually have selected the proper develop.

- In case the develop isn`t what you are looking for, make use of the Search area to get the develop that meets your needs and needs.

- Once you discover the appropriate develop, click Get now.

- Pick the prices prepare you need, complete the desired details to produce your money, and pay for an order using your PayPal or Visa or Mastercard.

- Pick a practical data file formatting and down load your backup.

Find every one of the record templates you may have purchased in the My Forms food list. You can aquire a further backup of Nebraska Checklist for Business Loans Secured by Real Estate whenever, if possible. Just click the necessary develop to down load or printing the record format.

Use US Legal Forms, one of the most comprehensive variety of lawful kinds, to conserve some time and stay away from mistakes. The services provides professionally manufactured lawful record templates which can be used for a range of uses. Create an account on US Legal Forms and begin making your daily life easier.