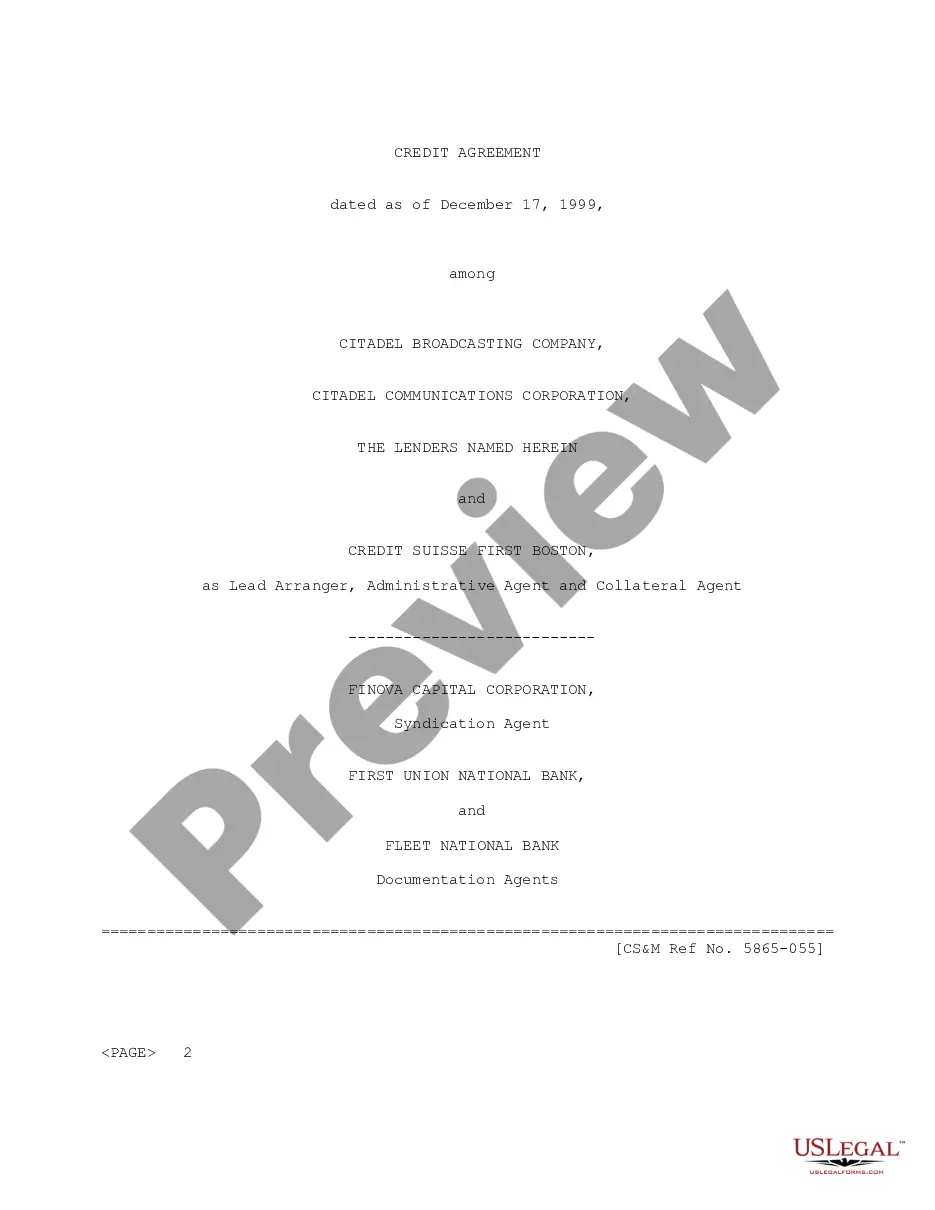

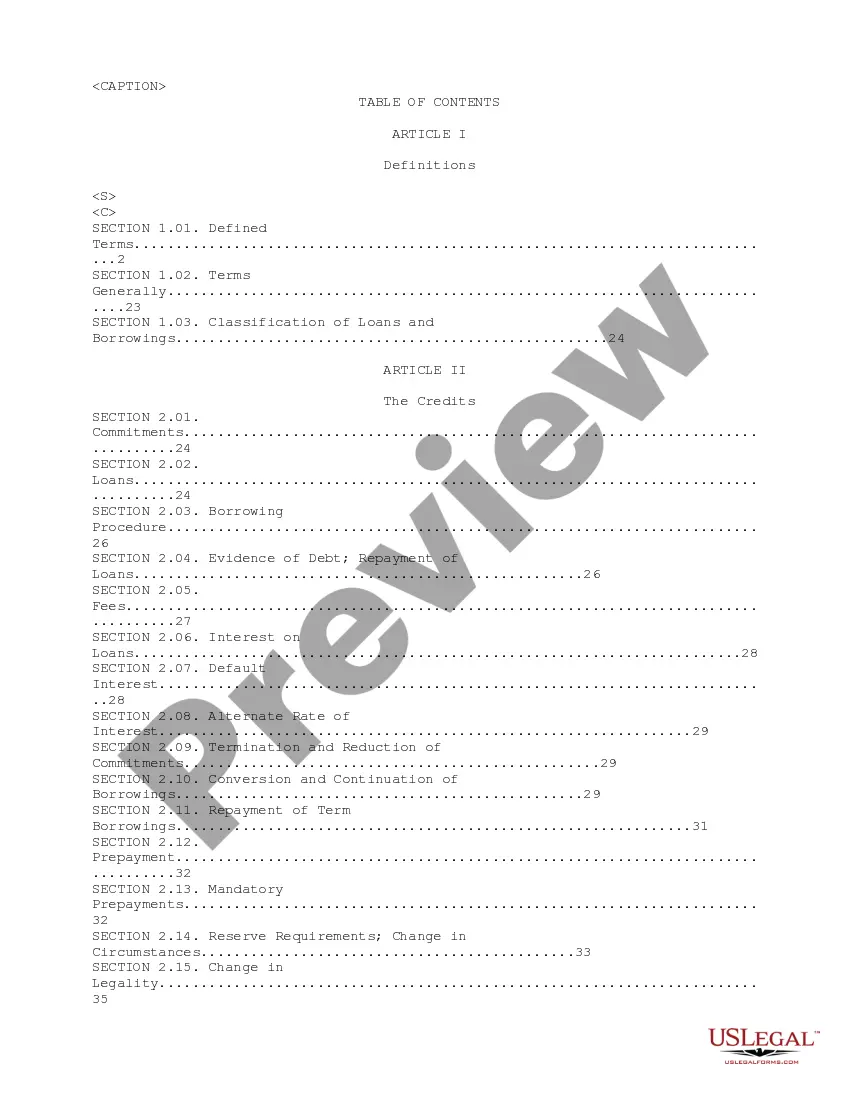

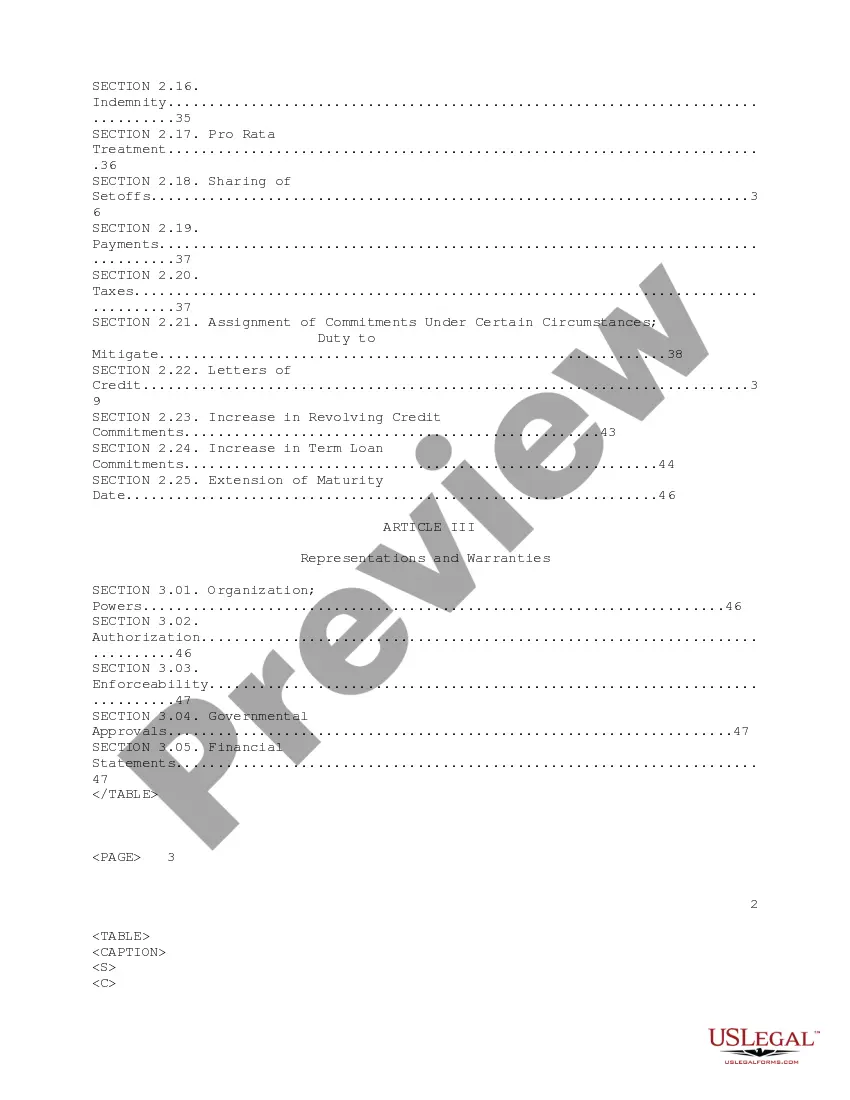

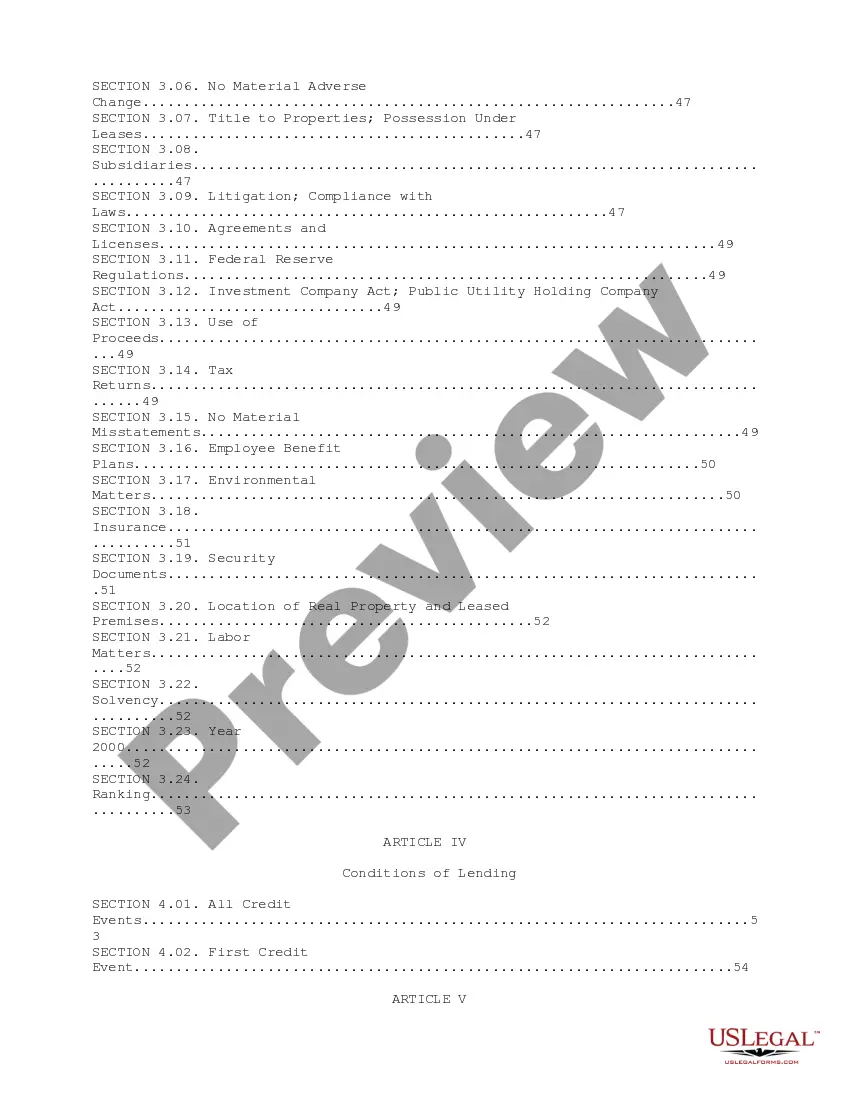

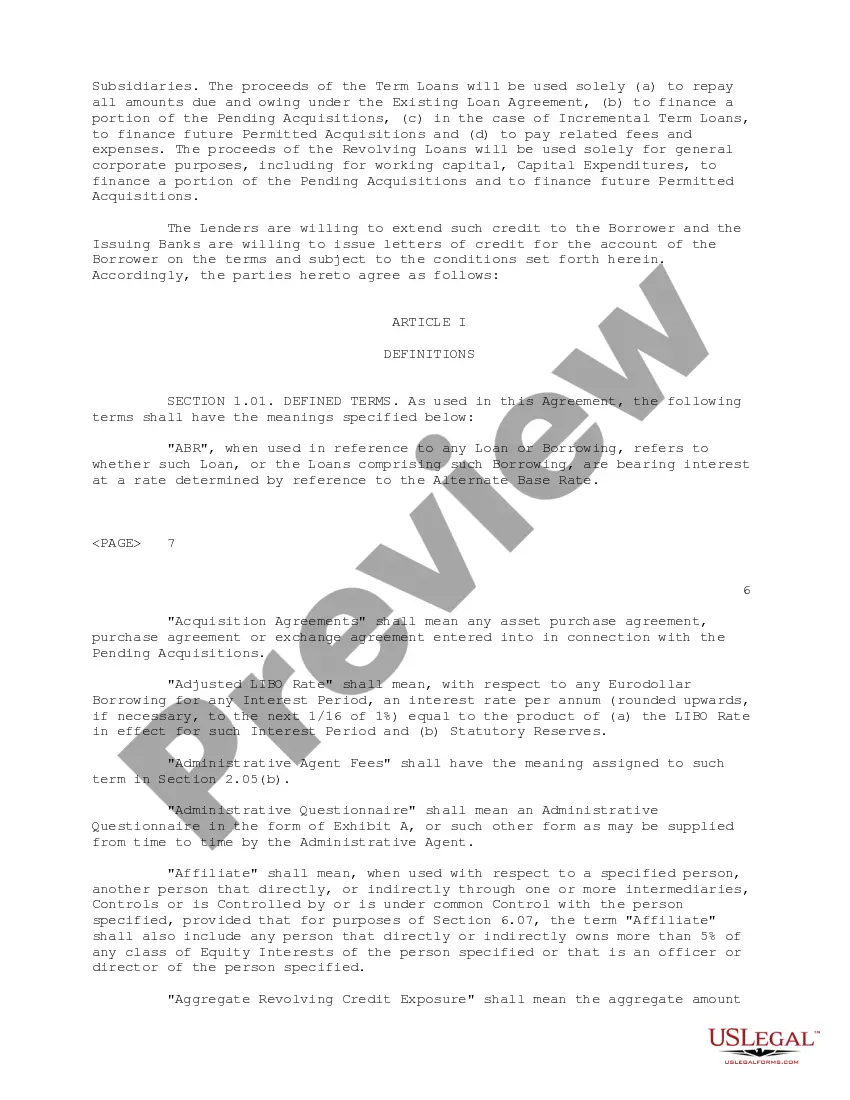

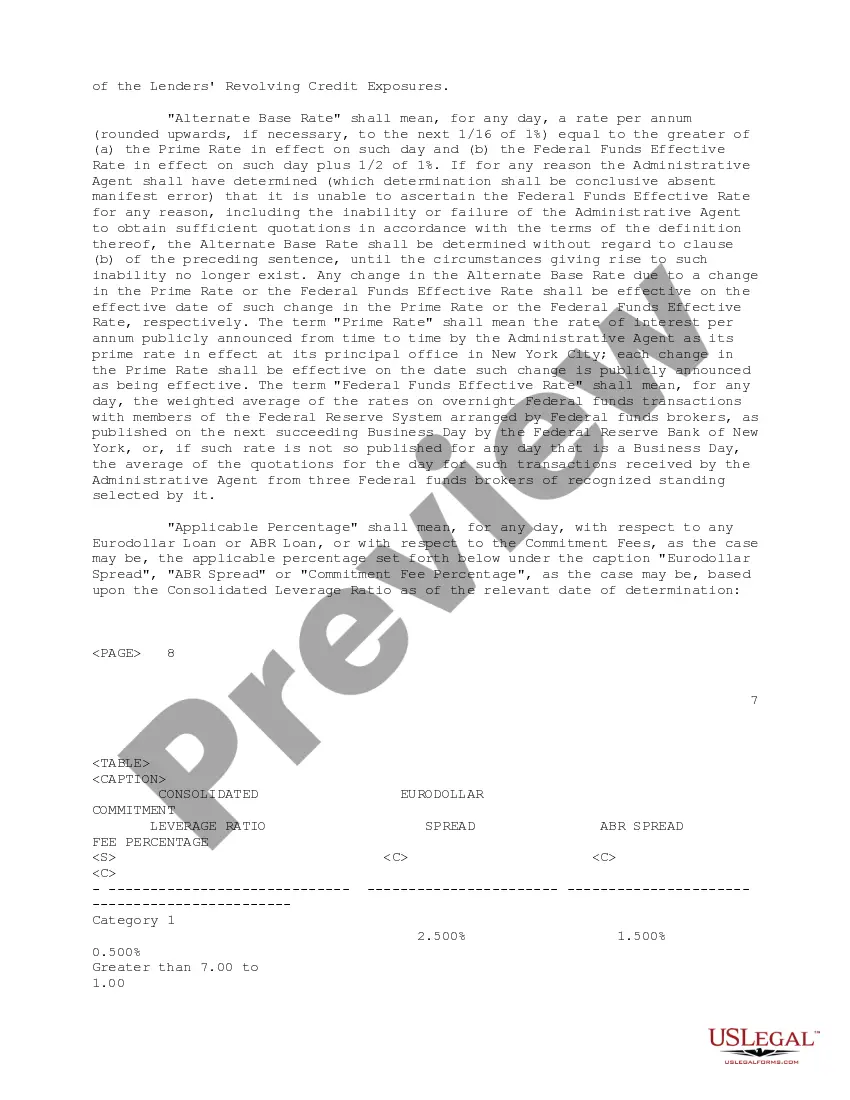

Nebraska Credit Agreement is a legal document that outlines the terms and conditions under which credit is extended to a borrower. It is a binding contract between the lender and the borrower, establishing the rights and responsibilities of both parties. This type of credit agreement is commonly used in Nebraska, and it is crucial for individuals or businesses seeking to obtain credit from a financial institution or other lending sources. It provides a framework for the extension of credit, ensuring transparency and protecting the interests of both parties involved. The Nebraska Credit Agreement typically contains various sections and provisions, including: 1. Parties involved: It clearly identifies the lender and the borrower, providing their legal names, addresses, and contact information. 2. Loan amount and interest rates: It specifies the principal amount of credit being extended and the interest rate at which the borrower will be charged. 3. Repayment terms: This section details the repayment schedule, including the frequency of payments (monthly, quarterly, etc.), the duration of the loan, and any specific terms related to early payment or prepayment penalties. 4. Collateral: If applicable, the agreement outlines any assets or collateral that the borrower pledges as security for the credit extended. This ensures that the lender has recourse in case of default. 5. Fees and charges: It discloses any fees, charges, or costs associated with the credit agreement, such as origination fees, late payment fees, or annual fees. 6. Default and remedies: This section outlines the consequences of default, including late payment, non-payment, or breach of any terms and conditions. It specifies the remedies available to the lender, such as acceleration of the entire loan, foreclosure, or repossession of collateral. 7. Governing law and jurisdiction: It defines the laws of Nebraska that govern the credit agreement and the jurisdiction where any legal disputes will be resolved. There are different types of Nebraska Credit Agreements regarding the extension of credit, each tailored to specific circumstances and entities: 1. Personal Credit Agreement: This type applies to individuals seeking personal loans or lines of credit from financial institutions or other lenders. 2. Business Credit Agreement: It encompasses credit extended to businesses, covering commercial loans, lines of credit, or trade credit. 3. Mortgage Credit Agreement: This agreement pertains specifically to real estate transactions, where credit is provided by a lender to finance the purchase or refinance of property. 4. Revolving Credit Agreement: It involves an open-ended line of credit that the borrower can access as needed, up to a predetermined limit. This type is commonly used by businesses for managing cash flow or financing short-term operational expenses. Nebraska Credit Agreements regarding the extension of credit play a vital role in protecting the rights and obligations of both borrowers and lenders. It is essential for all parties to carefully review and understand the terms before entering into such agreements to ensure a mutually beneficial and legally enforceable credit arrangement.

Nebraska Credit Agreement regarding extension of credit

Description

How to fill out Nebraska Credit Agreement Regarding Extension Of Credit?

US Legal Forms - one of several largest libraries of authorized kinds in America - delivers a wide range of authorized record templates you may obtain or printing. Using the internet site, you can find a large number of kinds for enterprise and personal reasons, categorized by groups, says, or keywords.You will find the most recent versions of kinds much like the Nebraska Credit Agreement regarding extension of credit within minutes.

If you already possess a membership, log in and obtain Nebraska Credit Agreement regarding extension of credit in the US Legal Forms library. The Down load key will appear on each type you view. You gain access to all earlier acquired kinds from the My Forms tab of your account.

If you wish to use US Legal Forms for the first time, allow me to share easy directions to help you get started:

- Be sure you have picked the best type to your area/area. Go through the Preview key to analyze the form`s articles. See the type explanation to ensure that you have selected the correct type.

- If the type doesn`t fit your requirements, take advantage of the Search field towards the top of the monitor to discover the one who does.

- If you are pleased with the shape, affirm your choice by clicking on the Purchase now key. Then, choose the rates strategy you like and give your references to sign up for an account.

- Method the deal. Use your Visa or Mastercard or PayPal account to perform the deal.

- Select the structure and obtain the shape on your own device.

- Make adjustments. Load, edit and printing and indication the acquired Nebraska Credit Agreement regarding extension of credit.

Each web template you added to your account lacks an expiry date and is also your own forever. So, if you would like obtain or printing one more copy, just proceed to the My Forms segment and then click in the type you will need.

Obtain access to the Nebraska Credit Agreement regarding extension of credit with US Legal Forms, one of the most considerable library of authorized record templates. Use a large number of expert and express-distinct templates that meet up with your organization or personal requirements and requirements.