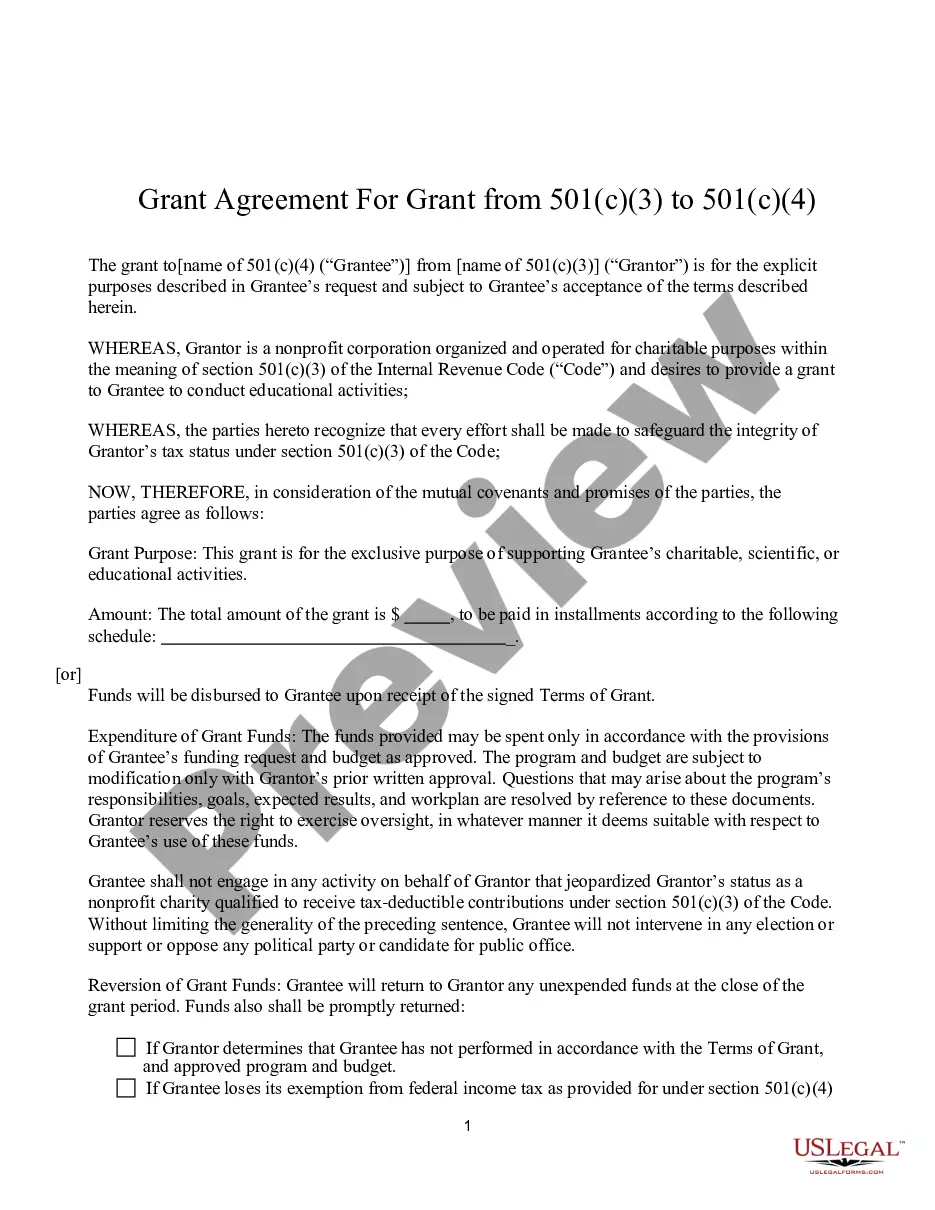

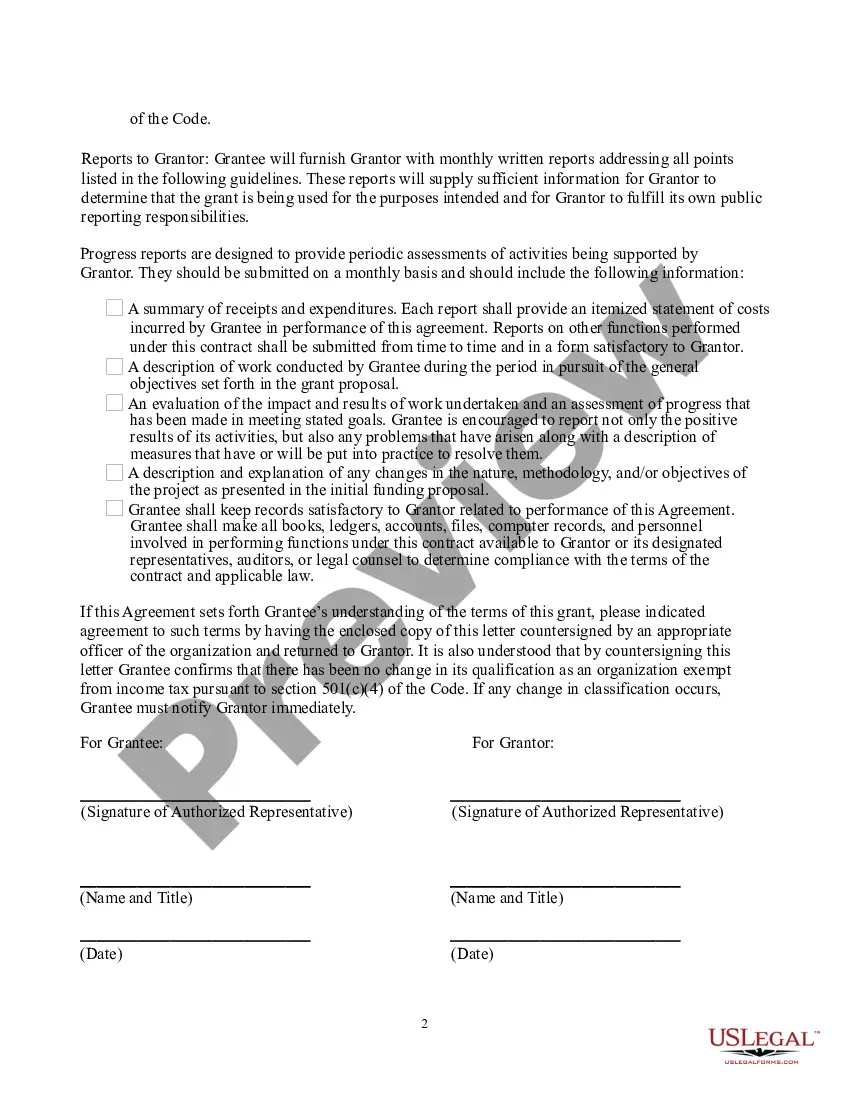

Nebraska Grant Agreement from 501(c)(3) to 501(c)(4): A Comprehensive Overview In Nebraska, a grant agreement from 501(c)(3) to 501(c)(4) refers to the process through which a nonprofit organization changes its tax-exempt status from a charitable organization (501(c)(3)) to a social welfare organization (501(c)(4)). This transition involves various legal and operational considerations and requires approval from the Internal Revenue Service (IRS). A 501(c)(3) organization is primarily designed for charitable, educational, religious, scientific, or literary purposes, whereas a 501(c)(4) organization focuses on promoting social welfare activities that benefit the community or segment of the population. While both are tax-exempt entities, the key distinction lies in the scope of their activities. To initiate the process of converting a 501(c)(3) organization to a 501(c)(4), the nonprofit must adhere to specific guidelines and regulations imposed by the IRS and the State of Nebraska. The grant agreement typically involves the following steps: 1. Assessing Eligibility: The nonprofit must determine if it meets the requirements for a 501(c)(4) organization under Nebraska law. This includes conducting activities that primarily promote social welfare and ensuring that political activities remain secondary to the organization's main purpose. 2. Internal Consensus: The nonprofit's board of directors, along with key stakeholders, should reach a consensus on the benefits and potential implications of converting to a 501(c)(4) organization. It is crucial to consider the impact on fundraising efforts, donor base, and the organization's overall mission. 3. Drafting Amendments: Once the decision is made, the organization must draft and adopt amendments to its articles of incorporation or bylaws to reflect the change in tax-exempt status. These amendments should align with Nebraska and IRS regulations and clearly outline the organization's purpose and activities under 501(c)(4). 4. Filing with IRS: The organization must submit Form 1024 to the IRS, along with applicable fees and supporting documents, such as the amended articles of incorporation or bylaws, financial statements, and a detailed description of its activities. The IRS will review the application and determine whether the organization meets the criteria for 501(c)(4) status. It's important to note that types or variations of Nebraska Grant Agreements from 501(c)(3) to 501(c)(4) may not have distinct official names or categories. However, organizations can have different motivations for seeking a change in tax-exempt status. Some common examples include: 1. Advocacy-Focused Organizations: Nonprofits aiming to engage in political activities, lobbying, and advocating for policy changes may choose to convert to a 501(c)(4) to have greater flexibility in pursuing their goals. 2. Social Welfare Initiatives: Organizations primarily dedicated to promoting social welfare activities, such as community development, economic improvement, environmental conservation, or healthcare reform, might opt for 501(c)(4) status to better align with their mission. 3. Hybrid Models: Certain nonprofits may consider establishing a parallel 501(c)(4) organization alongside their existing 501(c)(3) entity. This allows them to engage in advocacy and lobbying efforts while maintaining the tax-deductible nature of donations through the 501(c)(3). Before pursuing a transition from 501(c)(3) to 501(c)(4) in Nebraska, it is crucial for nonprofits to consult legal professionals adept in nonprofit law and seek guidance from the Nebraska Department of Revenue and the IRS to ensure compliance with all regulations.

Nebraska Grant Agreement from 501(c)(3) to 501(c)(4)

Description

How to fill out Nebraska Grant Agreement From 501(c)(3) To 501(c)(4)?

If you wish to full, obtain, or produce legitimate document templates, use US Legal Forms, the biggest variety of legitimate types, which can be found online. Make use of the site`s simple and convenient look for to get the files you want. Different templates for organization and person purposes are categorized by types and suggests, or keywords and phrases. Use US Legal Forms to get the Nebraska Grant Agreement from 501(c)(3) to 501(c)(4) in just a number of mouse clicks.

Should you be currently a US Legal Forms customer, log in to your account and click on the Obtain switch to find the Nebraska Grant Agreement from 501(c)(3) to 501(c)(4). Also you can access types you formerly downloaded in the My Forms tab of your respective account.

If you are using US Legal Forms initially, refer to the instructions listed below:

- Step 1. Be sure you have selected the shape for that proper area/region.

- Step 2. Make use of the Review method to look over the form`s content material. Don`t forget about to read the explanation.

- Step 3. Should you be unsatisfied with all the form, take advantage of the Research industry towards the top of the monitor to locate other variations of your legitimate form web template.

- Step 4. Once you have identified the shape you want, click on the Get now switch. Pick the pricing strategy you favor and put your credentials to sign up to have an account.

- Step 5. Approach the deal. You may use your credit card or PayPal account to complete the deal.

- Step 6. Choose the structure of your legitimate form and obtain it on the device.

- Step 7. Total, edit and produce or signal the Nebraska Grant Agreement from 501(c)(3) to 501(c)(4).

Each and every legitimate document web template you get is your own property permanently. You have acces to each and every form you downloaded in your acccount. Go through the My Forms portion and pick a form to produce or obtain once more.

Be competitive and obtain, and produce the Nebraska Grant Agreement from 501(c)(3) to 501(c)(4) with US Legal Forms. There are millions of professional and express-specific types you may use for your personal organization or person requires.