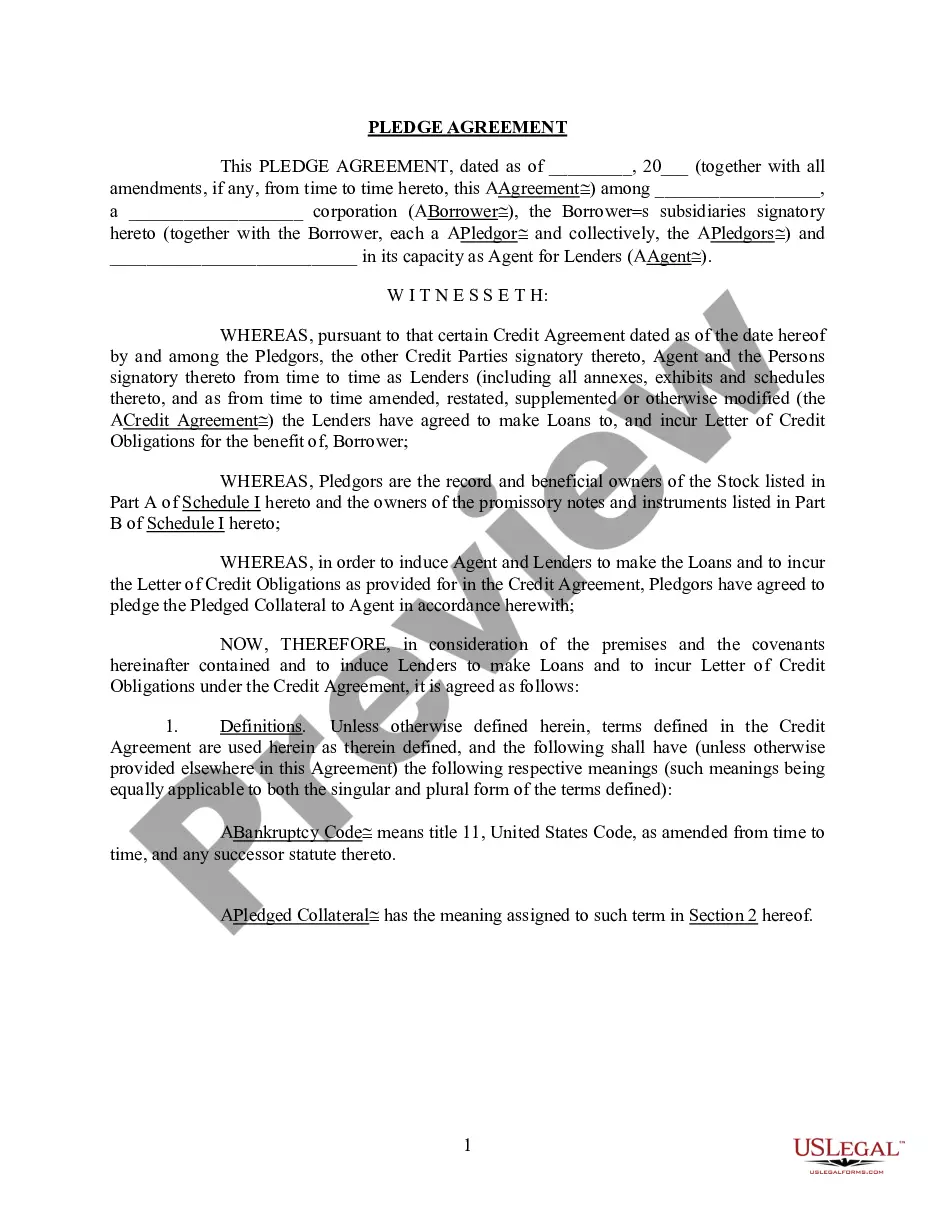

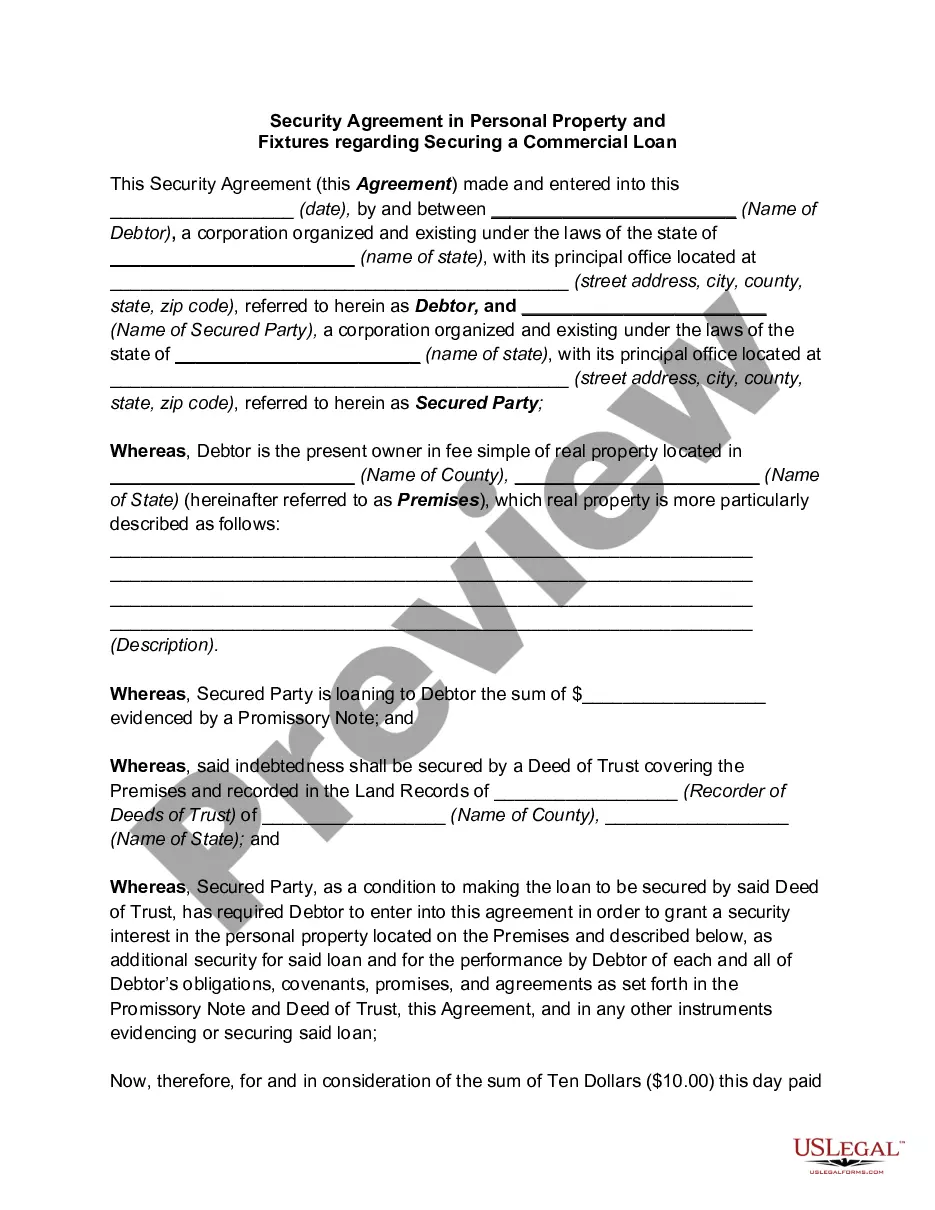

A pledge is a deposit of personal property as security for a personal loan of money. If the loan is not repaid when due, the personal property pledged is forfeited to the lender. The property is known as collateral. A pledge occurs when someone gives property to a pawnbroker in exchange for money.

As the pledge is for the benefit of both parties, the pledgee is bound to exercise only ordinary care over the pledge. The pledgee has the right of selling the pledge if the pledgor make default in payment at the stipulated time. In the case of a wrongful sale by a pledgee, the pledgor cannot recover the value of the pledge without a tender of the amount due.

New Hampshire Pledge of Personal Property as Collateral Security

Category:

State:

Multi-State

Control #:

US-03128BG

Format:

Word;

Rich Text

Instant download

Description

How to fill out Pledge Of Personal Property As Collateral Security?

Have you ever found yourself in a situation where you require documents for either professional or personal purposes on a daily basis? There is an abundance of legal document templates available online, but locating reliable ones can be challenging.

US Legal Forms provides a vast array of form templates, including the New Hampshire Pledge of Personal Property as Collateral Security, designed to comply with both state and federal requirements.

If you are already acquainted with the US Legal Forms website and possess an account, simply Log In. After that, you can download the New Hampshire Pledge of Personal Property as Collateral Security template.

Choose a convenient file format and download your copy.

Access all the document templates you have purchased in the My documents section. You can obtain another copy of the New Hampshire Pledge of Personal Property as Collateral Security at any time if needed. Just click the required form to download or print the document template.

- If you do not have an account and wish to use US Legal Forms, follow these steps.

- Find the form you need and confirm it is for the right city/state.

- Click the Review button to evaluate the form.

- Read the description to ensure that you have selected the correct form.

- If the form does not meet your requirements, utilize the Search field to discover the form that aligns with your needs.

- Once you find the right form, hit Buy now.

- Select the pricing plan you prefer, provide the necessary information to create your account, and process the payment using your PayPal or Visa or Mastercard.

Form popularity

FAQ

Any individual or business that possesses personal property can grant a security interest, provided they have the authority to do so. This includes owners of personal assets such as machinery, vehicles, or inventory. When it comes to the New Hampshire Pledge of Personal Property as Collateral Security, it ensures that the process is straightforward for property owners looking to secure financing.

To obtain a security interest, a lender must first assess the borrower's assets and the risk involved. Then, they draft a security agreement that complies with state laws, including the New Hampshire Pledge of Personal Property as Collateral Security. This agreement will dictate how the collateral is managed and what happens in case of default, creating a safeguard for the lender.

To establish an enforceable security interest, there are three essential requirements: attachment, which involves the borrower granting the interest; the secured creditor must have the rights to the collateral; and the debtor must have clear possession or control of the collateral. Understanding these requirements is crucial when considering the New Hampshire Pledge of Personal Property as Collateral Security. This pledge can simplify the enforcement process by providing clear terms.

Yes, personal property can indeed be used as collateral. Under the New Hampshire Pledge of Personal Property as Collateral Security, borrowers can pledge items like electronics or collectibles to secure loans. This provides a flexible financing option, allowing individuals to retain control over their valuable assets. Ensure that the lender understands the value and condition of your pledged items.

To use your property as collateral, you first need to assess the market value of your asset. Next, you can approach a lender and present your property for the New Hampshire Pledge of Personal Property as Collateral Security. The lender will evaluate the asset and typically require documentation to finalize the terms. This can be an effective way to obtain financing while keeping your property.

An example of pledge collateral includes personal property such as a vehicle, jewelry, or art. When using the New Hampshire Pledge of Personal Property as Collateral Security, you can leverage these items to secure loans. This process allows you to obtain necessary funds while retaining ownership of your property. Be sure to understand the terms before committing your assets as collateral.

To pledge assets as collateral (or Pledging) is the act of offering assets as collateral to secure loans. Assets pledged can be in the form of security holdings and act as assurance for recovering the borrowed amount should a borrower fail to pay up.

Collateral, a borrower's pledge to a lender of something specific that is used to secure the repayment of a loan (see credit). The collateral is pledged when the loan contract is signed and serves as protection for the lender.

Under the UCC, a pledge agreement is a security agreement. The nature of the pledged assets means that a pledge agreement may contain different representations and warranties and covenants than a security agreement over business assets (for example, voting rights).

To pledge assets as collateral (or Pledging) is the act of offering assets as collateral to secure loans. Assets pledged can be in the form of security holdings and act as assurance for recovering the borrowed amount should a borrower fail to pay up.