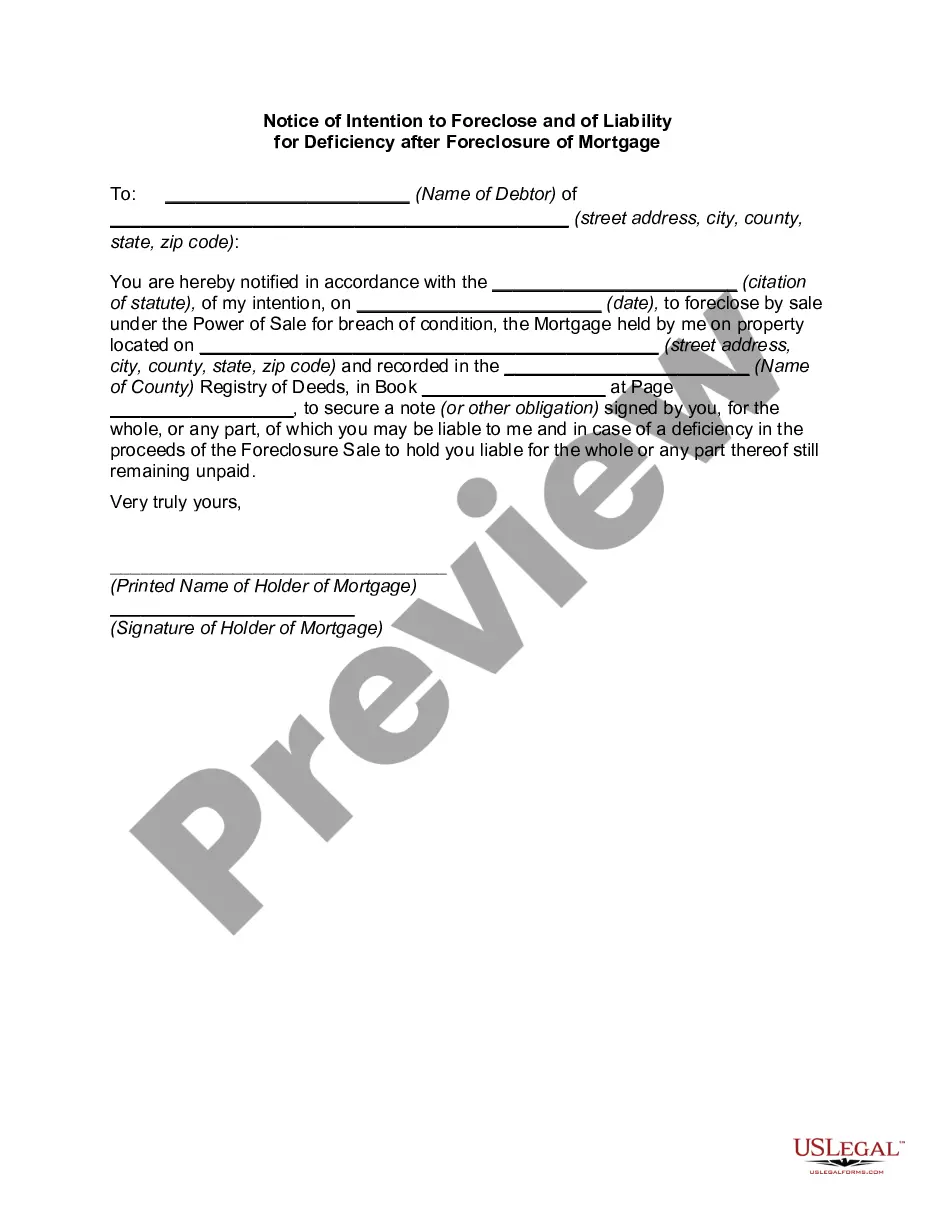

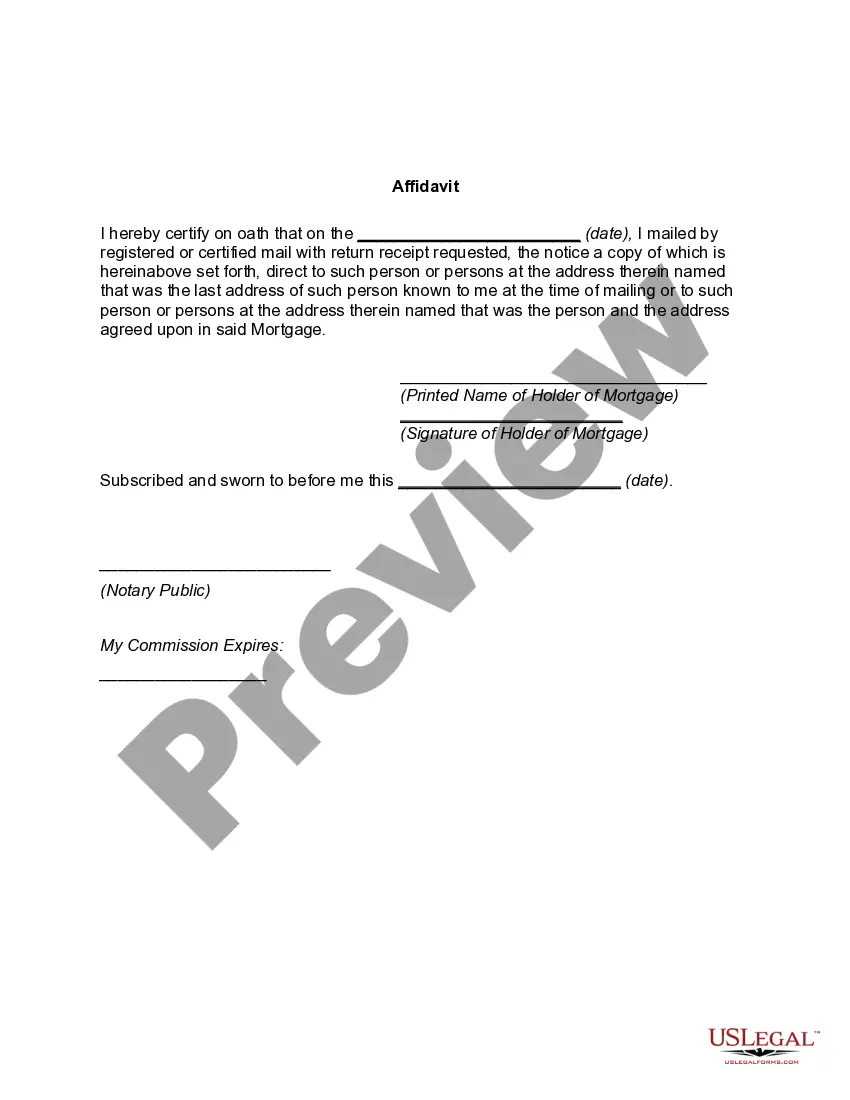

Nebraska Notice of Intention to Foreclose and Liability for Deficiency after Foreclosure of Mortgage is a legal document that serves as a warning to the property owner that their mortgage is at risk of being foreclosed upon. This notice is typically sent by the lender or mortgage holder to inform the homeowner of their intention to initiate foreclosure proceedings if the debt is not satisfied within a certain time frame. The Nebraska Notice of Intention to Foreclose outlines the specific details of the mortgage default, including the amount owed, any missed payments, and the actions that need to be taken to prevent foreclosure. It is crucial for homeowners to take this notice seriously and seek legal counsel or explore alternatives to avoid foreclosure. There are variations of the Nebraska Notice of Intention to Foreclose, tailored to different scenarios and types of mortgages. Some common examples include: 1. Residential Mortgage Notice: This notice is intended for homeowners with residential properties, forewarning them of potential foreclosure due to mortgage default or non-payment. 2. Commercial Mortgage Notice: This type of notice is specifically designed for property owners who have commercial mortgages, informing them of the imminent foreclosure proceedings if the mortgage debt is not rectified. 3. Second Mortgage Notice: In cases where homeowners have taken out a second mortgage or secured a home equity loan, this notice serves as a warning that the lender will initiate foreclosure if the outstanding debt is not resolved. 4. Mortgage Deficiency Liability Notice: After the foreclosure of a property, this notice alerts the former homeowner to their potential liability for deficiency. It means they may be responsible for paying the remaining debt that was not recovered through the foreclosure sale. When faced with a Nebraska Notice of Intention to Foreclose and Liability for Deficiency after Foreclosure of Mortgage, it is crucial for homeowners to carefully review the document and understand its implications. Seeking immediate legal advice can help explore options such as loan modification, refinancing, short sales, or negotiating a repayment plan to avoid foreclosure and minimize financial liabilities. Ignoring or delaying action after receiving this notice may lead to severe consequences, including the loss of the property and potential legal actions.

Nebraska Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage

Description

How to fill out Nebraska Notice Of Intention To Foreclose And Of Liability For Deficiency After Foreclosure Of Mortgage?

Choosing the best legitimate file design could be a struggle. Needless to say, there are tons of layouts available online, but how would you discover the legitimate form you require? Take advantage of the US Legal Forms internet site. The service gives a huge number of layouts, such as the Nebraska Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage, which you can use for company and personal needs. All the varieties are examined by specialists and meet state and federal demands.

When you are currently registered, log in in your account and click the Download switch to find the Nebraska Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage. Make use of your account to search from the legitimate varieties you have ordered formerly. Check out the My Forms tab of your account and acquire one more version of the file you require.

When you are a whole new consumer of US Legal Forms, allow me to share easy directions that you should follow:

- Initial, ensure you have chosen the correct form to your area/region. You are able to look through the form while using Review switch and study the form description to make certain this is basically the right one for you.

- In the event the form will not meet your needs, take advantage of the Seach industry to discover the right form.

- Once you are certain that the form is acceptable, click the Get now switch to find the form.

- Choose the rates plan you desire and enter the essential info. Build your account and purchase an order with your PayPal account or bank card.

- Pick the data file format and acquire the legitimate file design in your product.

- Complete, revise and print out and indicator the received Nebraska Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage.

US Legal Forms will be the biggest catalogue of legitimate varieties for which you can find a variety of file layouts. Take advantage of the service to acquire appropriately-created files that follow condition demands.