This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

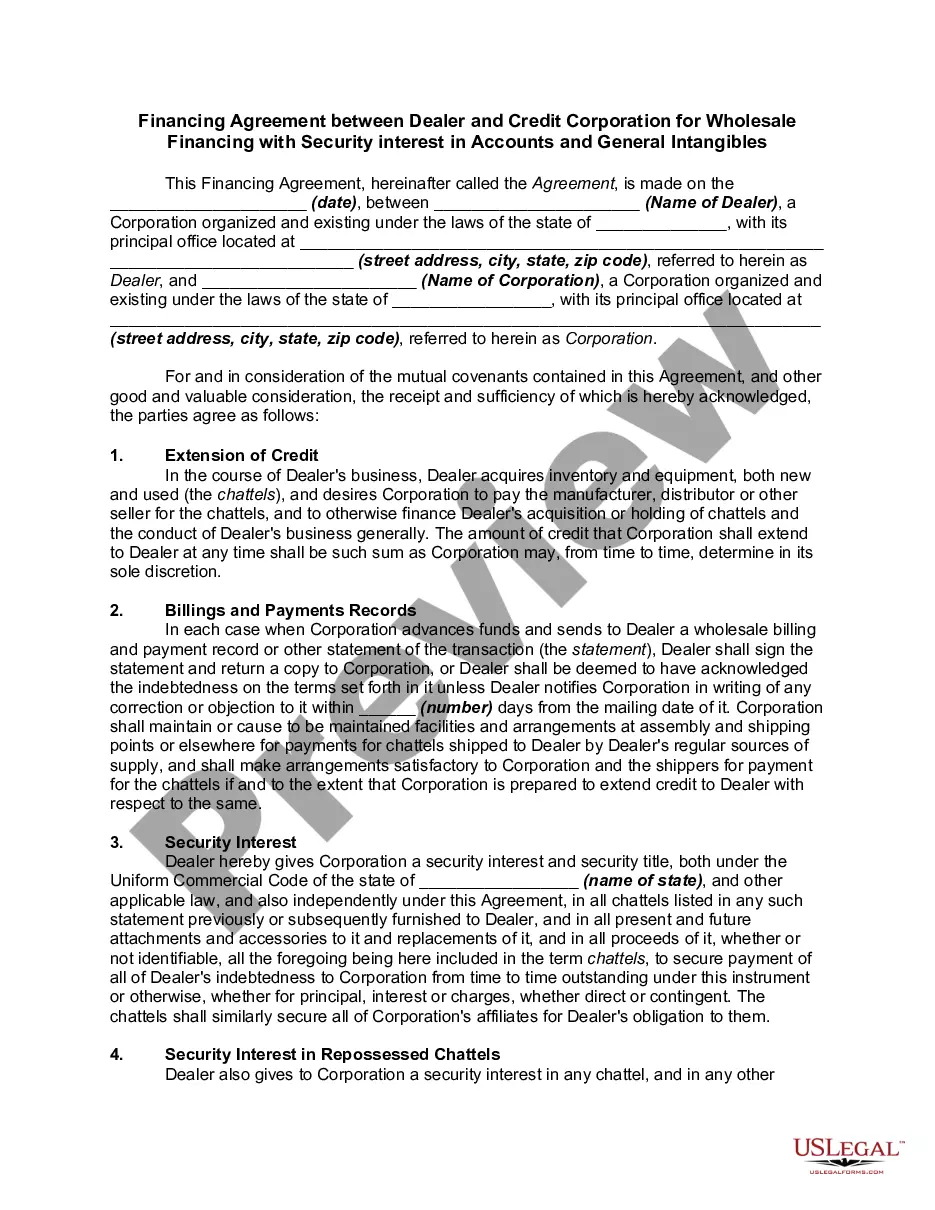

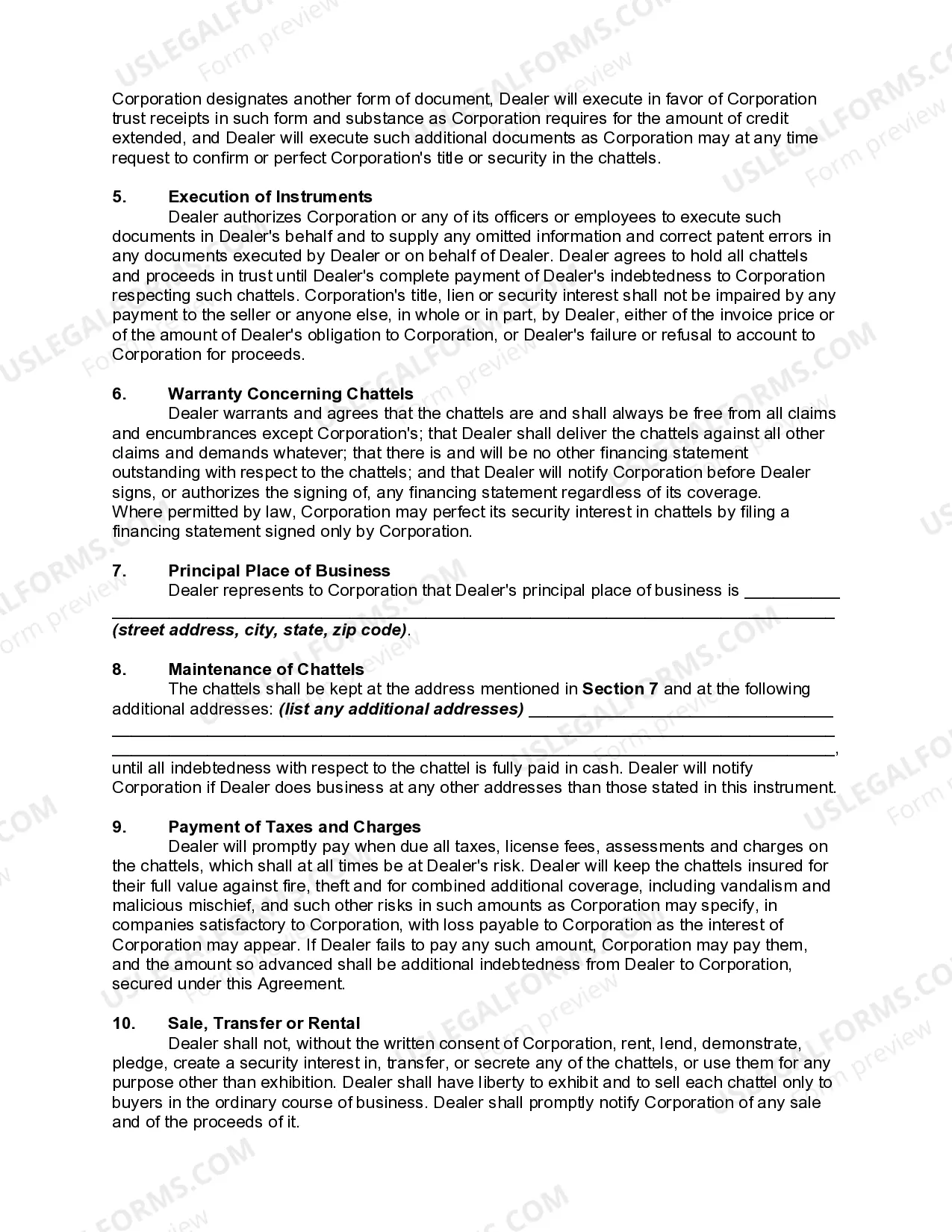

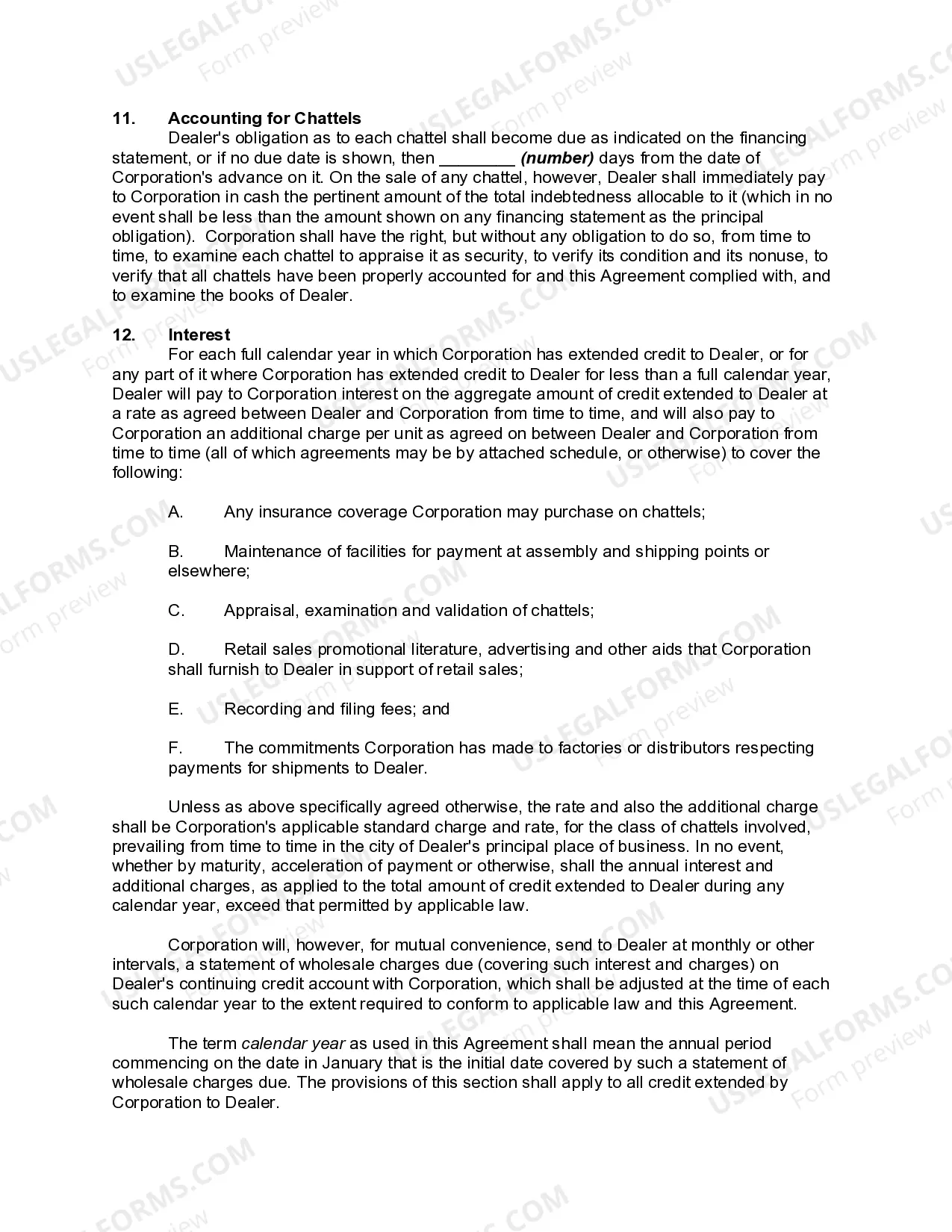

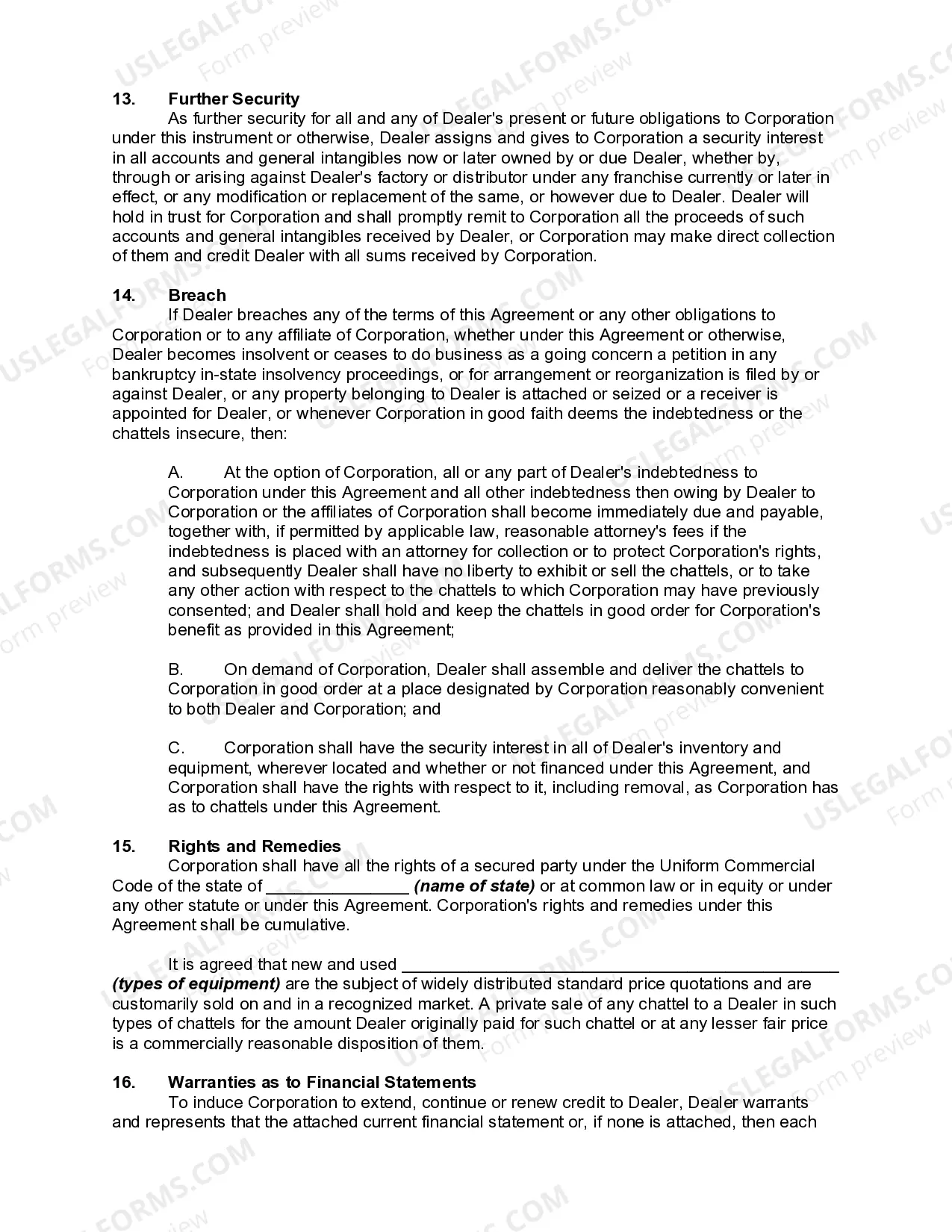

A New Hampshire Financing Agreement between a Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a legal document outlining the terms and conditions under which a credit corporation provides wholesale financing options to a dealer. This type of agreement is specifically designed to ensure the credit corporation is protected against potential defaults, especially when it comes to the dealer's accounts and general intangible assets. In New Hampshire, there might be different types of Financing Agreements between Dealers and Credit Corporations for Wholesale Financing with Security interest in Accounts and General Intangibles, categorized based on their specific terms and conditions. However, the core elements and concepts remain the same. Here are some important details typically included in such agreements: 1. Parties involved: The agreement identifies the parties entering into the transaction, namely the dealer (seller) and the credit corporation (lender). It highlights their legal names, addresses, and contact details. 2. Purpose: The agreement states that the credit corporation is providing financing to the dealer for wholesale transactions. It explains that the dealer requires funding to purchase goods and inventory for resale purposes. 3. Granting of Security Interest: This clause establishes that the dealer grants the credit corporation a security interest in their accounts and general intangibles. This ensures that the credit corporation has recourse in case of non-payment or default. 4. Collateral Description: The agreement provides a detailed description of the collateral offered by the dealer as security. It may include accounts receivable, trade names, software licenses, patents, trademarks, copyrights, and other intellectual property or intangible assets. 5. Financing Limits: The agreement specifies the maximum borrowing limit or credit line provided by the credit corporation to the dealer. This limit ensures that the dealer can access the necessary funds while still abiding by the agreed-upon terms and conditions. 6. Interest Rates and Fees: The agreement outlines the interest rates applicable to the financing provided. It also mentions any additional fees or charges associated with the agreement, such as origination fees, late payment penalties, or legal fees in case of default. 7. Default Provisions: This section of the agreement states the conditions under which the dealer would be considered in default. It highlights the consequences of default, including the credit corporation's right to take possession of the collateral or seek other legal remedies. 8. Term and Termination: The agreement specifies the duration of the financing arrangement, including any renewal options. It explains the termination provisions and conditions under which either party can terminate the agreement. 9. Governing Law and Jurisdiction: This clause identifies the applicable laws and jurisdiction in case of disputes between the parties. In the case of New Hampshire, it would typically reference New Hampshire state laws. Some variations of New Hampshire Financing Agreements between Dealers and Credit Corporations for Wholesale Financing with Security interest in Accounts and General Intangibles may include specific provisions tailored to the unique needs of the industry or parties involved. These could focus on factors such as the duration of collateral retention or additional guarantees required by the credit corporation. It is crucial for both the dealer and the credit corporation to thoroughly review the agreement and seek legal advice to ensure compliance with New Hampshire laws and to protect their respective interests within the scope of such a financing arrangement.A New Hampshire Financing Agreement between a Dealer and Credit Corporation for Wholesale Financing with Security interest in Accounts and General Intangibles is a legal document outlining the terms and conditions under which a credit corporation provides wholesale financing options to a dealer. This type of agreement is specifically designed to ensure the credit corporation is protected against potential defaults, especially when it comes to the dealer's accounts and general intangible assets. In New Hampshire, there might be different types of Financing Agreements between Dealers and Credit Corporations for Wholesale Financing with Security interest in Accounts and General Intangibles, categorized based on their specific terms and conditions. However, the core elements and concepts remain the same. Here are some important details typically included in such agreements: 1. Parties involved: The agreement identifies the parties entering into the transaction, namely the dealer (seller) and the credit corporation (lender). It highlights their legal names, addresses, and contact details. 2. Purpose: The agreement states that the credit corporation is providing financing to the dealer for wholesale transactions. It explains that the dealer requires funding to purchase goods and inventory for resale purposes. 3. Granting of Security Interest: This clause establishes that the dealer grants the credit corporation a security interest in their accounts and general intangibles. This ensures that the credit corporation has recourse in case of non-payment or default. 4. Collateral Description: The agreement provides a detailed description of the collateral offered by the dealer as security. It may include accounts receivable, trade names, software licenses, patents, trademarks, copyrights, and other intellectual property or intangible assets. 5. Financing Limits: The agreement specifies the maximum borrowing limit or credit line provided by the credit corporation to the dealer. This limit ensures that the dealer can access the necessary funds while still abiding by the agreed-upon terms and conditions. 6. Interest Rates and Fees: The agreement outlines the interest rates applicable to the financing provided. It also mentions any additional fees or charges associated with the agreement, such as origination fees, late payment penalties, or legal fees in case of default. 7. Default Provisions: This section of the agreement states the conditions under which the dealer would be considered in default. It highlights the consequences of default, including the credit corporation's right to take possession of the collateral or seek other legal remedies. 8. Term and Termination: The agreement specifies the duration of the financing arrangement, including any renewal options. It explains the termination provisions and conditions under which either party can terminate the agreement. 9. Governing Law and Jurisdiction: This clause identifies the applicable laws and jurisdiction in case of disputes between the parties. In the case of New Hampshire, it would typically reference New Hampshire state laws. Some variations of New Hampshire Financing Agreements between Dealers and Credit Corporations for Wholesale Financing with Security interest in Accounts and General Intangibles may include specific provisions tailored to the unique needs of the industry or parties involved. These could focus on factors such as the duration of collateral retention or additional guarantees required by the credit corporation. It is crucial for both the dealer and the credit corporation to thoroughly review the agreement and seek legal advice to ensure compliance with New Hampshire laws and to protect their respective interests within the scope of such a financing arrangement.