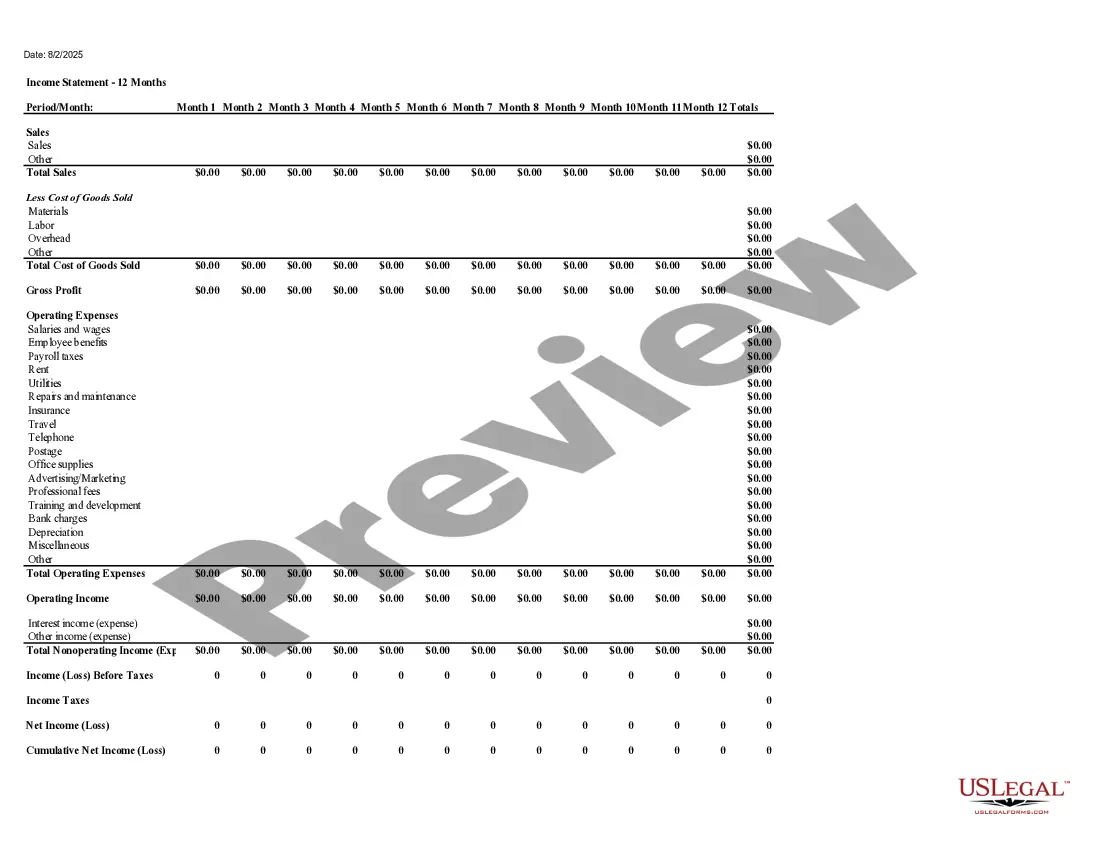

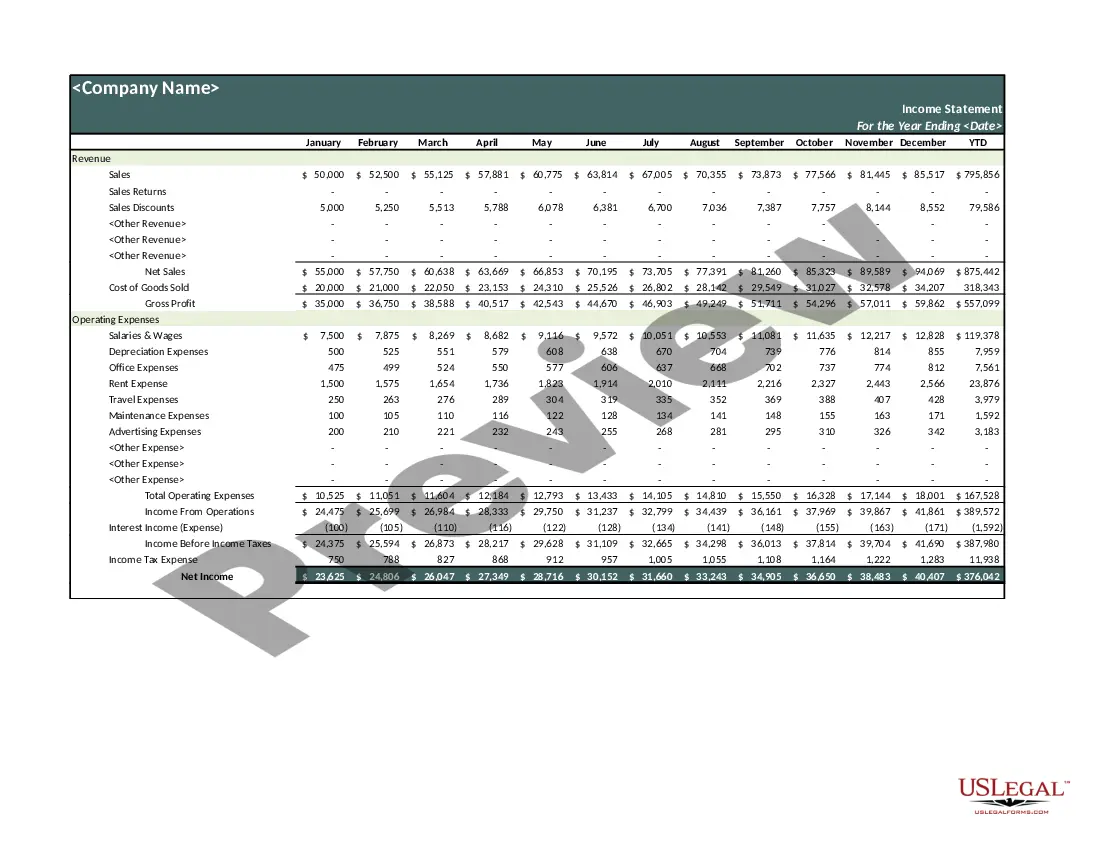

An income statement (sometimes called a profit and loss statement) lists your revenues and expenses, and tells you the profit or loss of your business for a given period of time. You can use this income statement form as a starting point to create one yourself.

Nebraska Income Statement

Category:

State:

Multi-State

Control #:

US-03600BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Income Statement?

You can spend hours online searching for the authentic document template that meets the state and federal regulations you require. US Legal Forms offers a multitude of legal forms that are reviewed by experts.

You can obtain or create the Nebraska Income Statement using our service.

If you already possess a US Legal Forms account, you can Log In and click on the Download button. After that, you can fill out, modify, print, or sign the Nebraska Income Statement. Every legal document template you purchase is yours indefinitely. To obtain another copy of the purchased form, navigate to the My documents section and click on the appropriate button.

Make changes to your document if possible. You can fill out, modify, sign, and print the Nebraska Income Statement. Download and print thousands of document templates using the US Legal Forms site, which offers the largest selection of legal forms. Utilize professional and state-specific templates to address your business or personal needs.

- If you are using the US Legal Forms site for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for the region/city of your choice. Review the form description to make sure you have chosen the accurate form. If available, utilize the Review button to examine the document template as well.

- If you wish to find another variant of the form, use the Search field to locate the template that suits your needs.

- Once you have found the template you require, click on Get now to proceed.

- Select the pricing plan you want, enter your credentials, and register for your account on US Legal Forms.

- Complete the transaction. You can use your Visa or Mastercard or PayPal account to purchase the legal form.

- Choose the format of your document and download it to your device.

Form popularity

FAQ

To prepare an income statement, follow these four steps: first, gather your revenue data, second, categorize your expenses, third, calculate the net income, and fourth, present your findings clearly. Ensuring accuracy at each step is crucial, and consulting resources like USLegalForms can greatly simplify the process, especially for your Nebraska Income Statement.

Writing an income statement involves summarizing your financial performance over a specific time. Start with total revenues, subtract costs of goods sold, and then deduct operating expenses to find net income. If you're looking for a clear structure, USLegalForms can guide you in drafting a compliant Nebraska Income Statement.

In Nebraska, most types of income are taxable, including wages, salaries, and income from businesses. Additionally, interest and dividends are subject to tax. It’s important to be aware of your responsibilities, and using a Nebraska Income Statement can help you track taxable income efficiently.

Filling out a basic income statement involves listing your business's revenues, subtracting expenses, and determining the net income. Begin with your total sales or revenue at the top, then categorize your expenses into different sections, such as direct costs and operating expenses. For an efficient process, USLegalForms can provide customizable templates for Nebraska Income Statements.

To calculate an income statement, start by collecting your revenue and expenses for a specific period. Subtract the total expenses from your total revenue to find your net income. If you need detailed guidance, consider using USLegalForms, which offers templates and resources tailored for filling out a Nebraska Income Statement.

Filing an income statement in Nebraska involves assembling your income records and filling out the appropriate forms. You can submit your Nebraska Income Statement electronically for convenience or choose to mail it. If you seek guidance, consider utilizing platforms like US Legal Forms for templates and resources to help you through the file preparation process.

The 1040 tax statement is a federal tax form used by U.S. taxpayers to report their annual income. When filing your Nebraska Income Statement, consider how your 1040 interacts with state requirements, as income reported on your 1040 affects your state filing. Understanding both forms can help you manage your overall tax liability.

If you earn income in Nebraska, you typically need to file a Nebraska Income Statement. There are certain thresholds and specific situations that may exempt you, but generally, if you meet the income requirements, you must file. Always check the specific filing requirements each year to ensure compliance.

You should mail your Nebraska Income Statement to the address specified by the Nebraska Department of Revenue on the instruction sheet of the tax form. Typically, the mailing address varies depending on whether you are expecting a refund or owe taxes. Make sure to check the latest guidelines on their website to send it to the correct location.

Filing your Nebraska Income Statement involves several steps. Begin by gathering all required documentation, completing the necessary forms online or via paper, and verifying your information for accuracy. After filing, keep a copy of your statement for your records, and track the status of your submission through the Nebraska Department of Revenue.