In real estate, a short sale occurs when a bank or mortgage lender agrees to discount a loan balance due to an economic hardship on the part of the mortgagor (i.e., the seller). Circumstances determine whether or not banks will discount a loan balance. These circumstances are usually related to the current real estate market climate and the individual borrower's financial situation. A short sale typically is executed to prevent a home foreclosure. Often a bank will choose to allow a short sale if they believe that it will result in a smaller financial loss than foreclosing.

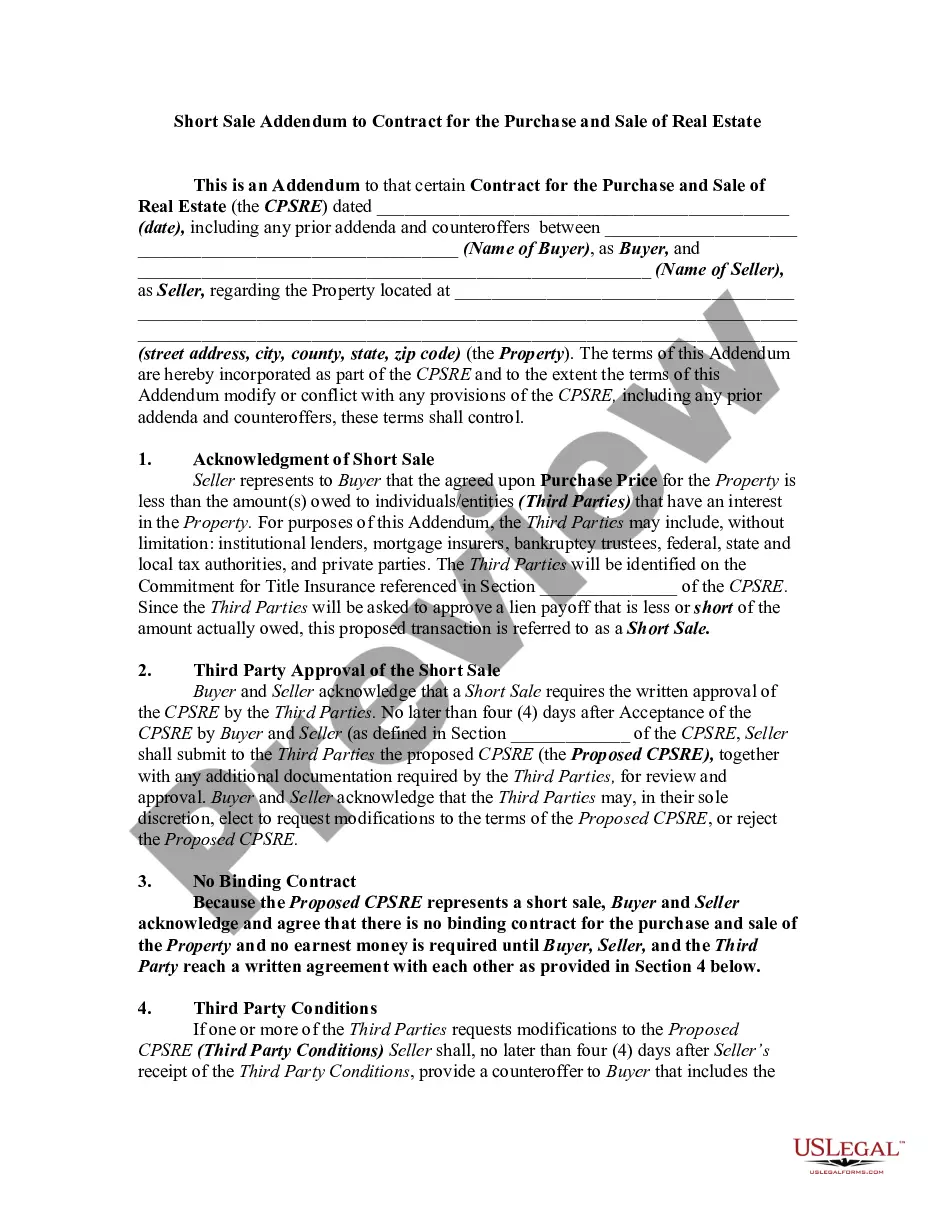

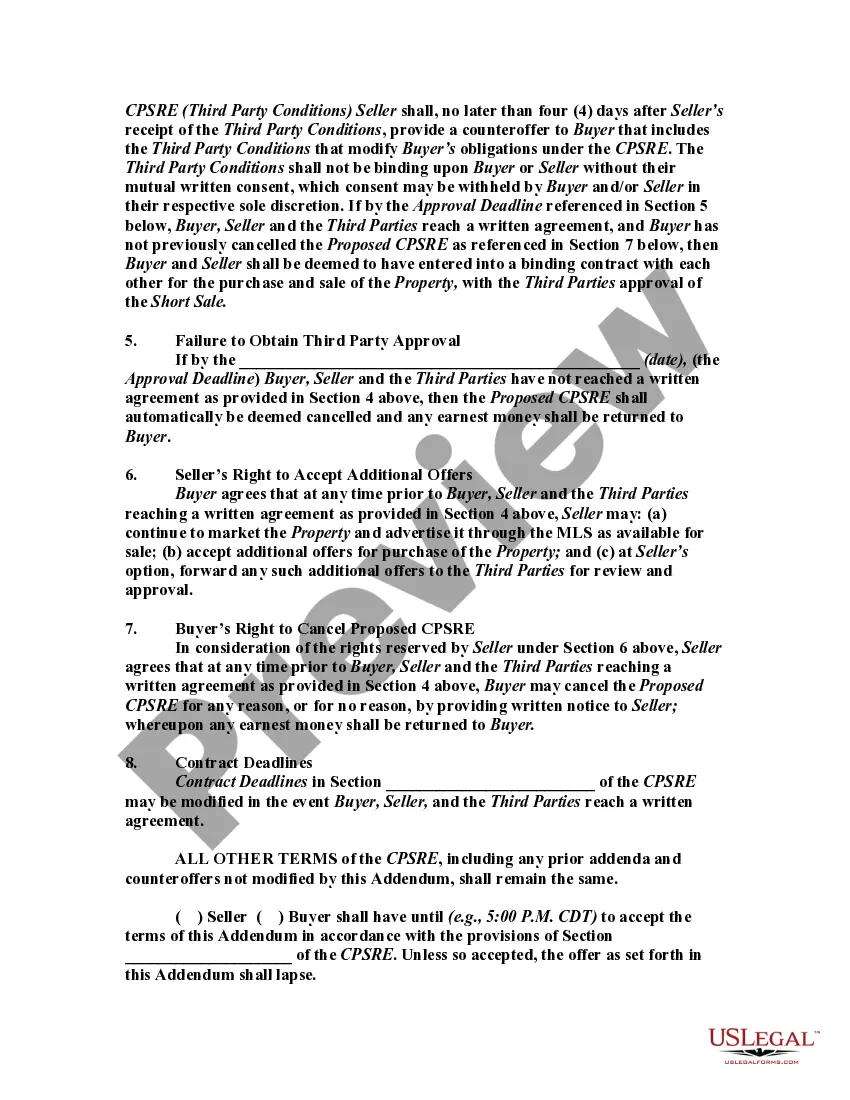

This form is a sample of an Addendum to a standard real estate sales contract in order to incorporate the short sales provisions. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The New Hampshire Short Sale Addendum to Contract for the Price, Purchase, and Sale of Real Estate is an essential document used in real estate transactions involving short sales in the state of New Hampshire. This addendum is designed to address specific conditions and terms related to short sales, ensuring a smooth and legally sound transaction for both the buyer and the seller. 1. Purpose: The purpose of the New Hampshire Short Sale Addendum is to modify and supplement the terms of the standard real estate purchase and sale agreement to accommodate the unique circumstances of a short sale. 2. Importance: Short sales involve selling a property for less than what the owner owes on their mortgage. As such, the New Hampshire Short Sale Addendum is crucial in outlining important provisions that protect the interests of both parties involved in the transaction. 3. Types of New Hampshire Short Sale Addendum: a. Standard Short Sale Addendum: This is the primary and most commonly used version of the addendum. It outlines the general terms and conditions surrounding the short sale, including provisions regarding lender approval, buyer concessions, and timelines for completing the transaction. b. Specialized Addendum for Mortgage Approval: In certain cases, a lender may require additional documentation and assurances from the buyer to approve the short sale. This specialized addendum outlines the specific conditions and requirements imposed by the lender before they grant their approval. c. Seller's Financial Disclosure Addendum: This addendum is used to obtain detailed financial information from the seller, including their income, assets, and liabilities. It helps the buyer and the lender assess the seller's financial situation and determine the feasibility of the short sale. d. Inspection Contingency Addendum: Since short sales often involve properties in distressed conditions, this addendum allows the buyer to conduct inspections and includes provisions for addressing any repair or maintenance issues that may arise. 4. Key Elements: The New Hampshire Short Sale Addendum typically includes the following key elements: a. Lender Approval Clause: Establishes that the sale is contingent upon the lender's approval of the short sale transaction. b. Negotiation Period: Specifies the timeframe within which the seller may negotiate with the lender to obtain approval for the short sale. c. Buyer Concessions: Outlines any special concessions the buyer is willing to make to facilitate the short sale, such as paying for certain closing costs or assuming responsibility for outstanding liens or repairs. d. Seller's Representations and Warranties: Requires the seller to provide accurate and complete information about the property and their financial situation. e. Termination Rights: Provides termination rights for both parties, allowing them to cancel the contract if certain conditions are not met. f. Closing Extension: Addresses the possibility of an extended closing timeline due to lender requirements or unforeseen circumstances. In summary, the various types of New Hampshire Short Sale Addendums to Contract for the Price, Purchase, and Sale of Real Estate serve to protect the interests of both buyers and sellers involved in short sale transactions. These addendums ensure that the unique conditions of short sales are properly accounted for, facilitating a smoother and more secure real estate transaction in New Hampshire.The New Hampshire Short Sale Addendum to Contract for the Price, Purchase, and Sale of Real Estate is an essential document used in real estate transactions involving short sales in the state of New Hampshire. This addendum is designed to address specific conditions and terms related to short sales, ensuring a smooth and legally sound transaction for both the buyer and the seller. 1. Purpose: The purpose of the New Hampshire Short Sale Addendum is to modify and supplement the terms of the standard real estate purchase and sale agreement to accommodate the unique circumstances of a short sale. 2. Importance: Short sales involve selling a property for less than what the owner owes on their mortgage. As such, the New Hampshire Short Sale Addendum is crucial in outlining important provisions that protect the interests of both parties involved in the transaction. 3. Types of New Hampshire Short Sale Addendum: a. Standard Short Sale Addendum: This is the primary and most commonly used version of the addendum. It outlines the general terms and conditions surrounding the short sale, including provisions regarding lender approval, buyer concessions, and timelines for completing the transaction. b. Specialized Addendum for Mortgage Approval: In certain cases, a lender may require additional documentation and assurances from the buyer to approve the short sale. This specialized addendum outlines the specific conditions and requirements imposed by the lender before they grant their approval. c. Seller's Financial Disclosure Addendum: This addendum is used to obtain detailed financial information from the seller, including their income, assets, and liabilities. It helps the buyer and the lender assess the seller's financial situation and determine the feasibility of the short sale. d. Inspection Contingency Addendum: Since short sales often involve properties in distressed conditions, this addendum allows the buyer to conduct inspections and includes provisions for addressing any repair or maintenance issues that may arise. 4. Key Elements: The New Hampshire Short Sale Addendum typically includes the following key elements: a. Lender Approval Clause: Establishes that the sale is contingent upon the lender's approval of the short sale transaction. b. Negotiation Period: Specifies the timeframe within which the seller may negotiate with the lender to obtain approval for the short sale. c. Buyer Concessions: Outlines any special concessions the buyer is willing to make to facilitate the short sale, such as paying for certain closing costs or assuming responsibility for outstanding liens or repairs. d. Seller's Representations and Warranties: Requires the seller to provide accurate and complete information about the property and their financial situation. e. Termination Rights: Provides termination rights for both parties, allowing them to cancel the contract if certain conditions are not met. f. Closing Extension: Addresses the possibility of an extended closing timeline due to lender requirements or unforeseen circumstances. In summary, the various types of New Hampshire Short Sale Addendums to Contract for the Price, Purchase, and Sale of Real Estate serve to protect the interests of both buyers and sellers involved in short sale transactions. These addendums ensure that the unique conditions of short sales are properly accounted for, facilitating a smoother and more secure real estate transaction in New Hampshire.