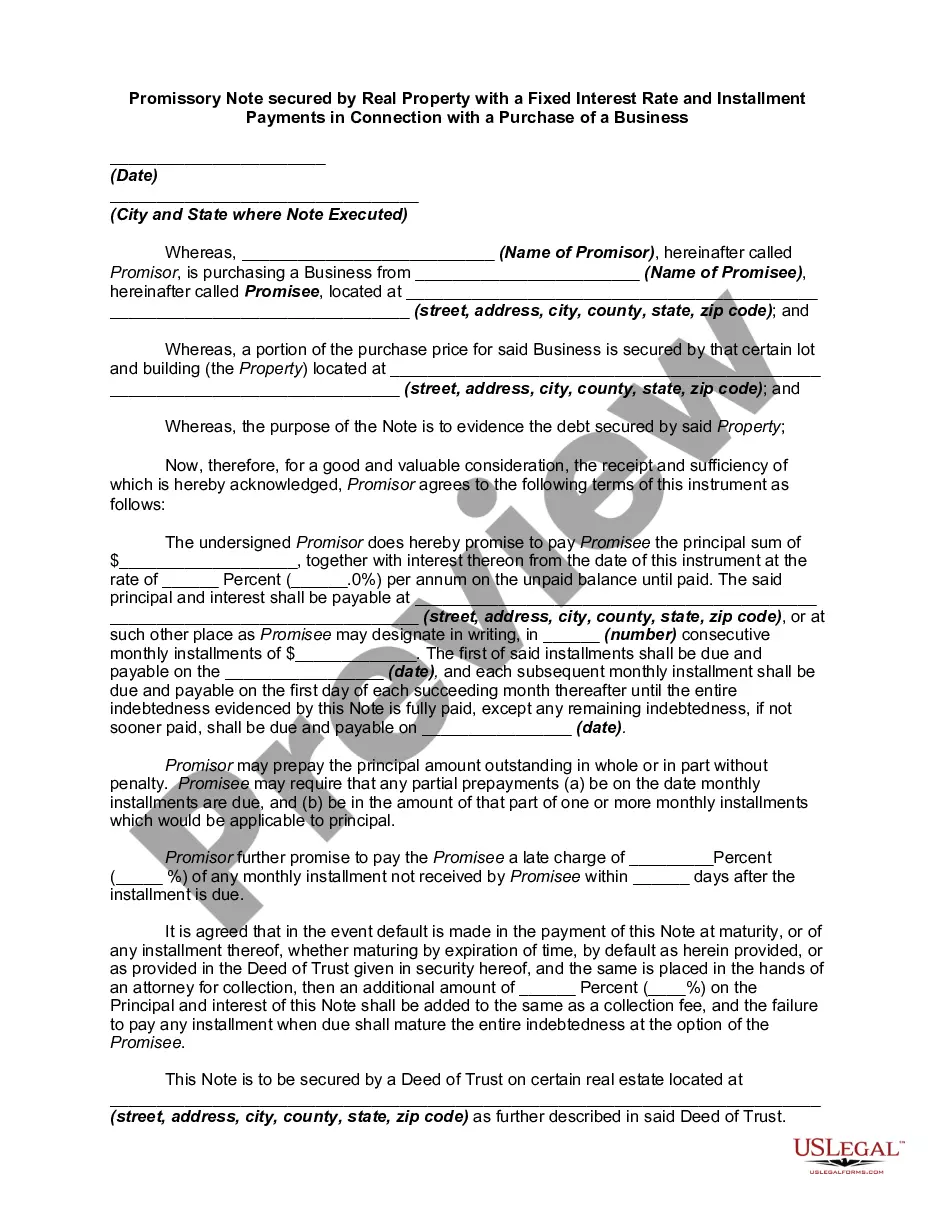

A promissory note is a written promise to pay a debt. An unconditional promise to pay on demand or at a fixed or determined future time a particular sum of money to or to the order of a specified person A promissory note should have several essential elements, including the amount of the loan, the date by which it is to be paid back, the interest rate, and a record of any collateral that is being used to secure the loan. Default terms (what happens if a payment is missed or the loan is not paid off by its due date) should also be spelled out in the promissory note.

A New Hampshire Promissory Note secured by Real Property with a Fixed Interest Rate and Installment Payments in Connection with a Purchase of a Business is a legal document that outlines the terms and conditions of a loan agreement made between a lender and a borrower in the state of New Hampshire. This type of promissory note is specifically used when the loan is secured by real property and is tied to the purchase of a business. In this type of promissory note, the borrower agrees to repay the loan through periodic installment payments over a specified period of time. The interest rate is fixed, meaning it remains constant throughout the entire loan term, providing stability and predictability for both parties involved. The real property serves as collateral for the loan, providing the lender with a security interest in the property. This means that if the borrower defaults on the loan, the lender has the right to foreclose on the property and sell it in order to recover the outstanding loan amount. Different types of New Hampshire Promissory Note secured by Real Property with a Fixed Interest Rate and Installment Payments in Connection with a Purchase of a Business may include variations in the loan term, the interest rate, and the specific details of the purchase agreement. Some examples include: 1. Short-term fixed installment promissory note: This type of promissory note may have a relatively short loan term, typically ranging from one to five years. The interest rate and installment payments are fixed throughout the loan term. 2. Long-term fixed installment promissory note: This type of promissory note extends the loan term beyond five years and may be suitable for larger loan amounts or more complex business purchases. The interest rate and installment payments remain fixed throughout the loan term. 3. Balloon payment promissory note: This type of promissory note involves smaller periodic payments throughout the loan term, with a larger lump sum payment, known as a balloon payment, due at the end of the loan term. 4. Adjustable rate promissory note: In contrast to a fixed interest rate, an adjustable rate promissory note includes an interest rate that may change over the loan term, typically based on an index such as the prime rate. The installment payments may adjust accordingly as well. It is crucial for both the lender and the borrower to carefully review and understand the terms and conditions outlined in the New Hampshire Promissory Note secured by Real Property with a Fixed Interest Rate and Installment Payments in Connection with a Purchase of a Business. Consulting with legal professionals familiar with New Hampshire laws regarding real estate transactions and business purchases can help ensure compliance and protect the interests of both parties involved.A New Hampshire Promissory Note secured by Real Property with a Fixed Interest Rate and Installment Payments in Connection with a Purchase of a Business is a legal document that outlines the terms and conditions of a loan agreement made between a lender and a borrower in the state of New Hampshire. This type of promissory note is specifically used when the loan is secured by real property and is tied to the purchase of a business. In this type of promissory note, the borrower agrees to repay the loan through periodic installment payments over a specified period of time. The interest rate is fixed, meaning it remains constant throughout the entire loan term, providing stability and predictability for both parties involved. The real property serves as collateral for the loan, providing the lender with a security interest in the property. This means that if the borrower defaults on the loan, the lender has the right to foreclose on the property and sell it in order to recover the outstanding loan amount. Different types of New Hampshire Promissory Note secured by Real Property with a Fixed Interest Rate and Installment Payments in Connection with a Purchase of a Business may include variations in the loan term, the interest rate, and the specific details of the purchase agreement. Some examples include: 1. Short-term fixed installment promissory note: This type of promissory note may have a relatively short loan term, typically ranging from one to five years. The interest rate and installment payments are fixed throughout the loan term. 2. Long-term fixed installment promissory note: This type of promissory note extends the loan term beyond five years and may be suitable for larger loan amounts or more complex business purchases. The interest rate and installment payments remain fixed throughout the loan term. 3. Balloon payment promissory note: This type of promissory note involves smaller periodic payments throughout the loan term, with a larger lump sum payment, known as a balloon payment, due at the end of the loan term. 4. Adjustable rate promissory note: In contrast to a fixed interest rate, an adjustable rate promissory note includes an interest rate that may change over the loan term, typically based on an index such as the prime rate. The installment payments may adjust accordingly as well. It is crucial for both the lender and the borrower to carefully review and understand the terms and conditions outlined in the New Hampshire Promissory Note secured by Real Property with a Fixed Interest Rate and Installment Payments in Connection with a Purchase of a Business. Consulting with legal professionals familiar with New Hampshire laws regarding real estate transactions and business purchases can help ensure compliance and protect the interests of both parties involved.