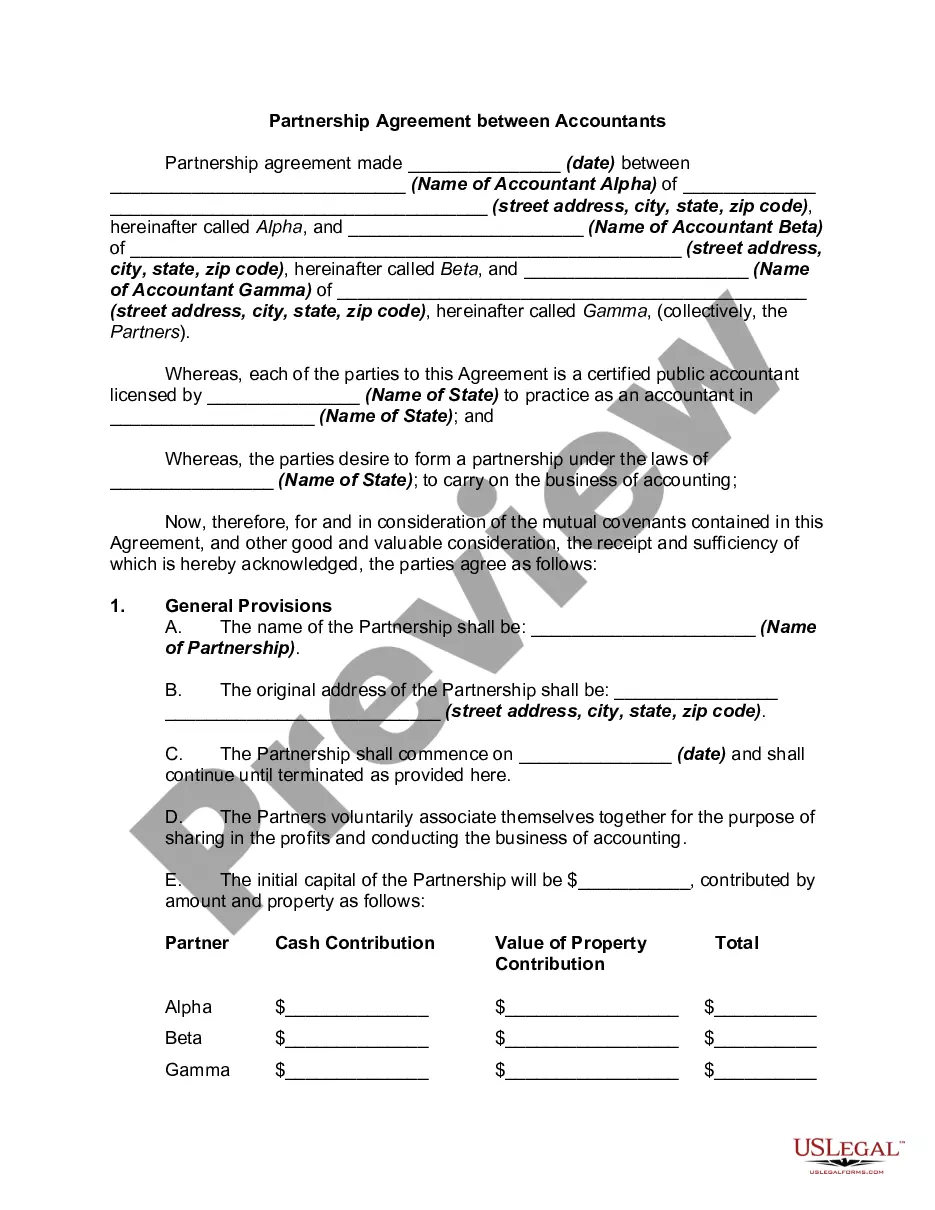

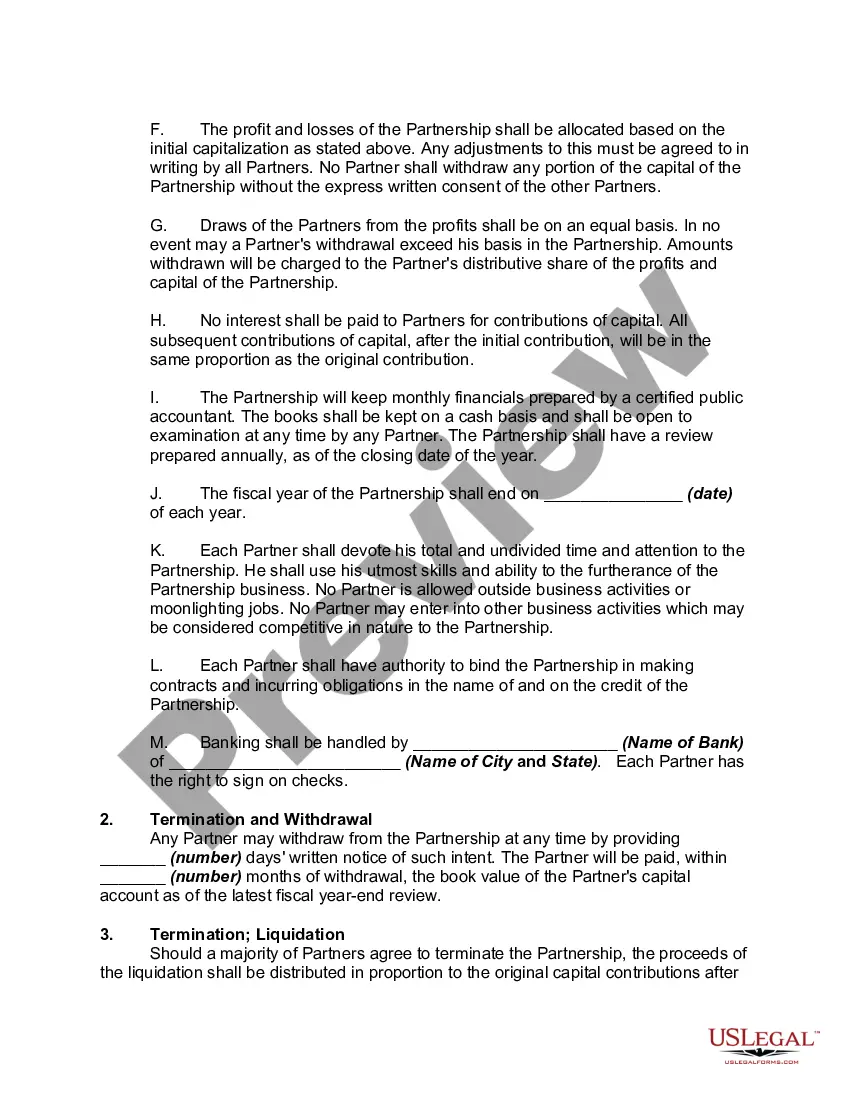

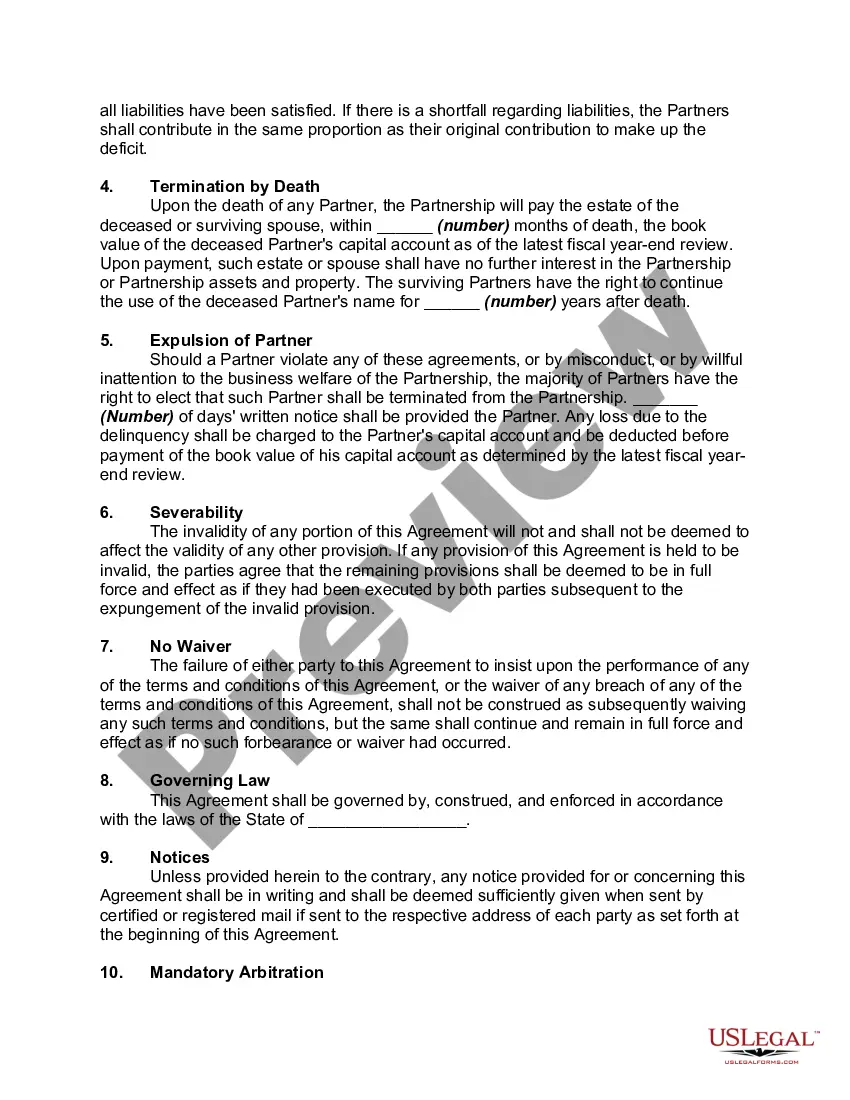

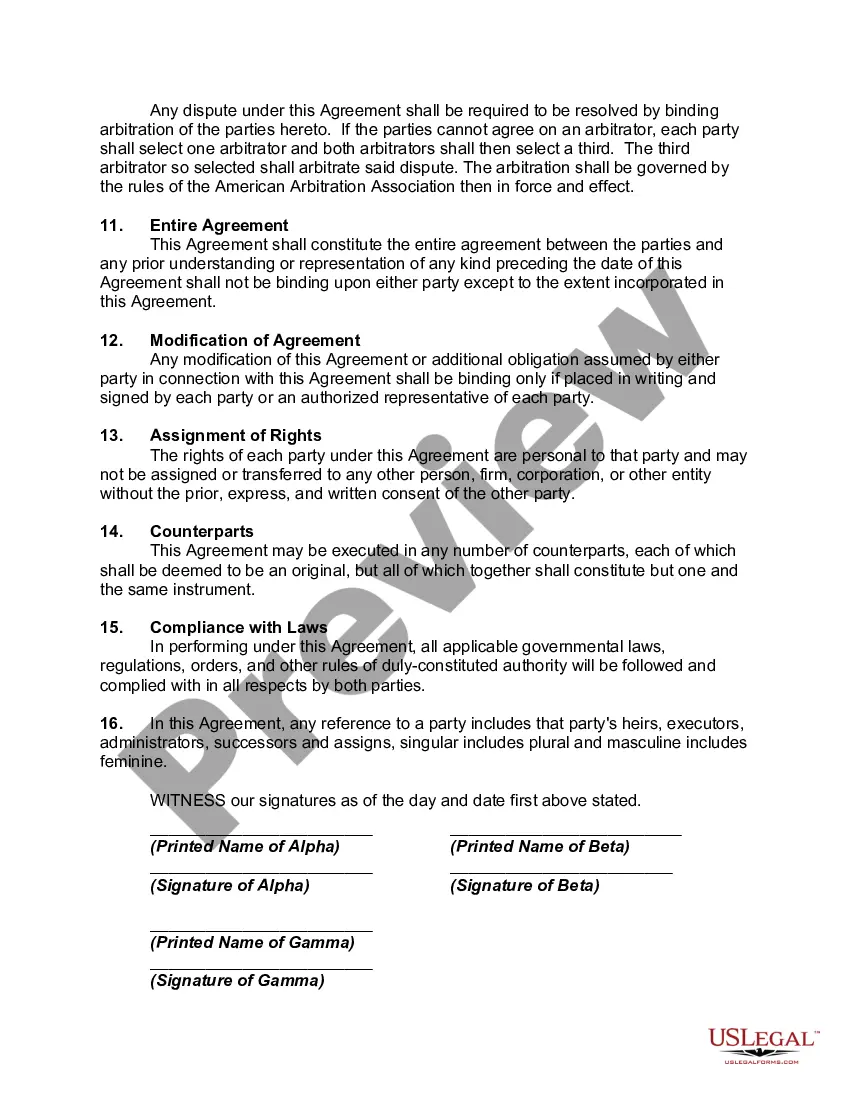

Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

A New Hampshire Partnership Agreement Between Accountants is a legally binding document that outlines the terms and conditions of a partnership formed between two or more accounting professionals or firms in the state of New Hampshire. This agreement serves as a blueprint for the partnership's operations, goals, responsibilities, and financial arrangements. Keywords: New Hampshire, Partnership Agreement, Accountants Types of New Hampshire Partnership Agreement Between Accountants: 1. General Partnership Agreement: A general partnership agreement is the most common type of partnership agreement. It establishes a partnership in which each partner has equal rights and responsibilities in managing the business. Profits, losses, and liabilities are shared equally among the partners unless otherwise stated in the agreement. 2. Limited Partnership Agreement: A limited partnership agreement is formed when one or more partners contribute capital to the partnership and have limited liability. These partners, known as "limited partners," do not participate in the day-to-day management of the business but rather act as investors. The general partner(s) assume full management responsibility and unlimited liability. 3. Limited Liability Partnership Agreement: A limited liability partnership (LLP) agreement offers a unique structure that protects individual partners from personal liability for the actions, debts, and obligations of the partnership and other partners. This agreement allows each partner to be shielded from the negligence or misconduct of other partners. 4. Professional Corporation Partnership Agreement: Professional accounting firms may choose to form a partnership as a professional corporation (PC). A professional corporation partnership agreement combines features of a traditional partnership and a corporation. This agreement outlines the professional standards, licensing requirements, and governance of the partnership. 5. Joint Venture Partnership Agreement: A joint venture partnership agreement is established when two or more accounting firms collaborate on a specific project or business endeavor. It outlines the purpose of the joint venture, the responsibilities of each partner, profit-sharing arrangements, and the duration of the partnership. The New Hampshire Partnership Agreement Between Accountants serves as a crucial document for accounting professionals seeking to establish a partnership within the state. It provides a legal framework delineating the roles and responsibilities of each partner, distribution of profits and losses, decision-making processes, admission and withdrawal of partners, dispute resolution mechanisms, and dissolution procedures. By adhering to a well-drafted partnership agreement, accountants in New Hampshire can ensure clarity, protection, and alignment of interests, enabling them to build a successful and mutually beneficial partnership in the competitive accounting industry.