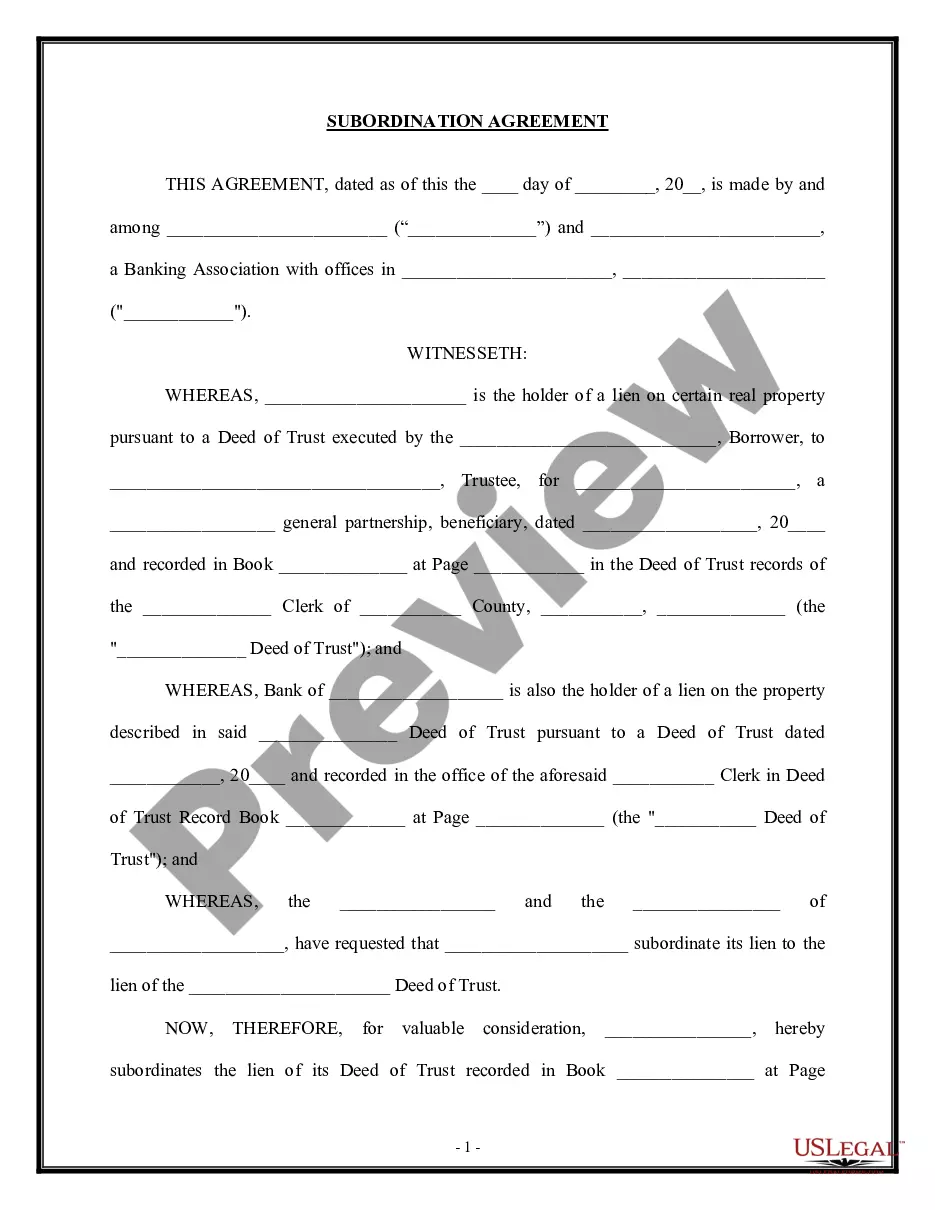

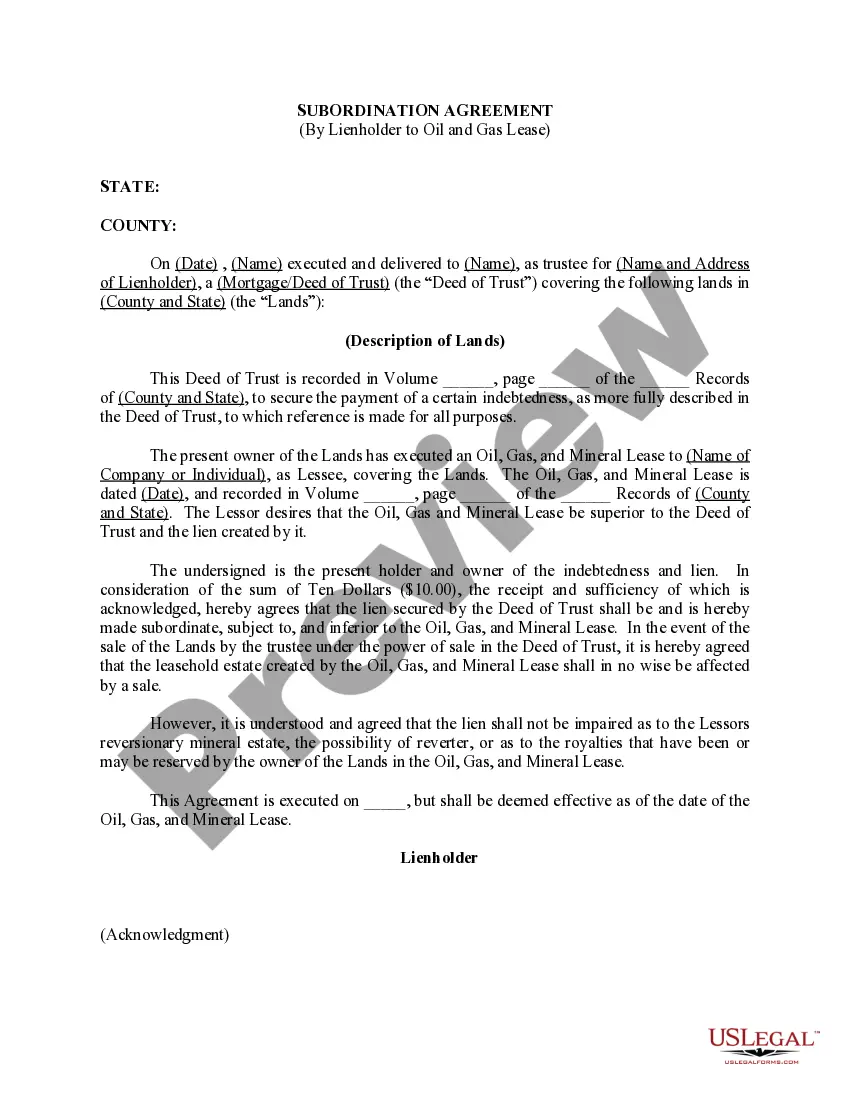

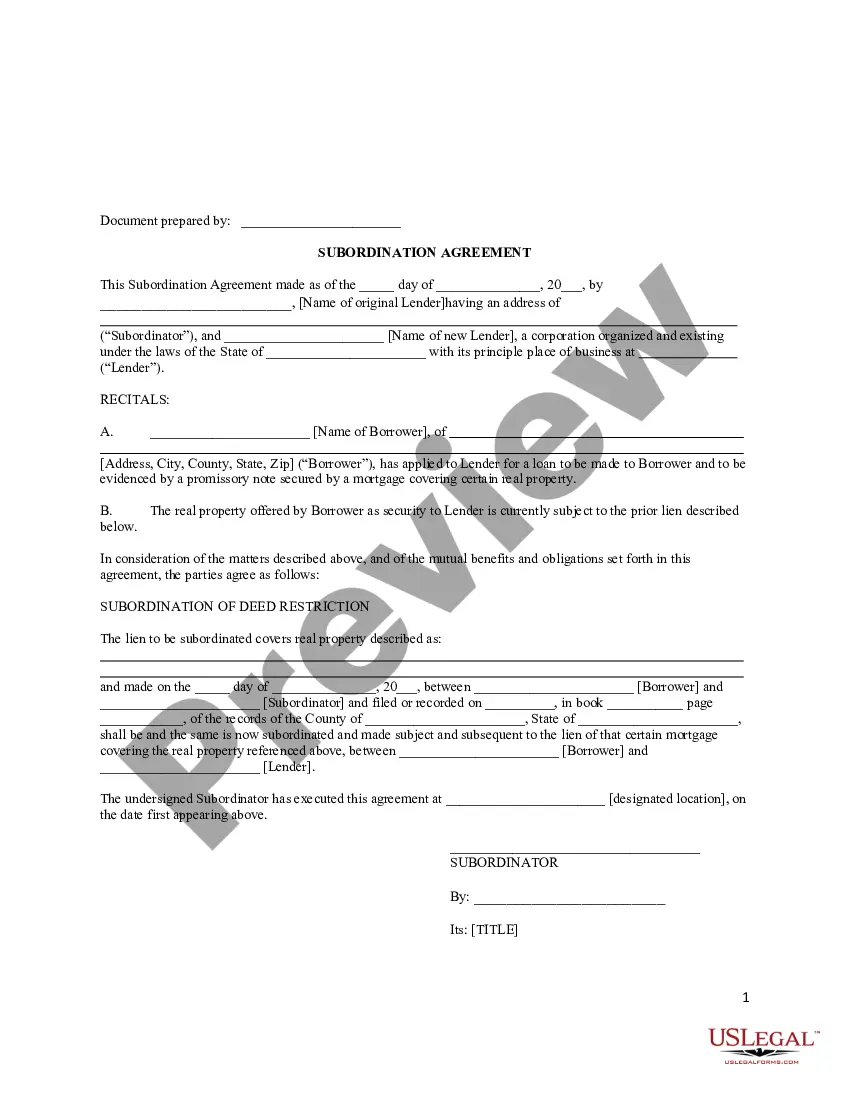

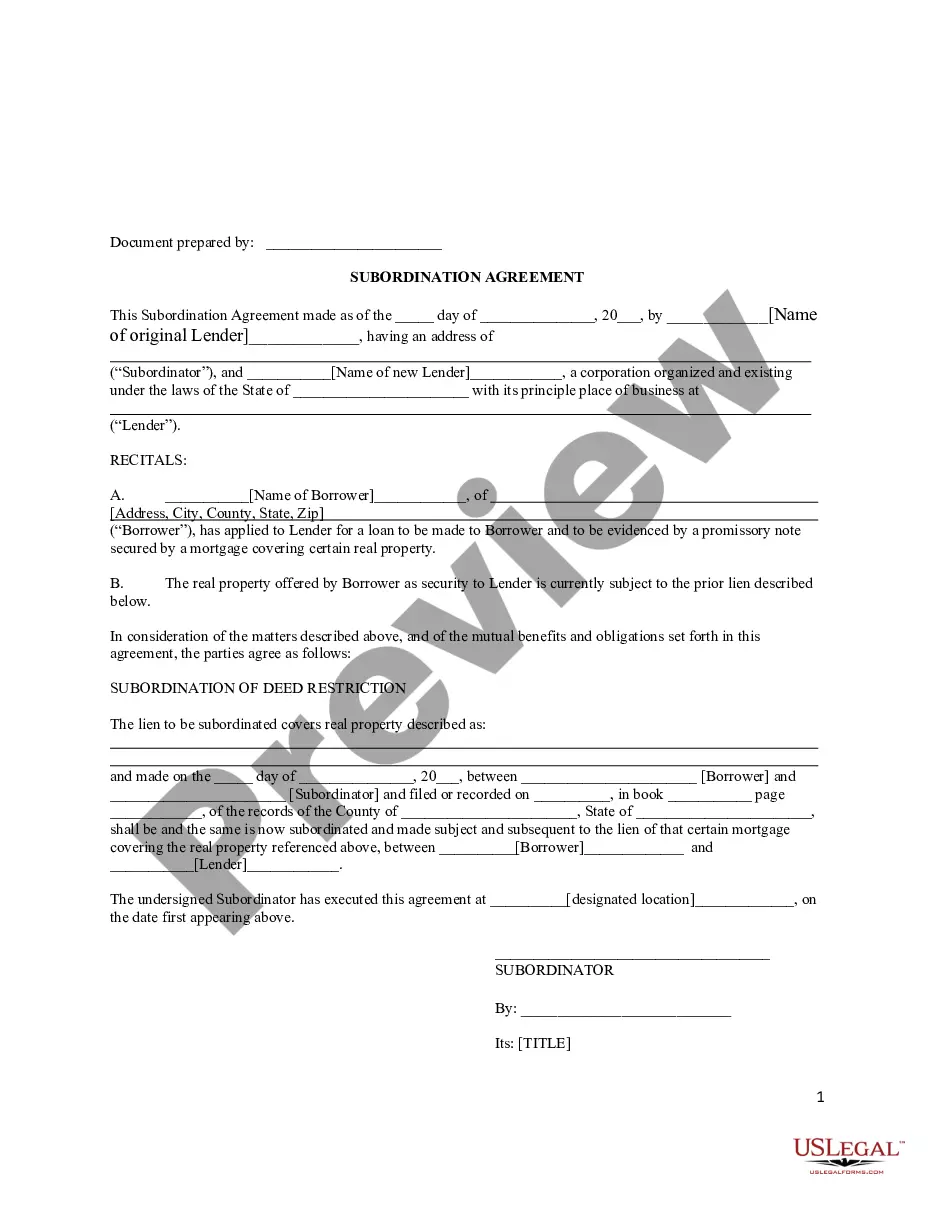

New Hampshire Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Choosing the right lawful papers template can be quite a have difficulties. Obviously, there are plenty of web templates available online, but how can you discover the lawful develop you require? Utilize the US Legal Forms internet site. The assistance provides a huge number of web templates, for example the New Hampshire Subordination Agreement Subordinating Existing Mortgage to New Mortgage, which can be used for company and private demands. Every one of the types are examined by professionals and meet up with federal and state demands.

If you are currently signed up, log in for your bank account and then click the Download key to have the New Hampshire Subordination Agreement Subordinating Existing Mortgage to New Mortgage. Utilize your bank account to check with the lawful types you have ordered formerly. Visit the My Forms tab of your own bank account and acquire yet another version of the papers you require.

If you are a brand new end user of US Legal Forms, allow me to share straightforward recommendations that you should stick to:

- Initial, make certain you have selected the correct develop for the metropolis/region. You are able to check out the form making use of the Preview key and study the form information to guarantee this is the best for you.

- In the event the develop does not meet up with your needs, take advantage of the Seach industry to find the right develop.

- Once you are certain that the form is proper, select the Acquire now key to have the develop.

- Opt for the prices program you need and enter in the essential details. Build your bank account and pay money for the order with your PayPal bank account or bank card.

- Opt for the file file format and acquire the lawful papers template for your product.

- Full, edit and print and sign the attained New Hampshire Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

US Legal Forms may be the greatest library of lawful types in which you can see different papers web templates. Utilize the company to acquire professionally-manufactured papers that stick to express demands.

Form popularity

FAQ

Again, if you're refinancing your first mortgage and the property also has a subordinate mortgage, the refinancing lender will usually handle the process of getting the necessary subordination agreement. But you need to ensure that the required subordination agreement is completed before the new loan's closing date.

A subordination clause is a clause in an agreement that states that the current claim on any debts will take priority over any other claims formed in other agreements made in the future. Subordination is the act of yielding priority.

Many people have a subordinate mortgage in the form of a home equity line of credit or home equity loan. A subordinate mortgage is secured by your property but sits in second position, if you have a primary mortgage, for getting paid in the event you default.

Many people have a subordinate mortgage in the form of a home equity line of credit or home equity loan. A subordinate mortgage is secured by your property but sits in second position, if you have a primary mortgage, for getting paid in the event you default.

A mortgage subordination refers to the order the outstanding liens on your property get repaid if you stop making your mortgage payments. For example, your first home loan (primary mortgage) is repaid first, with any remaining funds paying off additional liens, including second mortgages, HELOCs and home equity loans.

A subordination real estate mortgage clause gives the loan it's in reference to first lien position. It states that any other loans or liens on the property take a second lien position. Most first mortgage lenders won't fund a loan unless there is a subordination clause giving them first lien position.

Who Benefits from a Subordination Clause? A subordination clause is meant to protect the interests of the primary lender. A primary mortgage usually covers the cost of purchasing the home; however, if there is a secondary mortgage, the clause ensures that the primary lender retains the number one priority.

Getting A Second Mortgage A second mortgage will become a subordinate loan. If you repay the primary loan within the term of the second mortgage, the second mortgage can take its place as the primary loan.