Gift taxes are taxes that supplement the Estate Tax. Gift taxes are placed on gifts given away to any person while you are still living, so that you may not avoid estate taxes by making gifts of your estate. You may give up to $12,000 a year in cash or assets to an unlimited number of people each year without incurring gift tax liability, but the gifts must have no conditions attached. Married couples can give, as a couple, a $24,000 gift per year to as many people as they want. Under federal tax law, gifts totaling more than $12,000 to one person in one year are considered a taxable gift and generate a potential gift tax. It does not matter if you give one $13,000 gift or 13 gifts of $1,000 each, or one gift of $12,000 and a "birthday gift" of $1,000.

Gifts beyond the $12,000 limit (there is an exception for gifts that are directly paid by the gift giver for tuition and medical expenses) are considered "taxable gifts." Taxable gifts create liability for a gift tax. But gift tax is not due to be paid until you give away over $1,000,000 in your lifetime.

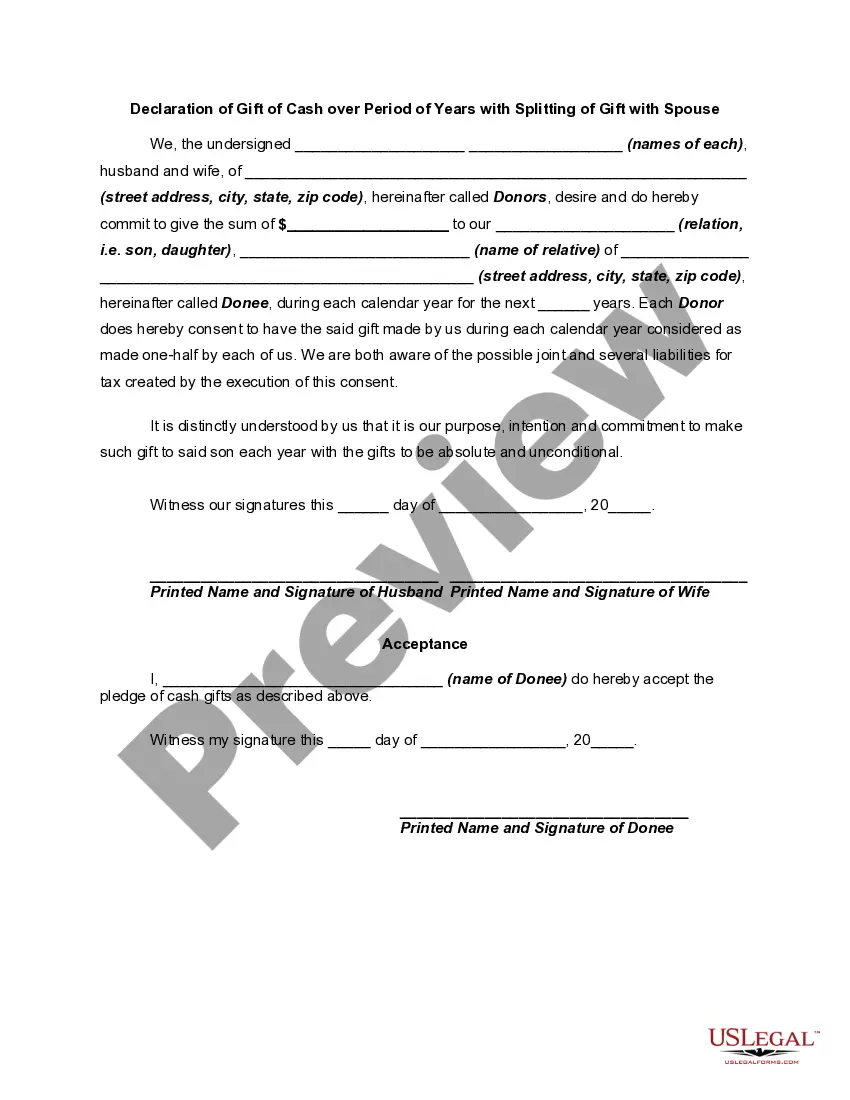

The New Hampshire Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document that allows an individual to donate a specific cash amount to another person or organization over a period of years while splitting the gift with their spouse. This declaration ensures that the gift is given in a structured manner and provides clarity on both the timeline and distribution of funds. Keyword: New Hampshire Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse There are several types of New Hampshire Declarations of Gift of Cash over Period of Years with Splitting of Gift with Spouse, depending on the specific circumstances and intentions of the donor. Some variations include: 1. Irrevocable Declaration of Gift: An irrevocable declaration of gift of cash over a period of years with splitting of gift with a spouse is a binding agreement that cannot be reversed or modified once it is signed. This type of declaration is often used when the donor wants to ensure that the gift is given as intended and cannot be altered later on. 2. Revocable Declaration of Gift: A revocable declaration of gift of cash over a period of years with splitting of gift with a spouse allows the donor to modify or revoke the declaration at any time before the gift is fully given. This type of declaration provides flexibility if circumstances change, but it also requires continuous involvement from the donor. 3. Charitable Declaration of Gift: A charitable declaration of gift of cash over a period of years with splitting of gift with a spouse is specifically designed for individuals who want to donate to a charitable organization. This type of declaration typically includes additional provisions related to tax deductions and ensures that the gift is used for charitable purposes. 4. Family Declaration of Gift: A family declaration of gift of cash over a period of years with splitting of gift with a spouse is often used when the donor wants to provide financial support to their family members. This type of declaration can outline specific conditions, such as educational expenses or medical bills, that the gift should cover. In conclusion, the New Hampshire Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a versatile legal document that allows individuals to donate a specific cash amount over time while sharing the gift with their spouse. Different types of declarations exist to accommodate various intentions and circumstances, including irrevocable or revocable declarations, charitable declarations, and family declarations. Consulting with a legal professional is recommended to ensure that the declaration aligns with the donor's objectives and adheres to all applicable laws and regulations.