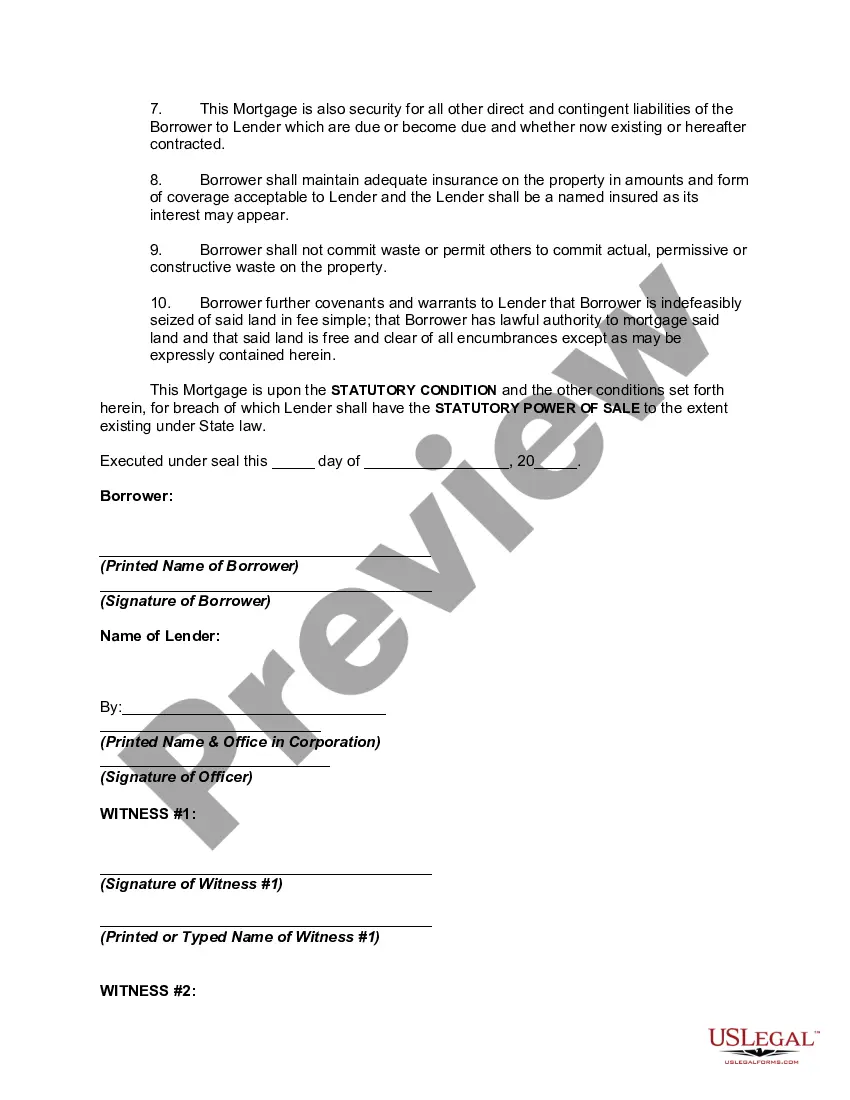

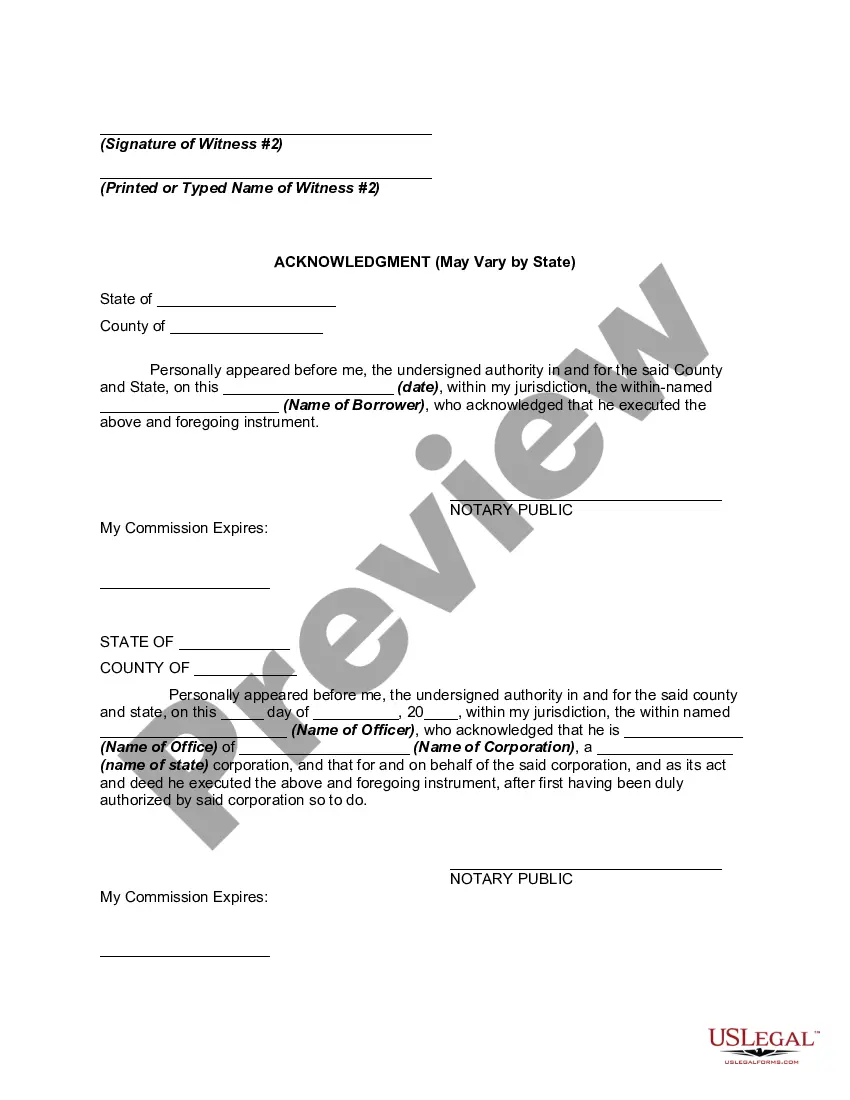

A New Hampshire Mortgage Deed is a legal document that establishes a lien on a property in New Hampshire as security for a mortgage loan. It serves as evidence of the borrower's obligation to repay the loan and provides the lender with the ability to foreclose on the property in case of default. The New Hampshire Mortgage Deed typically includes various details such as the names and addresses of the borrower (mortgagor) and the lender (mortgagee), a description of the property being mortgaged, the terms of the mortgage loan including the amount borrowed, interest rate, repayment period, and any specific provisions related to the loan. Keyword: New Hampshire Mortgage Deed There are different types of New Hampshire Mortgage Deeds that can be used: 1. Fixed-Rate Mortgage Deed: This type of mortgage deed features a fixed interest rate for the entire term of the loan. Borrowers benefit from predictable monthly payments, making budgeting easier. 2. Adjustable-Rate Mortgage Deed (ARM): With an ARM, the interest rate on the loan adjusts periodically based on market conditions. The initial interest rate is typically lower than a fixed-rate mortgage but can increase or decrease over time, potentially affecting the monthly payments. 3. Balloon Mortgage Deed: In a balloon mortgage, the borrower initially makes smaller monthly payments for a fixed period, and at the end of this period, a large "balloon" payment is due. This type of mortgage is suitable for those who plan on selling or refinancing the property before the balloon payment becomes due. 4. Interest-Only Mortgage Deed: With this type of mortgage deed, the borrower only pays the interest on the loan for a specific period, typically between 5 and 10 years. After that period, the borrower starts making payments towards both the principal and interest amounts. 5. Reverse Mortgage Deed: Reserved for homeowners who are at least 62 years old, a reverse mortgage allows eligible borrowers to convert a portion of their home equity into loan proceeds. Repayment is typically deferred until the borrower moves out of the property or passes away. It is important to note that specific legal requirements and regulations may apply to each type of New Hampshire Mortgage Deed. It is recommended to consult with a qualified attorney or mortgage professional to ensure compliance and to make informed decisions based on individual circumstances.

New Hampshire Mortgage Deed

Description

How to fill out New Hampshire Mortgage Deed?

Choosing the right authorized papers format could be a struggle. Needless to say, there are tons of templates available on the Internet, but how do you discover the authorized kind you will need? Take advantage of the US Legal Forms web site. The assistance offers thousands of templates, for example the New Hampshire Mortgage Deed, which can be used for enterprise and private needs. Each of the kinds are examined by specialists and meet up with federal and state specifications.

In case you are currently registered, log in to your profile and click the Acquire button to have the New Hampshire Mortgage Deed. Utilize your profile to appear from the authorized kinds you might have acquired earlier. Go to the My Forms tab of your profile and have yet another backup of your papers you will need.

In case you are a brand new end user of US Legal Forms, here are basic instructions that you can comply with:

- Initially, make sure you have selected the right kind for your personal area/county. You can examine the shape while using Review button and browse the shape information to guarantee this is basically the right one for you.

- When the kind does not meet up with your requirements, utilize the Seach discipline to find the appropriate kind.

- Once you are certain that the shape is acceptable, click the Get now button to have the kind.

- Opt for the pricing strategy you want and enter the necessary details. Make your profile and purchase the transaction utilizing your PayPal profile or Visa or Mastercard.

- Opt for the document structure and obtain the authorized papers format to your gadget.

- Comprehensive, edit and print out and indication the attained New Hampshire Mortgage Deed.

US Legal Forms is the greatest library of authorized kinds where you can see a variety of papers templates. Take advantage of the company to obtain professionally-created papers that comply with express specifications.