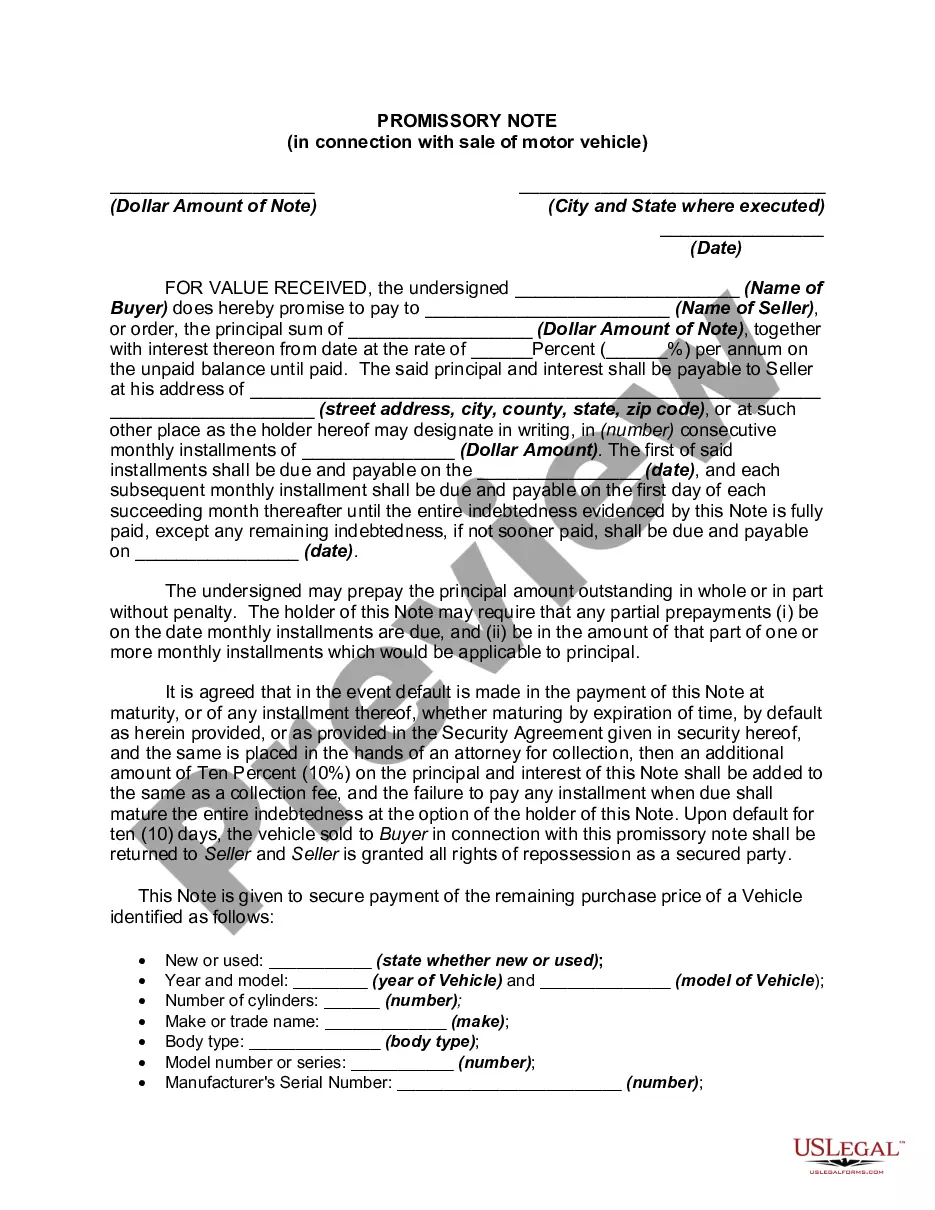

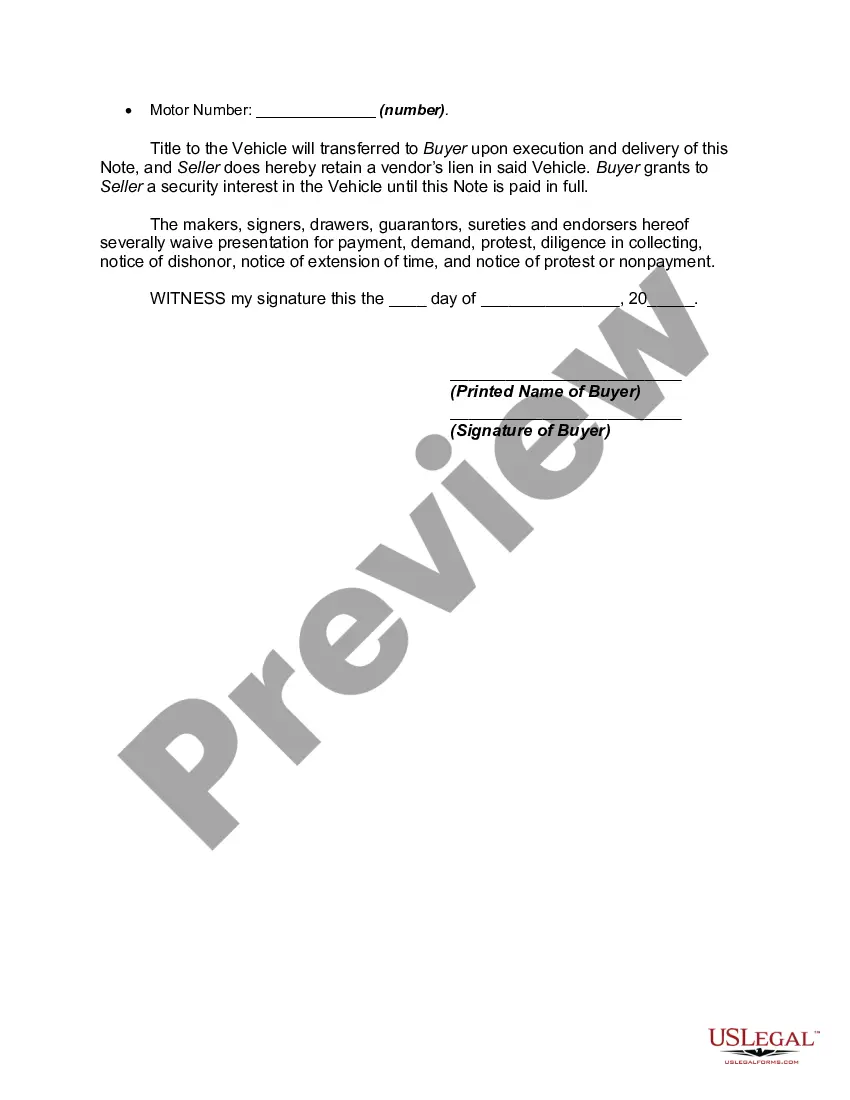

A New Hampshire Promissory Note in Connection with the Sale of a Motor Vehicle is a legally binding document that establishes an agreement between a buyer and a seller for the purchase of a motor vehicle. This note outlines the terms and conditions of the sale, including the purchase price, payment terms, and consequences of defaulting on the payment. The New Hampshire Promissory Note serves as evidence of the buyer's promise to repay the seller in full for the vehicle within a specified timeframe. It protects both parties' interests and helps ensure a smooth and transparent transaction. Keywords: New Hampshire, Promissory Note, Sale of Motor Vehicle, buyer, seller, purchase price, payment terms, defaulting, repayment, specified timeframe, transaction. Different types of New Hampshire Promissory Notes in Connection with the Sale of Motor Vehicle include: 1. Installment Promissory Note: This type of note allows the buyer to make payments in installments over a specific period. The note specifies the repayment schedule, including the amount and frequency of each installment. 2. Secured Promissory Note: A secured note adds a layer of security for the seller by allowing them to place a lien on the motor vehicle. This means that if the buyer defaults on the payment, the seller has the right to repossess the vehicle to recover the amount owed. 3. Unsecured Promissory Note: An unsecured note does not involve any collateral, putting more weight on the buyer's creditworthiness. If the buyer defaults, the seller may have to pursue legal action to recover the outstanding amount. 4. Balloon Promissory Note: A balloon note defers a significant portion of the payment to the end of the loan term, usually in a lump sum. This allows the buyer to enjoy lower monthly payments during the loan term but requires a larger final payment.

New Hampshire Promissory Note in Connection with Sale of Motor Vehicle

Description

How to fill out New Hampshire Promissory Note In Connection With Sale Of Motor Vehicle?

Choosing the best lawful file web template can be quite a struggle. Needless to say, there are plenty of layouts available online, but how do you get the lawful develop you will need? Utilize the US Legal Forms web site. The assistance delivers a huge number of layouts, including the New Hampshire Promissory Note in Connection with Sale of Motor Vehicle, which can be used for company and personal requirements. Every one of the types are examined by pros and meet state and federal demands.

In case you are already authorized, log in for your bank account and click on the Down load key to obtain the New Hampshire Promissory Note in Connection with Sale of Motor Vehicle. Utilize your bank account to search throughout the lawful types you possess acquired earlier. Proceed to the My Forms tab of your respective bank account and have another backup from the file you will need.

In case you are a fresh consumer of US Legal Forms, listed below are straightforward recommendations for you to stick to:

- Initially, ensure you have chosen the correct develop for the metropolis/county. It is possible to examine the form while using Review key and look at the form information to make certain it is the right one for you.

- If the develop is not going to meet your requirements, use the Seach industry to find the appropriate develop.

- Once you are positive that the form is suitable, click on the Get now key to obtain the develop.

- Pick the prices strategy you need and enter in the essential information and facts. Make your bank account and pay for the order using your PayPal bank account or charge card.

- Select the file file format and down load the lawful file web template for your product.

- Comprehensive, revise and printing and indicator the received New Hampshire Promissory Note in Connection with Sale of Motor Vehicle.

US Legal Forms may be the most significant collection of lawful types that you can discover numerous file layouts. Utilize the service to down load appropriately-produced documents that stick to status demands.