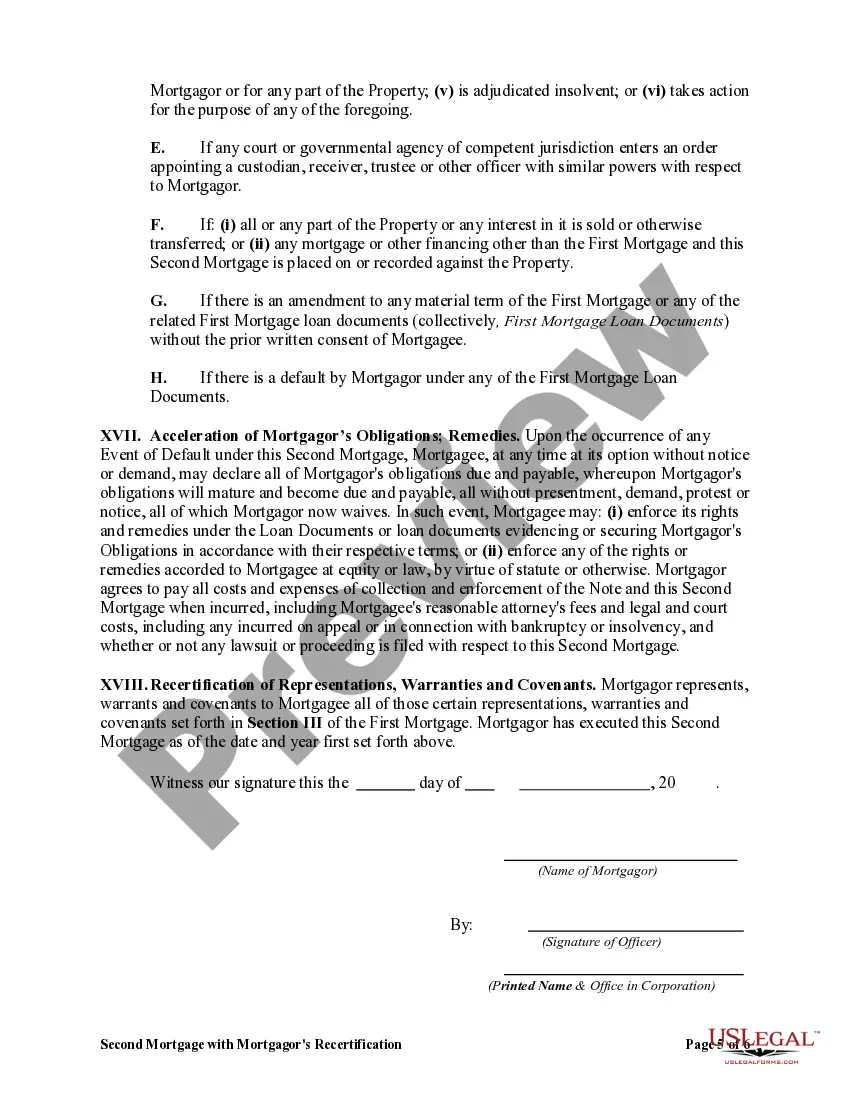

A Nebraska Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage is a financial agreement that allows homeowners in Nebraska to borrow against the equity they have built in their first mortgage. This type of mortgage is also known as a home equity loan or a home equity line of credit (HELOT). The Nebraska Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage requires the mortgagor (the borrower) to reaffirm the statements, promises, and guarantees made in the original first mortgage. This ensures that the mortgagor still meets the eligibility criteria, financial obligations, and other requirements as stipulated in the first mortgage. By obtaining a second mortgage, homeowners in Nebraska can access additional funds for various purposes, such as home renovations, debt consolidation, educational expenses, or any other financial need. Unlike the first mortgage, which is used to purchase the property initially, the second mortgage leverages the accumulated equity in the home. It's important to note that there can be different types of Nebraska Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage. Some common variations include: 1. Fixed-Rate Second Mortgage: This type of second mortgage offers a fixed interest rate throughout the loan term, providing stability in monthly installments. This is beneficial for borrowers who prefer predictable payments. 2. Home Equity Line of Credit (HELOT): HELOT acts as a revolving line of credit, allowing homeowners to borrow funds multiple times up to a predetermined credit limit. Borrowers can withdraw funds as needed, and the interest is typically variable, based on market conditions. 3. Adjustable-Rate Second Mortgage: In this type, the interest rate can fluctuate over time, depending on market conditions. This can result in varying monthly payments, making it essential for borrowers to understand the potential risks involved. To initiate a Nebraska Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage, homeowners usually need to submit an application, provide updated financial information, and consent to a thorough evaluation by the mortgage lender. The lender will assess the borrower's creditworthiness, income stability, and the value of the property to determine the loan terms and conditions. Obtaining a second mortgage can be a beneficial financial tool, but it is crucial for borrowers to thoroughly understand the terms, repayment options, and any potential risks associated with the loan. Seeking advice from a qualified financial advisor or mortgage professional is recommended to make informed decisions about the specific requirements and offerings of a Nebraska Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage.

Nebraska Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage

Description

How to fill out Nebraska Second Mortgage With Mortgagor's Recertification Of Representations, Warranties And Covenants In First Mortgage?

You can devote hrs on the web attempting to find the authorized file design that meets the state and federal requirements you will need. US Legal Forms provides a huge number of authorized kinds which are reviewed by professionals. It is simple to acquire or print the Nebraska Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage from our assistance.

If you already possess a US Legal Forms profile, you can log in and click on the Acquire option. After that, you can full, edit, print, or sign the Nebraska Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage. Each authorized file design you get is the one you have forever. To acquire another copy for any bought type, proceed to the My Forms tab and click on the corresponding option.

If you use the US Legal Forms website for the first time, adhere to the straightforward directions under:

- Very first, make sure that you have chosen the proper file design for the county/metropolis that you pick. Browse the type explanation to ensure you have chosen the proper type. If offered, utilize the Review option to appear from the file design also.

- If you would like locate another variation from the type, utilize the Lookup discipline to get the design that meets your requirements and requirements.

- Upon having found the design you want, simply click Get now to continue.

- Choose the pricing program you want, key in your qualifications, and register for your account on US Legal Forms.

- Complete the deal. You can use your bank card or PayPal profile to pay for the authorized type.

- Choose the format from the file and acquire it to the device.

- Make changes to the file if necessary. You can full, edit and sign and print Nebraska Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage.

Acquire and print a huge number of file web templates making use of the US Legal Forms web site, which offers the largest variety of authorized kinds. Use professional and condition-specific web templates to handle your business or person needs.

Form popularity

FAQ

A first mortgage is a primary lien on the property that secures the mortgage. The second mortgage is money borrowed against home equity to fund other projects and expenditures.

TL;DR: The primary mortgage market is used for homebuyers and lenders. Lenders finance a borrower's purchase of a home. The secondary mortgage market is between lenders and mortgage investors. Lenders will sell the debt to the investor who will buy it to make a profit.

First Mortgagee means any person named as a mortgagee or beneficiary in any First Mortgage, or any successor to the interest of any such person under such First Mortgage.

The Bottom Line Because the second mortgage also uses the same property for collateral as the first mortgage, the original mortgage has priority on the collateral should the borrower default on their payments. If the loan goes into default, the first mortgage lender gets paid before the second mortgage lender.

A second mortgage, however, allows you to use your home's equity and put it to work. Instead of having that money tied up in your home, it's available for expenses you have right now. This option can be a help or a hindrance, depending on your financial goals.