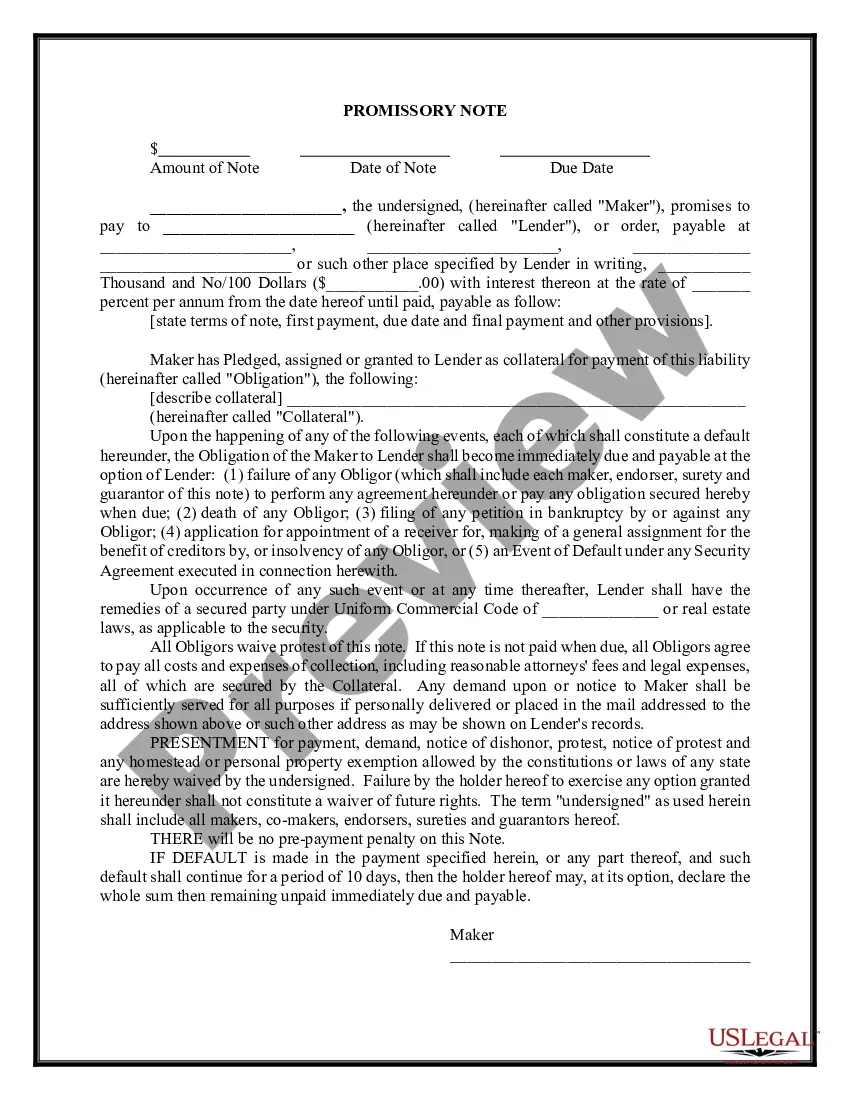

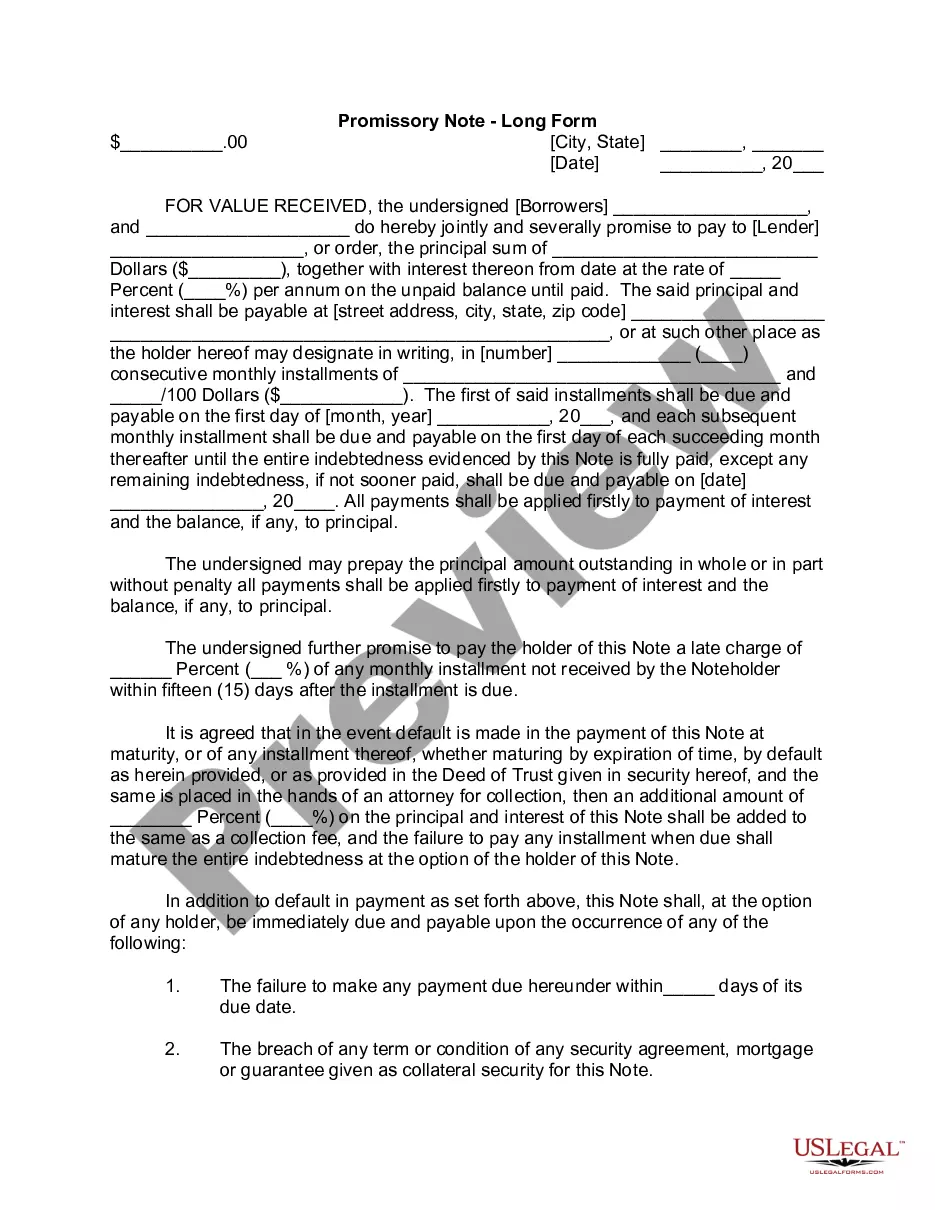

A promissory note is a written promise to pay a debt. An unconditional promise to pay on demand or at a fixed or determined future time a particular sum of money to or to the order of a specified person or to the bearer.

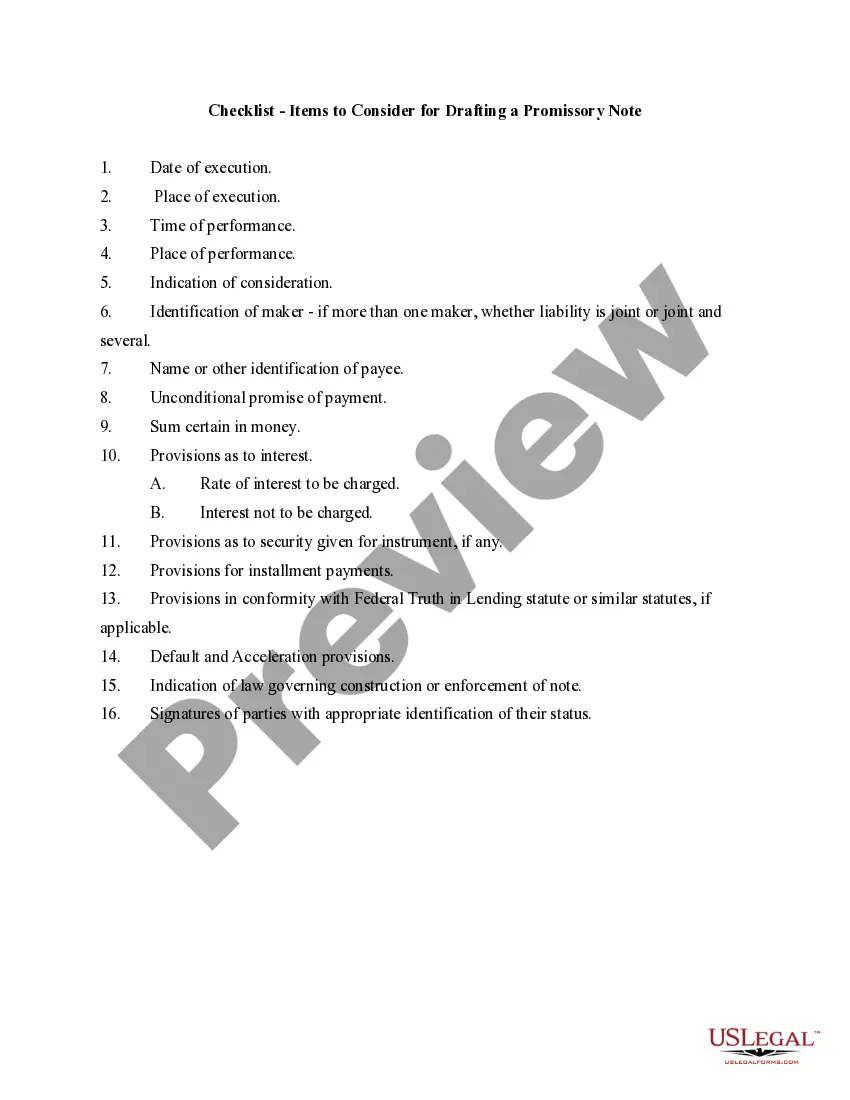

New Hampshire Checklist - Items to Consider for Drafting a Promissory Note

Category:

State:

Multi-State

Control #:

US-03060BG

Format:

Word;

Rich Text

Instant download

Description

How to fill out Checklist - Items To Consider For Drafting A Promissory Note?

If you require to sum up, obtain, or produce authentic document templates, utilize US Legal Forms, the largest assortment of authentic forms that can be accessed online.

Take advantage of the website's user-friendly and efficient search function to locate the documents you need.

A range of templates for business and personal use is organized by categories and states or keywords.

Step 4. Once you find the form you want, click the Purchase now button. Choose your preferred pricing plan and enter your details to register for an account.

Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the purchase.Step 6. Select the format of the legal form and download it to your device.Step 7. Fill out, modify, and print or sign the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note. Every legal document format you purchase is yours permanently. You have access to all forms you downloaded in your account. Click on the My documents section and select a form to print or download again.

- Utilize US Legal Forms to find the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note with just a few clicks.

- If you are already a US Legal Forms customer, Log In to your account and click the Obtain button to receive the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note.

- You can also access forms you previously downloaded in the My documents tab of your account.

- If you are utilizing US Legal Forms for the first time, follow the steps below.

- Step 1. Ensure you have chosen the form for the relevant city/state.

- Step 2. Use the Review option to examine the form's details. Don’t forget to read the description.

- Step 3. If you are not satisfied with the form, use the Lookup area at the top of the screen to search for other versions of the legal form template.

Form popularity

FAQ

The elements of a promissory note include the principal amount, the interest rate, and the maturity date. Additionally, both the borrower and the lender must sign the document to validate it. Each element plays a vital role in defining the obligations of each party. To ensure you include all necessary components, consult the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note.

A required element of a valid promissory note is the clear statement of the amount owed. This statement ensures that both parties understand the financial commitment involved. Including specific details such as the due date and interest rate is also crucial. For a complete understanding, refer to the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note.

Promissory notes follow specific rules, such as being in writing, clearly stating payment terms, and containing the correct signatures. Furthermore, the note should also address any interest rates and default conditions. Familiarizing yourself with these rules can prevent future disputes. The New Hampshire Checklist - Items to Consider for Drafting a Promissory Note can serve as a practical guide in navigating these critical aspects.

Legal requirements for a promissory note typically include a clear agreement outlining the debt, signatures from both parties, and the terms of repayment. It is also important that the note meets any specific state laws governing promissory notes. To ensure you comply with all legal stipulations, use the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note. This resource offers valuable insights into crafting a compliant document.

Promissory notes can be deemed invalid for several reasons, including lack of consideration or an unclear repayment term. Additionally, if the note does not contain the necessary signatures, it may not be enforceable. To avoid these pitfalls, consult the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note for guidance. This checklist helps ensure your note complies with legal standards.

To ensure your promissory note is valid, it should include the names of the lender and borrower, the principal amount, interest rate, and payment terms. Furthermore, the document needs to be signed by the borrower to confirm their commitment. Following the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note will guide you through these critical components.

While some features of a promissory note enhance its effectiveness, not all are essential for validity. For instance, including a payment due date is helpful but not strictly necessary. The New Hampshire Checklist - Items to Consider for Drafting a Promissory Note helps clarify what is important and what can be omitted when creating your document.

You would need to incorporate several key components in a promissory note, including the principal amount, interest rates, repayment schedule, and the parties involved. Explicitly stating these elements minimizes misunderstandings and lays a clear framework for repayment. Using the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note will facilitate a thorough preparation process.

To fill out a promissory note sample, start by entering the date, followed by the lender's and borrower's names. Specify the amount, interest rate, and payment schedule next. Lastly, remember to sign the note to validate the agreement, and ensure you stick to the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note for guidance.

For a promissory note to be valid, it must be in writing, clearly outline the amount, and be signed by the borrower. It’s crucial that both parties understand and agree on the terms; this clarity helps prevent misunderstandings. Use the New Hampshire Checklist - Items to Consider for Drafting a Promissory Note to ensure that your note meets all legal standards.