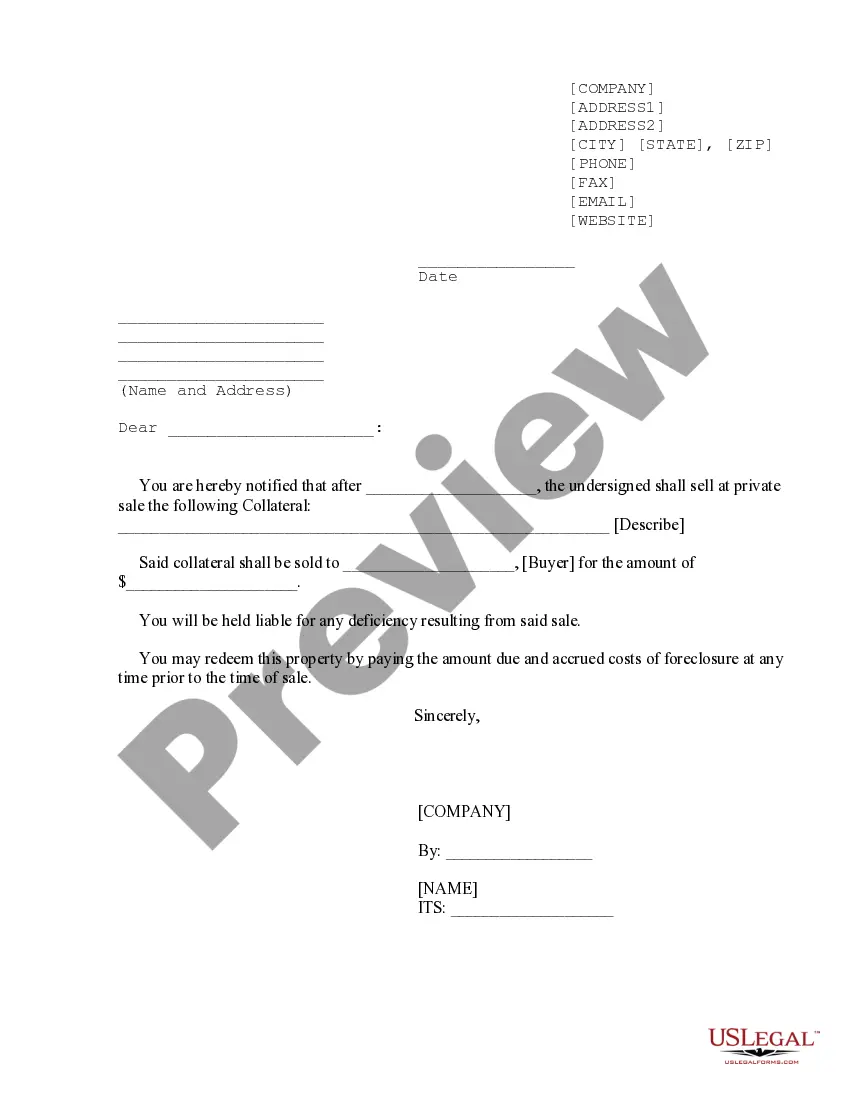

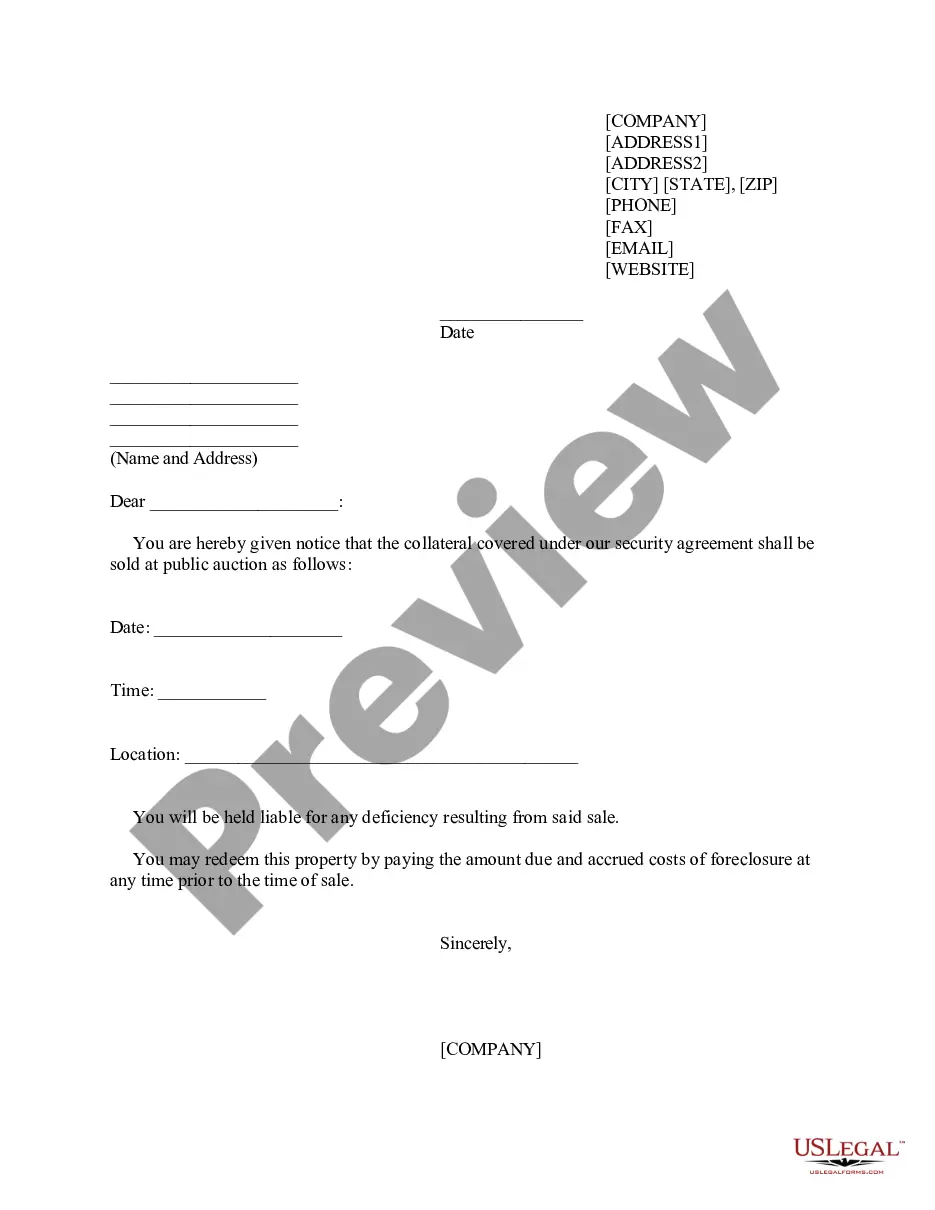

New Hampshire Notice of Private Sale of Collateral (Non-consumer Goods) on Default

Description

How to fill out Notice Of Private Sale Of Collateral (Non-consumer Goods) On Default?

Selecting the appropriate legal document template can be a challenge.

Of course, there are numerous templates available online, but how can you find the legal form you require? Utilize the US Legal Forms website.

The service offers a vast array of templates, including the New Hampshire Notice of Private Sale of Collateral (Non-consumer Goods) on Default, which you can use for both business and personal purposes. All forms are reviewed by specialists and comply with federal and state regulations.

Once you are confident that the form is suitable, click the Get now button to obtain the document. Select the pricing plan you want and enter the required details. Create your account and pay for the order using your PayPal account or credit card. Choose the file format and download the legal document template to your device. Complete, modify, and print and sign the acquired New Hampshire Notice of Private Sale of Collateral (Non-consumer Goods) on Default. US Legal Forms is the largest collection of legal templates where you can find various document templates. Use the service to obtain properly crafted paperwork that adheres to state requirements.

- If you are already registered, Log In to your account and click the Download button to access the New Hampshire Notice of Private Sale of Collateral (Non-consumer Goods) on Default.

- Use your account to browse the legal forms you may have purchased previously.

- Visit the My documents section of your account to obtain another copy of the document you need.

- If you are a new user of US Legal Forms, here are straightforward steps to follow.

- First, ensure you have chosen the correct form for your city/county. You can preview the form using the Preview button and review the form details to confirm it's suitable for you.

- If the form does not meet your criteria, use the Search function to find the appropriate form.

Form popularity

FAQ

Article 9 of the Uniform Commercial Code (UCC) governs secured transactions involving personal property. It lays the framework for creating, enforcing, and perfecting security interests, including those related to the New Hampshire Notice of Private Sale of Collateral (Non-consumer Goods) on Default. Understanding Article 9 is essential for anyone involved in secured lending or borrowing, as it outlines key provisions for protecting both the debtor and the secured party. If you need help navigating these regulations, uslegalforms provides valuable resources and templates.

The debtor's rights to redeem collateral after repossession are detailed in UCC Section 9-623. This section allows the debtor to reclaim their collateral by paying off the outstanding obligation. Recognizing these rights is vital, especially before a New Hampshire Notice of Private Sale of Collateral (Non-consumer Goods) on Default is issued.

Article 9 is an article under the Uniform Commercial Code (UCC) that governs secured transactions, or those transactions that pair a debt with the creditor's interest in the secured property.

Collateral Disposition means any sale, transfer or other disposition (whether voluntary or involuntary) to the extent involving assets or other rights or property that constitute Collateral.

On the debtor's default, a secured party can take possession (peacefully or by the court order) of the collateral covered by the security agreement. This provision, because it occurs without the use of the judicial process, is often referred to as the "self-help" provision of article 9.

When a borrower applies for a loan, most lenders require the borrower to pledge an asset as security for the repayment of the loan, i.e. collateral. In the event the borrower defaults, usually by failing to make loan payments, a secured creditor has a right to take possession of the collateral. § 679.609, Fla.

A PMSI is created in goods when a seller retains a security interest in the goods sold on credit by a security agreement. A debtor need not sign the financing statement. Attachment must occur in order to make a security interest enforceable against the debtor and against third parties.

Article 9 is a section under the UCC governing secured transactions including the creation and enforcement of debts. Article 9 spells out the procedure for settling debts, including various types of collateralized loans and bonds.

If a borrower defaults on a secured credit product, the secured creditor has a legal right to the secured asset used as collateral. The secured asset may be seized by the secured creditor and sold to pay off any remaining obligations.

on Default")