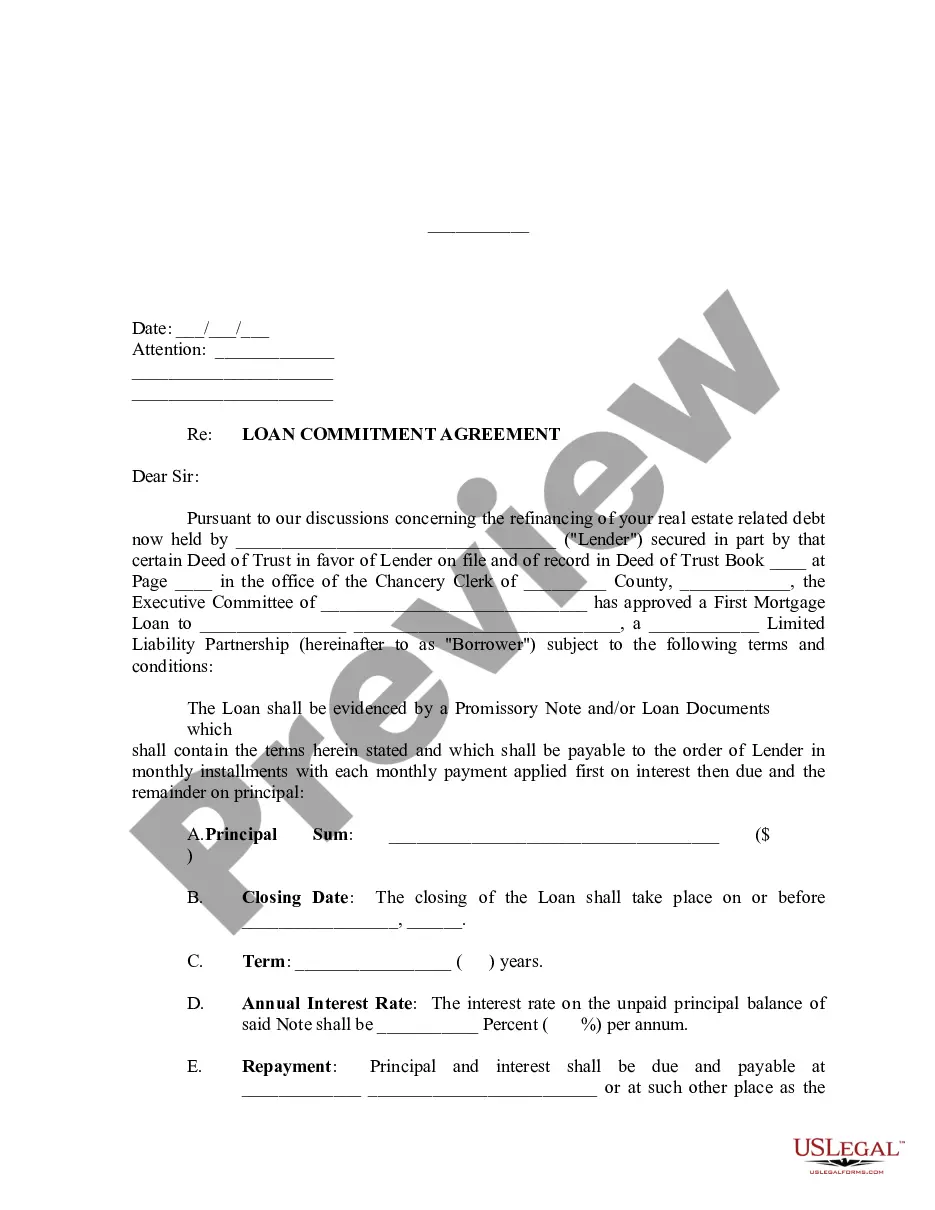

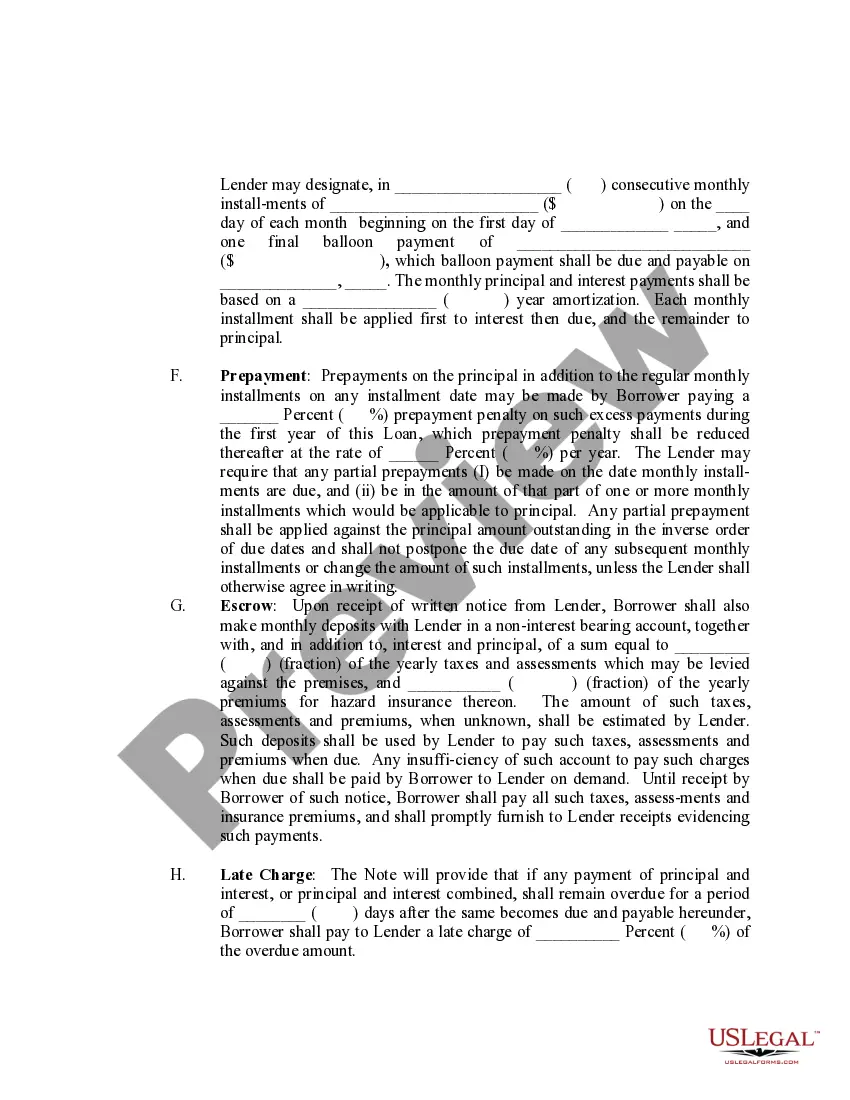

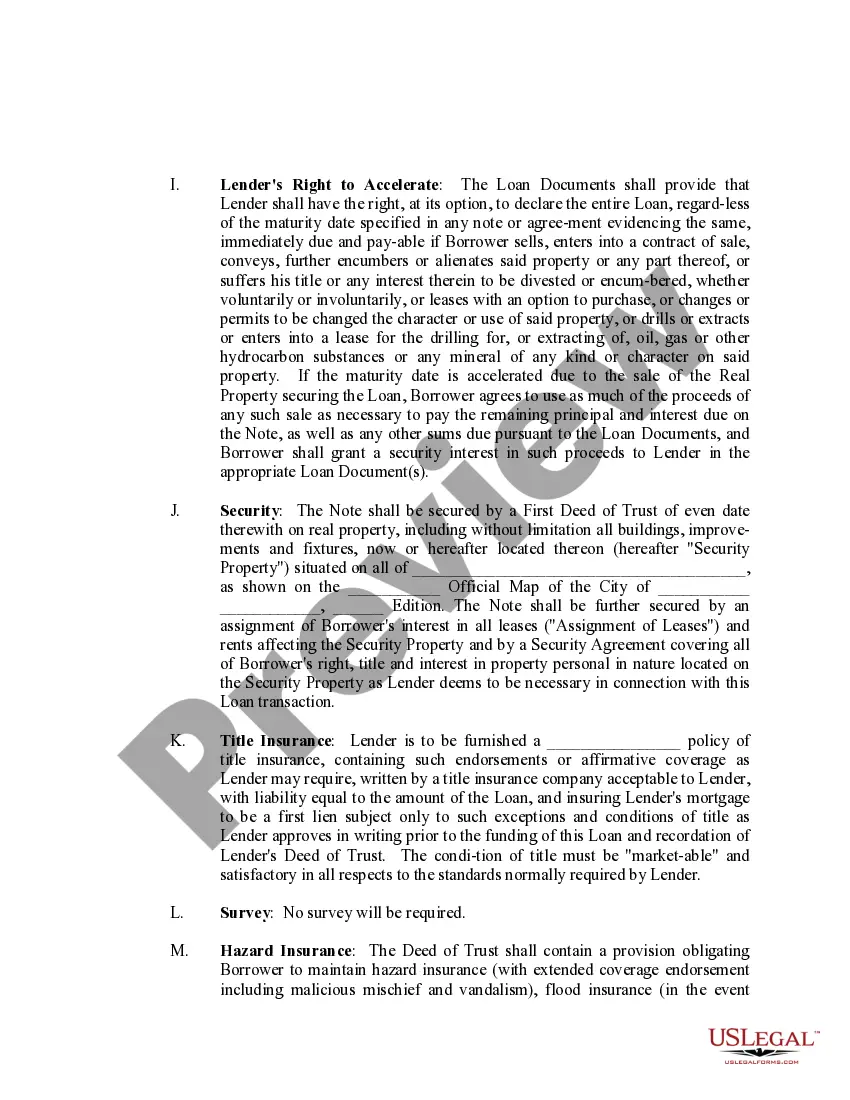

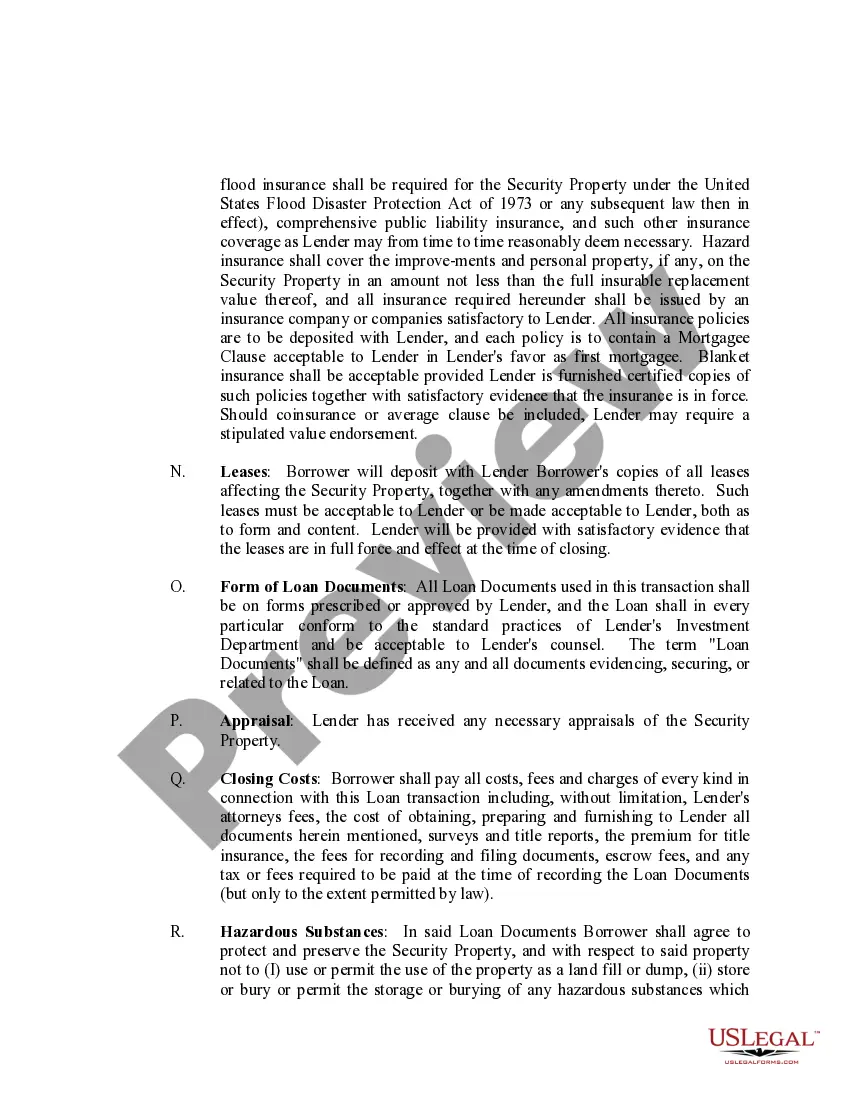

A Nebraska Loan Commitment Agreement Letter is a legal document that outlines the terms and conditions of a loan commitment made by a lender to a borrower in the state of Nebraska. This letter serves as written confirmation of the lender's commitment to extend credit to the borrower based on certain specified conditions and requirements. The Nebraska Loan Commitment Agreement Letter is a vital component of the loan process as it helps both parties understand their rights and obligations. It typically includes details such as the loan amount, interest rate, repayment schedule, collateral requirements, and any additional conditions that must be met before the loan is disbursed. There are different types of Nebraska Loan Commitment Agreement Letters based on the specific loan program or purpose. Some common variations include: 1. Commercial Loan Commitment Agreement Letter: This type of agreement is used when a borrower seeks a loan for commercial purposes, such as starting a business, expanding operations, or investing in commercial real estate. 2. Residential Mortgage Loan Commitment Agreement Letter: In the case of homebuyers or individuals seeking mortgage financing, this letter outlines the terms and conditions for a residential mortgage loan. 3. Agricultural Loan Commitment Agreement Letter: When borrowers in Nebraska require financing for agricultural purposes, such as purchasing farm equipment, acquiring land, or managing crop production, this type of agreement is used. 4. Construction Loan Commitment Agreement Letter: Construction projects often require specialized financing. This agreement specifies the terms and conditions of a loan commitment for building or renovating projects in Nebraska. 5. Small Business Loan Commitment Agreement Letter: For entrepreneurs and small business owners looking to fund their ventures, this agreement outlines the terms and conditions of a loan commitment specifically tailored to small businesses. It's essential to review every detail mentioned in the Nebraska Loan Commitment Agreement Letter thoroughly. Both the lender and borrower should understand their obligations, rights, and the consequences of not meeting the specified terms. Consulting with legal professionals or financial advisors can be helpful to ensure full comprehension of the agreement and to address any concerns or questions before proceeding with the loan.

Nebraska Loan Commitment Agreement Letter

Description

How to fill out Nebraska Loan Commitment Agreement Letter?

Choosing the right lawful file web template can be quite a have a problem. Needless to say, there are plenty of themes accessible on the Internet, but how can you find the lawful form you want? Use the US Legal Forms website. The assistance offers a huge number of themes, including the Nebraska Loan Commitment Agreement Letter, that you can use for business and private needs. Each of the varieties are checked out by professionals and meet up with state and federal needs.

If you are currently signed up, log in to your account and then click the Obtain option to get the Nebraska Loan Commitment Agreement Letter. Make use of account to check with the lawful varieties you might have purchased previously. Check out the My Forms tab of your own account and have yet another duplicate of your file you want.

If you are a whole new consumer of US Legal Forms, here are easy instructions that you can follow:

- Initially, be sure you have chosen the correct form for the area/state. It is possible to look through the form using the Review option and read the form explanation to ensure this is basically the best for you.

- In the event the form fails to meet up with your expectations, use the Seach industry to find the right form.

- Once you are certain that the form would work, click on the Buy now option to get the form.

- Pick the costs plan you need and type in the needed information. Create your account and pay money for your order making use of your PayPal account or credit card.

- Select the data file formatting and acquire the lawful file web template to your system.

- Full, modify and produce and indicator the acquired Nebraska Loan Commitment Agreement Letter.

US Legal Forms is definitely the biggest collection of lawful varieties for which you can see numerous file themes. Use the company to acquire expertly-created papers that follow status needs.