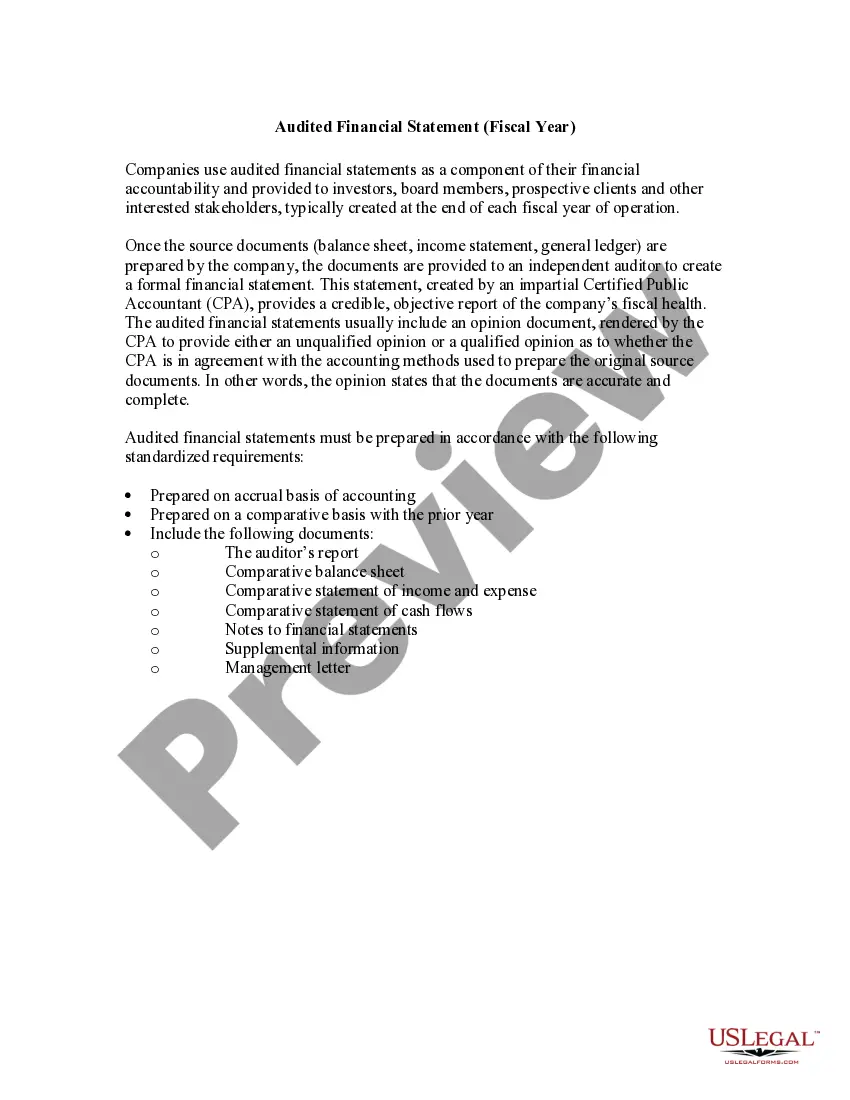

As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

New Hampshire Report of Independent Accountants after Audit of Financial Statements

Category:

State:

Multi-State

Control #:

US-01939BG

Format:

Word

Instant download

Description

How to fill out Report Of Independent Accountants After Audit Of Financial Statements?

If you need to extensive, acquire, or print out sanctioned document templates, utilize US Legal Forms, the leading source of legal forms, accessible online.

Leverage the website's straightforward and convenient search to obtain the documents you require. Various templates for business and personal purposes are categorized by types and jurisdictions, or keywords.

Use US Legal Forms to obtain the New Hampshire Report of Independent Accountants after Audit of Financial Statements with just a few clicks.

Every legal document template you purchase belongs to you permanently. You have access to every form you downloaded in your account. Click the My documents section and select a form to print or download again.

Stay ahead and obtain, and print the New Hampshire Report of Independent Accountants after Audit of Financial Statements with US Legal Forms. There are millions of professional and state-specific forms available for your business or personal needs.

- If you are currently a US Legal Forms subscriber, sign in to your account and select the Obtain option to locate the New Hampshire Report of Independent Accountants after Audit of Financial Statements.

- You may also find forms you have previously downloaded in the My documents section of your account.

- If you are utilizing US Legal Forms for the first time, follow the guidelines below.

- Step 1. Ensure you have chosen the form for the correct city/state.

- Step 2. Use the Review option to check the form's details. Don't forget to read the description.

- Step 3. If you are unsatisfied with the form, use the Search box at the top of the screen to find alternative versions of the legal form style.

- Step 4. After locating the form you desire, click the Acquire now button. Choose the payment plan you prefer and provide your information to create an account.

- Step 5. Process the transaction. You can use your credit card or PayPal account to complete the payment.

- Step 6. Locate the format of the legal form and download it to your device.

- Step 7. Complete, edit, and print or sign the New Hampshire Report of Independent Accountants after Audit of Financial Statements.

Form popularity

FAQ

Yes, audited financial statements are classified as public information. This means they can be available to shareholders, investors, and the general public, allowing for informed decision-making. The New Hampshire Report of Independent Accountants after Audit of Financial Statements ensures that this information is presented clearly, helping to promote transparency and accountability in business practices.

Financial statements must be independently reviewed when a company is required to meet regulatory standards or when seeking external financing. Such reviews provide an added layer of credibility, ensuring stakeholders that the numbers are accurate and reliable. In New Hampshire, the Report of Independent Accountants after Audit of Financial Statements showcases this independent assessment, underlining the integrity of the financial data.

You can check audited financial statements through several channels, including company websites, financial databases, and regulatory agencies. Many companies publish these statements as part of their annual reports. Additionally, platforms like US Legal Forms provide convenient access to templates and guidance on how to create compliant financial statements, including the New Hampshire Report of Independent Accountants after Audit of Financial Statements.

Most companies looking to go public need at least three years of audited financial statements. These years must reflect a consistent recording and reporting of financial data to instill investor confidence. The New Hampshire Report of Independent Accountants after Audit of Financial Statements is essential during this period, providing transparency and verifiable financial history. Having these statements ready can ease the initial public offering process significantly.

Yes, financial accounting reports are typically audited by Certified Public Accountants (CPAs). These professionals bring expertise to review and verify the accuracy of financial information. This process is critical to ensure compliance with regulations and to enhance the credibility of the reports. Consequently, a reliable New Hampshire Report of Independent Accountants after Audit of Financial Statements will reflect the findings of the CPA's evaluation.

Yes, audited financial statements are generally considered public documents. In New Hampshire, these statements may be accessed by interested parties, including investors and creditors, as they provide crucial information regarding a company's financial health. Organizations are encouraged to publish their audited financials to promote transparency and build trust. This is particularly relevant for the New Hampshire Report of Independent Accountants after Audit of Financial Statements.

Financial statements should be reviewed at least annually, but more frequent reviews are advisable for organizations with complex financial situations. Regular reviews help ensure that the New Hampshire Report of Independent Accountants after Audit of Financial Statements reflects accurate and updated information. This proactive approach also assists in compliance and risk management. Our platform offers tools to facilitate ongoing financial statement reviews, making the process smooth and effective.

The purpose of the independent review is to provide a verified opinion on the financial statements' reliability. This review helps organizations identify any discrepancies and address issues promptly. It supports the objectives of the New Hampshire Report of Independent Accountants after Audit of Financial Statements, fostering transparency and credibility. Choosing our platform can enhance your review experience, making it comprehensive and efficient.

An independent review should be conducted regularly, especially before major financial events such as mergers or fundraising. Additionally, it is advisable to conduct these reviews annually to maintain compliance and build trust with stakeholders. Keeping the New Hampshire Report of Independent Accountants after Audit of Financial Statements updated is crucial for accurate representation. Our platform can help schedule and manage reviews effectively, ensuring you stay ahead.

To complete an audit report, the auditor must gather and evaluate evidence regarding the financial statements. This process involves planning, conducting fieldwork, and assessing the internal controls of the organization. Ultimately, it's about forming an opinion that aligns with the New Hampshire Report of Independent Accountants after Audit of Financial Statements. With our services, you can navigate report completion efficiently, ensuring all necessary components are addressed.