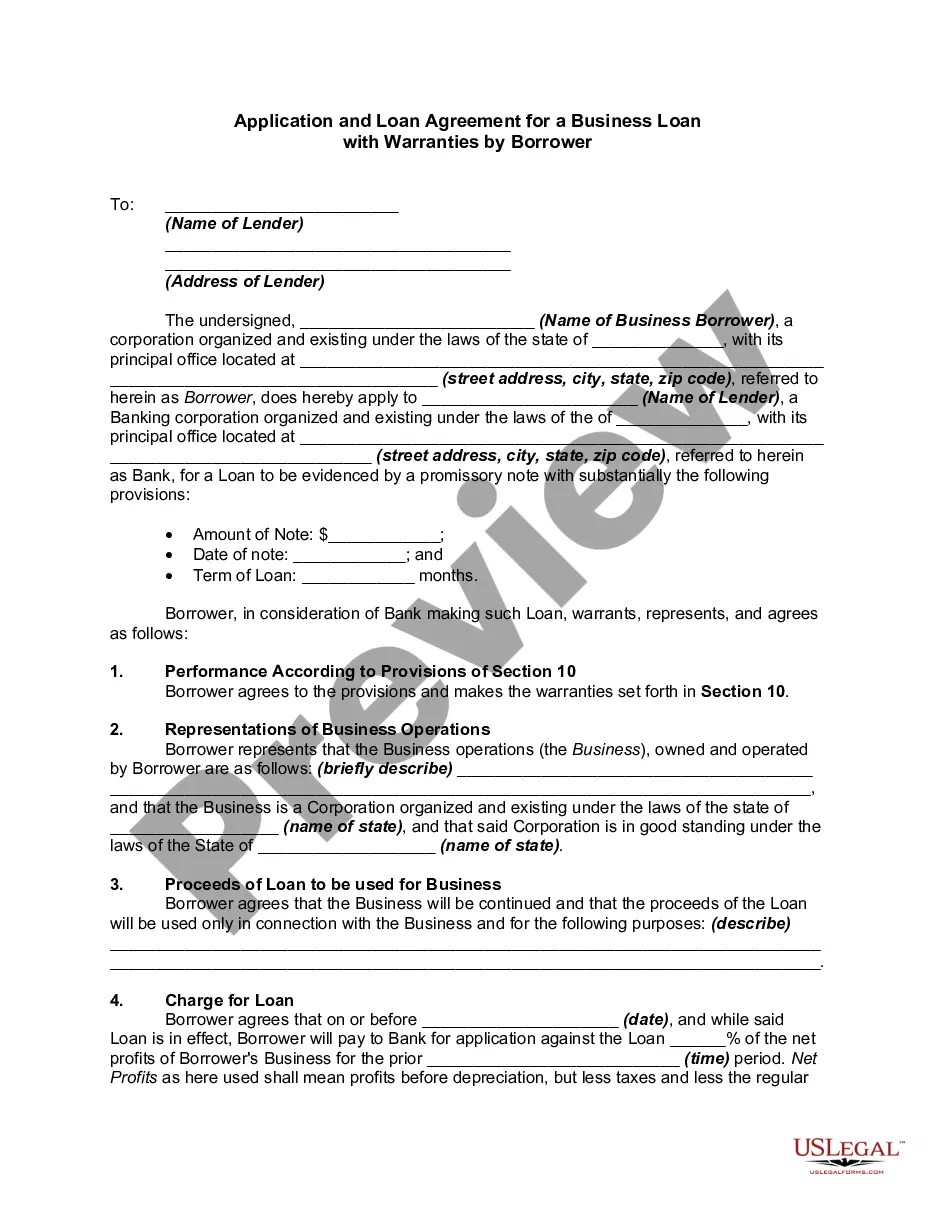

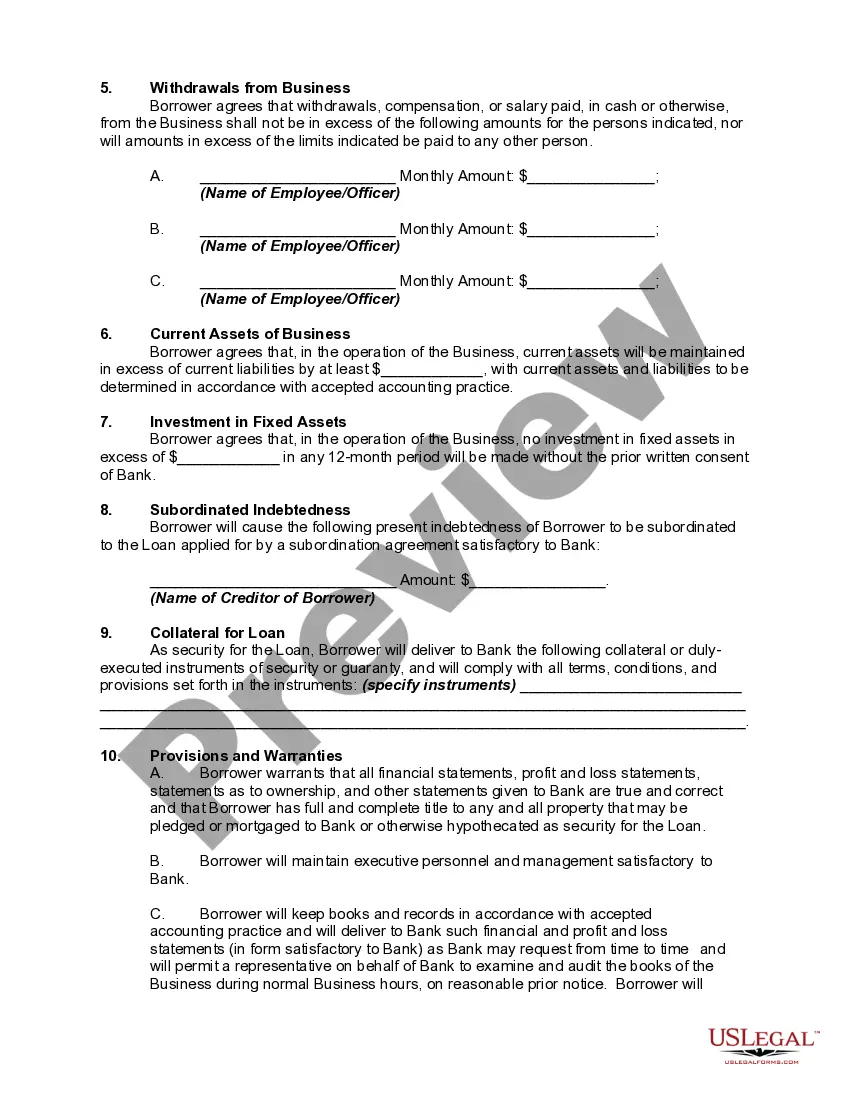

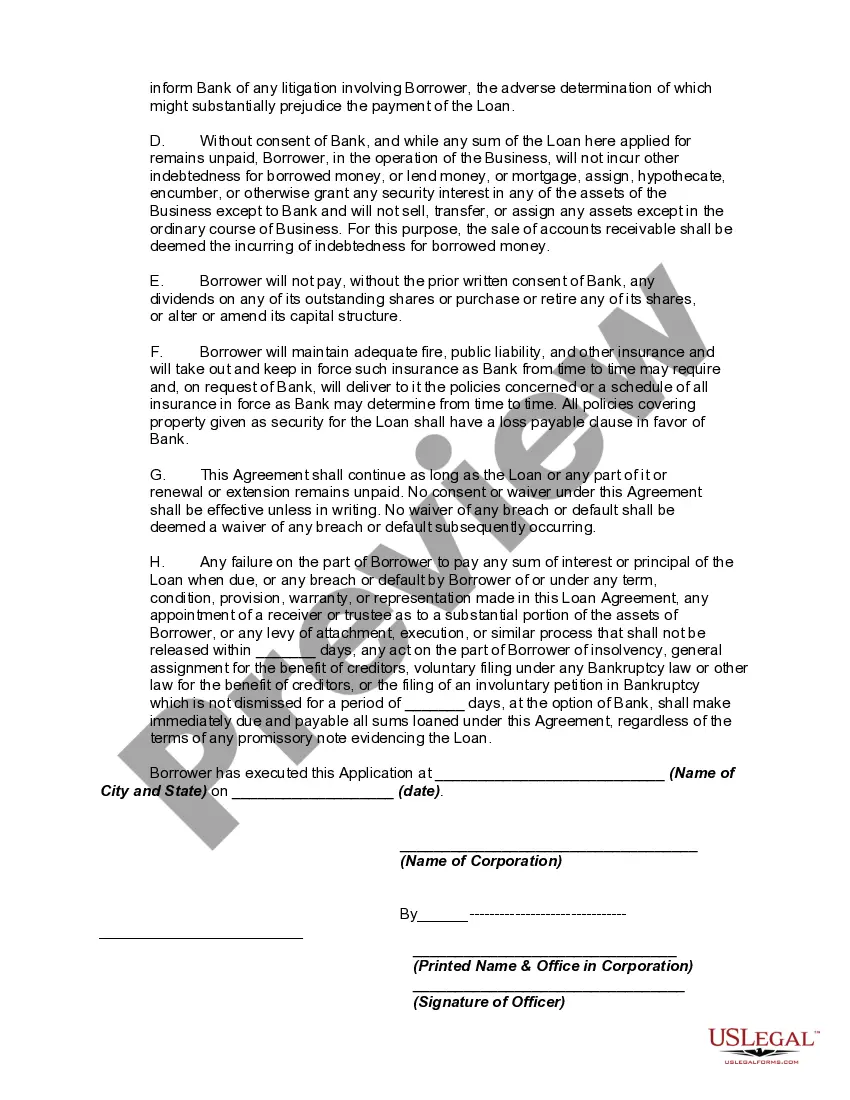

As a general matter, a loan by a bank is the borrowing of money by a person or entity who promises to return it on or before a specific date, with interest, or who pledges collateral as security for the loan and promises to redeem it at a specific later date. Loans are usually made on the basis of applications, together with financial statements submitted by the applicants.

The Federal Truth in Lending Act and the regulations promulgated under the Act apply to certain credit transactions, primarily those involving loans made to a natural person and intended for personal, family, or household purposes and for which a finance charge is made, or loans that are payable in more than four installments. However, said Act and regulations do not apply to a business loan of this type.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

New Hampshire Application and Loan Agreement for a Business Loan with Warranties by Borrower is a legal document designed for businesses seeking financial assistance in the form of a loan in the state of New Hampshire. This agreement outlines the terms and conditions under which the loan will be provided, including the borrower's warranties, which serve as assurances to the lender. Key keywords: New Hampshire, application, loan agreement, business loan, warranties, borrower. Types of New Hampshire Application and Loan Agreement for a Business Loan with Warranties by Borrower: 1. Secured Business Loan Agreement: This type of loan agreement involves the borrower offering collateral or security for the loan. The collateral may be in the form of assets, property, or inventory, which provides assurance to the lender in case of default. 2. Unsecured Business Loan Agreement: This agreement does not require the borrower to provide any collateral or security. However, it usually comes with higher interest rates and stricter terms and conditions to compensate for the increased risk faced by the lender. 3. Revolving Business Loan Agreement: A revolving loan agreement allows the borrower to access a predetermined credit limit multiple times. As long as the borrower stays within the set limit and fulfills the repayment terms, they can withdraw and repay funds as needed. 4. Term Business Loan Agreement: In this type of loan agreement, a specific amount is borrowed for a defined period, usually with fixed repayment installments over a predetermined term. Typically, term loans are used for large capital investments, such as equipment purchase or business expansion. 5. SBA (Small Business Administration) Loan Agreement: SBA loans are backed by the U.S. Small Business Administration, providing guarantees to the lending institution. This agreement follows specific guidelines and requirements set by the SBA to support small businesses in their financing needs. 6. Equipment Loan Agreement: Equipment loans are specifically designed to finance the acquisition or leasing of equipment necessary for business operations. This agreement outlines the terms for borrowing funds to purchase or lease the equipment, along with the warranties provided by the borrower. It is important for businesses in New Hampshire to carefully review and understand the chosen type of Application and Loan Agreement for a Business Loan with Warranties by Borrower before signing. Seeking legal counsel is recommended to ensure compliance with state laws and to protect the borrower's rights and obligations.New Hampshire Application and Loan Agreement for a Business Loan with Warranties by Borrower is a legal document designed for businesses seeking financial assistance in the form of a loan in the state of New Hampshire. This agreement outlines the terms and conditions under which the loan will be provided, including the borrower's warranties, which serve as assurances to the lender. Key keywords: New Hampshire, application, loan agreement, business loan, warranties, borrower. Types of New Hampshire Application and Loan Agreement for a Business Loan with Warranties by Borrower: 1. Secured Business Loan Agreement: This type of loan agreement involves the borrower offering collateral or security for the loan. The collateral may be in the form of assets, property, or inventory, which provides assurance to the lender in case of default. 2. Unsecured Business Loan Agreement: This agreement does not require the borrower to provide any collateral or security. However, it usually comes with higher interest rates and stricter terms and conditions to compensate for the increased risk faced by the lender. 3. Revolving Business Loan Agreement: A revolving loan agreement allows the borrower to access a predetermined credit limit multiple times. As long as the borrower stays within the set limit and fulfills the repayment terms, they can withdraw and repay funds as needed. 4. Term Business Loan Agreement: In this type of loan agreement, a specific amount is borrowed for a defined period, usually with fixed repayment installments over a predetermined term. Typically, term loans are used for large capital investments, such as equipment purchase or business expansion. 5. SBA (Small Business Administration) Loan Agreement: SBA loans are backed by the U.S. Small Business Administration, providing guarantees to the lending institution. This agreement follows specific guidelines and requirements set by the SBA to support small businesses in their financing needs. 6. Equipment Loan Agreement: Equipment loans are specifically designed to finance the acquisition or leasing of equipment necessary for business operations. This agreement outlines the terms for borrowing funds to purchase or lease the equipment, along with the warranties provided by the borrower. It is important for businesses in New Hampshire to carefully review and understand the chosen type of Application and Loan Agreement for a Business Loan with Warranties by Borrower before signing. Seeking legal counsel is recommended to ensure compliance with state laws and to protect the borrower's rights and obligations.