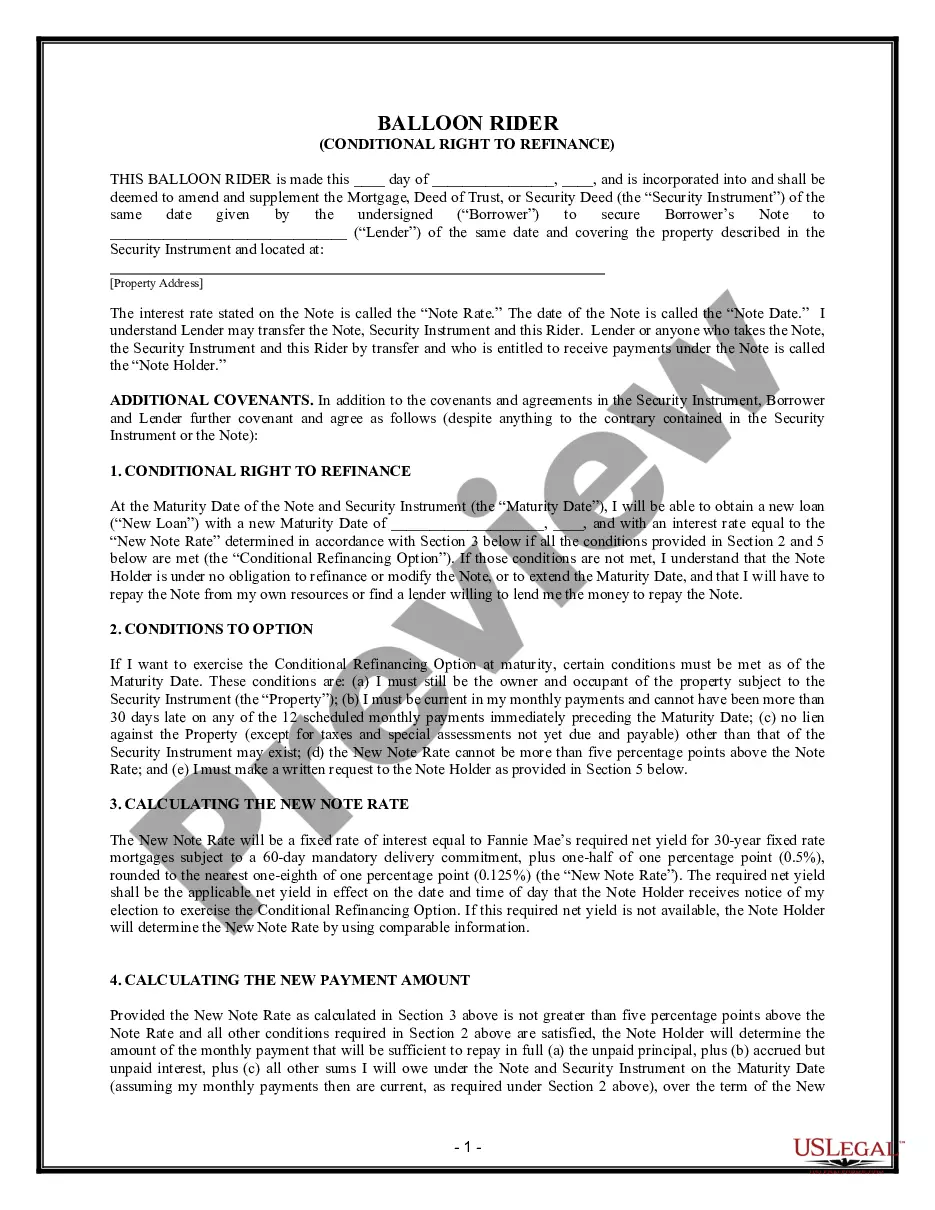

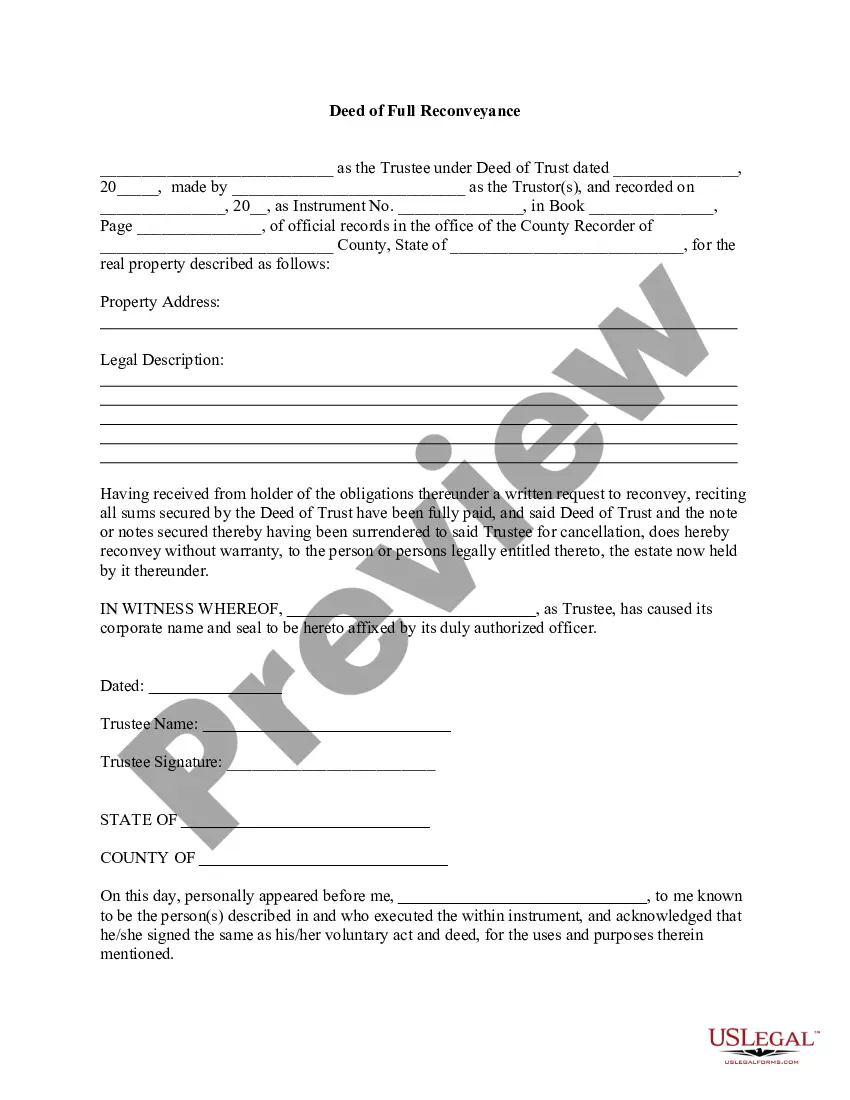

A balloon payment is the final payment needed to satisfy the payment of the entire principal amount due on a note, if different from the monthly payment. It is a lump-sum principal payment due at the end of a loan. For example, a loan may have monthly payments as if the principal amount were amortized over thirty (30), but a balloon payment could be due at the end of fifteen (15) years, at which time the loan would have to be paid in full or refinanced.

Some states may require that the balloon mortgage clause appear in bold or upper case typeface. It is placed at the top of the first page and again directly above the signature lines. The clause might be required when the final payment or principal balance due at maturity is greater than twice the amount of the regular monthly or periodic payment. A different statutory clause may be required when the note has a variable or adjustable interest rate. Failure to include the clause may result in an automatic extension of the maturity date of the mortgage.