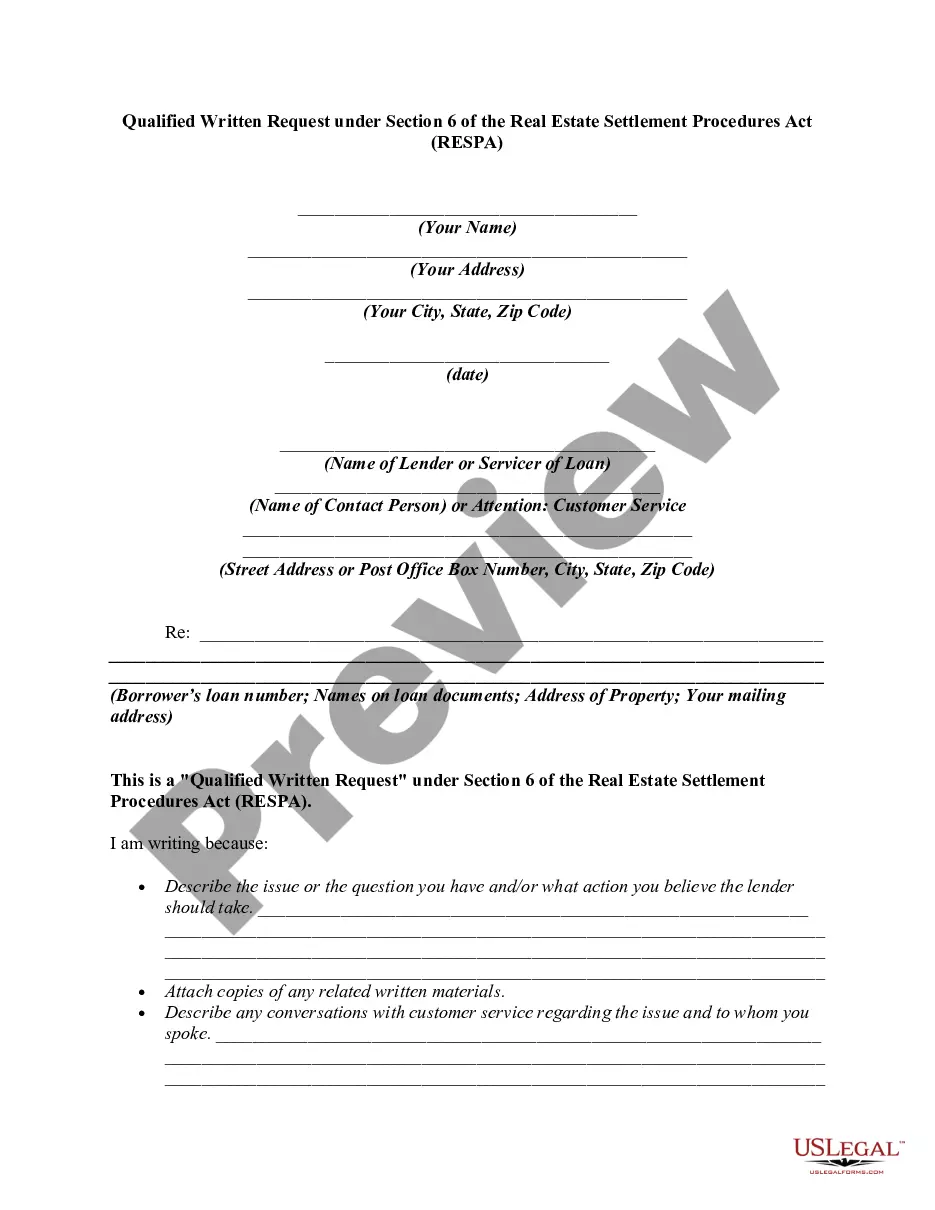

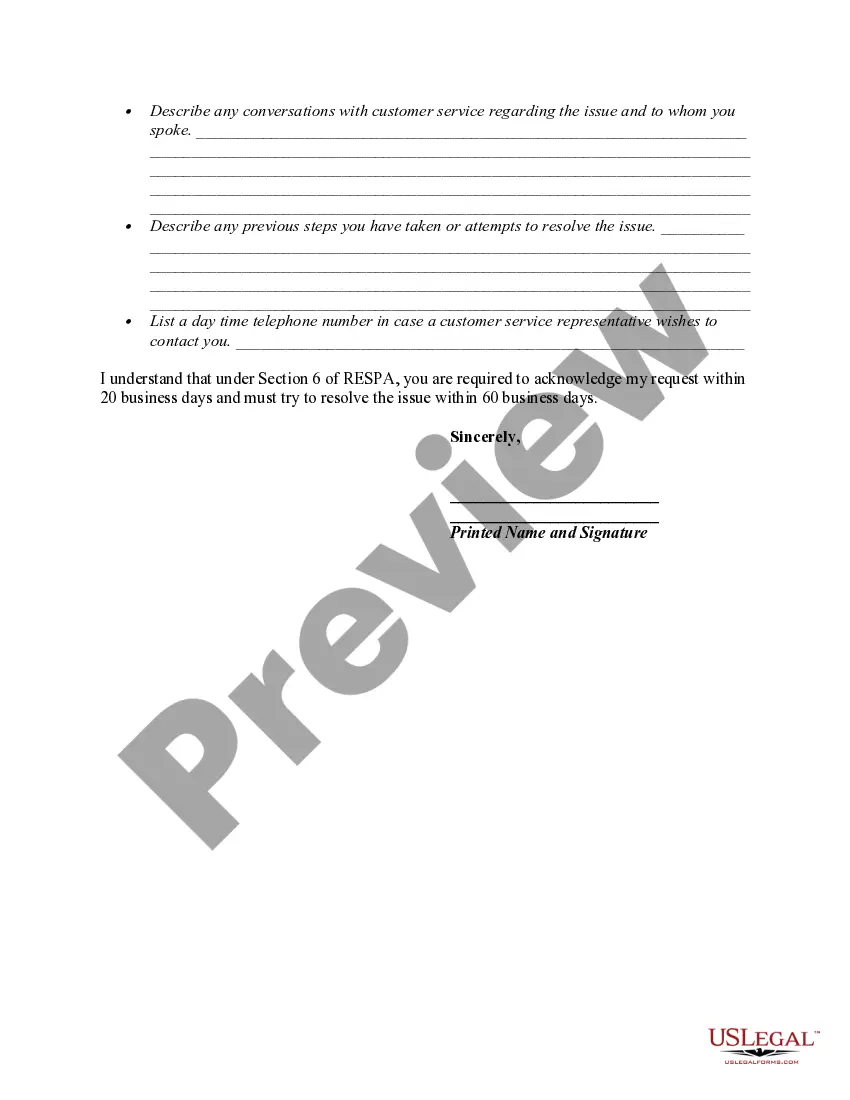

12 USC 2605(e) creates a duty of a loan servicer to respond to the inquiries of borrowers regarding loans covered by RESPA. If the borrower believes there is an error in the mortgage account, he or she can make a "qualified written request" to the loan servicer. The request must be in writing, identify the borrower by name and account, and include a statement of reasons why the borrower believes the account is in error. The request should include the words "qualified written request". It cannot be written on the payment coupon, but must be on a separate piece of paper. The Department of Housing and Urban Development provides a sample letter.

The servicer must acknowledge receipt of the request within 20 days. The servicer then has 60 days (from the request) to take action on the request. The servicer has to either provide a written notification that the error has been corrected, or provide a written explanation as to why the servicer believes the account is correct. Either way, the servicer has to provide the name and telephone number of a person with whom the borrower can discuss the matter.

A New Hampshire Qualified Written Request (BWR) is a formal request made by a borrower to a loan service, lender, or mortgage loan originator regarding the servicing of their mortgage loan that falls under Section 6 of the Real Estate Settlement Procedures Act (RESP). The BWR aims to obtain specific information, resolve issues related to the loan, or address any potential violations committed by the loan service or lender. Under RESP, Section 6 provides borrowers with the right to request information, clarification, or resolution regarding their mortgage loan. To initiate a New Hampshire BWR, the borrower must submit a written request to the loan service. This request must contain certain information to be considered valid, including the borrower's name, the account information, a statement of the requested information or explanation sought, and any supporting documents or evidence. The New Hampshire BWR serves as a powerful tool for borrowers in dealing with potential loan servicing errors, disputes, or other mortgage-related issues. By submitting a BWR, borrowers can request clarification on any discrepancies, challenge incorrect charges, seek assistance in modifying their loan, or raise concerns about the foreclosure process, among others. There are no specific types of New Hampshire BWR outlined within Section 6 of RESP. Instead, the nature and content of the BWR will vary based on the borrower's specific concerns and objectives. Some common types of issues addressed in a BWR may include: 1. Request for Escrow Account Information: The borrower may seek clarification regarding the calculation or use of funds in their escrow account, such as insurance premiums and property taxes. 2. Documentation and Billing Discrepancies: Borrowers may challenge inconsistencies in billing statements, installment amounts, or interest rates applied to the loan. They may request detailed documentation to support such charges. 3. Loan Modification Requests: An individual facing financial hardship may utilize a BWR to inquire about the loan modification options available to them or to challenge a loan modification denial. 4. Foreclosure Process Inquiries: If facing imminent foreclosure, borrowers can utilize the BWR to request information regarding the foreclosure process's timeline, status, or potential alternatives to foreclosure. 5. General Loan Servicing Concerns: Borrowers may have various concerns, including errors in crediting payments, misapplication of funds, or failures to respond to previous inquiries or requests. It is important to note that the specific requirements and procedures for submitting a New Hampshire BWR may vary, and borrowers are advised to consult legal counsel or resources such as the Consumer Financial Protection Bureau (CFPB) for detailed guidance. However, by submitting a well-crafted BWR, borrowers can avail themselves of important consumer protections under RESP and potentially resolve issues related to their mortgage loan effectively.

A New Hampshire Qualified Written Request (BWR) is a formal request made by a borrower to a loan service, lender, or mortgage loan originator regarding the servicing of their mortgage loan that falls under Section 6 of the Real Estate Settlement Procedures Act (RESP). The BWR aims to obtain specific information, resolve issues related to the loan, or address any potential violations committed by the loan service or lender. Under RESP, Section 6 provides borrowers with the right to request information, clarification, or resolution regarding their mortgage loan. To initiate a New Hampshire BWR, the borrower must submit a written request to the loan service. This request must contain certain information to be considered valid, including the borrower's name, the account information, a statement of the requested information or explanation sought, and any supporting documents or evidence. The New Hampshire BWR serves as a powerful tool for borrowers in dealing with potential loan servicing errors, disputes, or other mortgage-related issues. By submitting a BWR, borrowers can request clarification on any discrepancies, challenge incorrect charges, seek assistance in modifying their loan, or raise concerns about the foreclosure process, among others. There are no specific types of New Hampshire BWR outlined within Section 6 of RESP. Instead, the nature and content of the BWR will vary based on the borrower's specific concerns and objectives. Some common types of issues addressed in a BWR may include: 1. Request for Escrow Account Information: The borrower may seek clarification regarding the calculation or use of funds in their escrow account, such as insurance premiums and property taxes. 2. Documentation and Billing Discrepancies: Borrowers may challenge inconsistencies in billing statements, installment amounts, or interest rates applied to the loan. They may request detailed documentation to support such charges. 3. Loan Modification Requests: An individual facing financial hardship may utilize a BWR to inquire about the loan modification options available to them or to challenge a loan modification denial. 4. Foreclosure Process Inquiries: If facing imminent foreclosure, borrowers can utilize the BWR to request information regarding the foreclosure process's timeline, status, or potential alternatives to foreclosure. 5. General Loan Servicing Concerns: Borrowers may have various concerns, including errors in crediting payments, misapplication of funds, or failures to respond to previous inquiries or requests. It is important to note that the specific requirements and procedures for submitting a New Hampshire BWR may vary, and borrowers are advised to consult legal counsel or resources such as the Consumer Financial Protection Bureau (CFPB) for detailed guidance. However, by submitting a well-crafted BWR, borrowers can avail themselves of important consumer protections under RESP and potentially resolve issues related to their mortgage loan effectively.