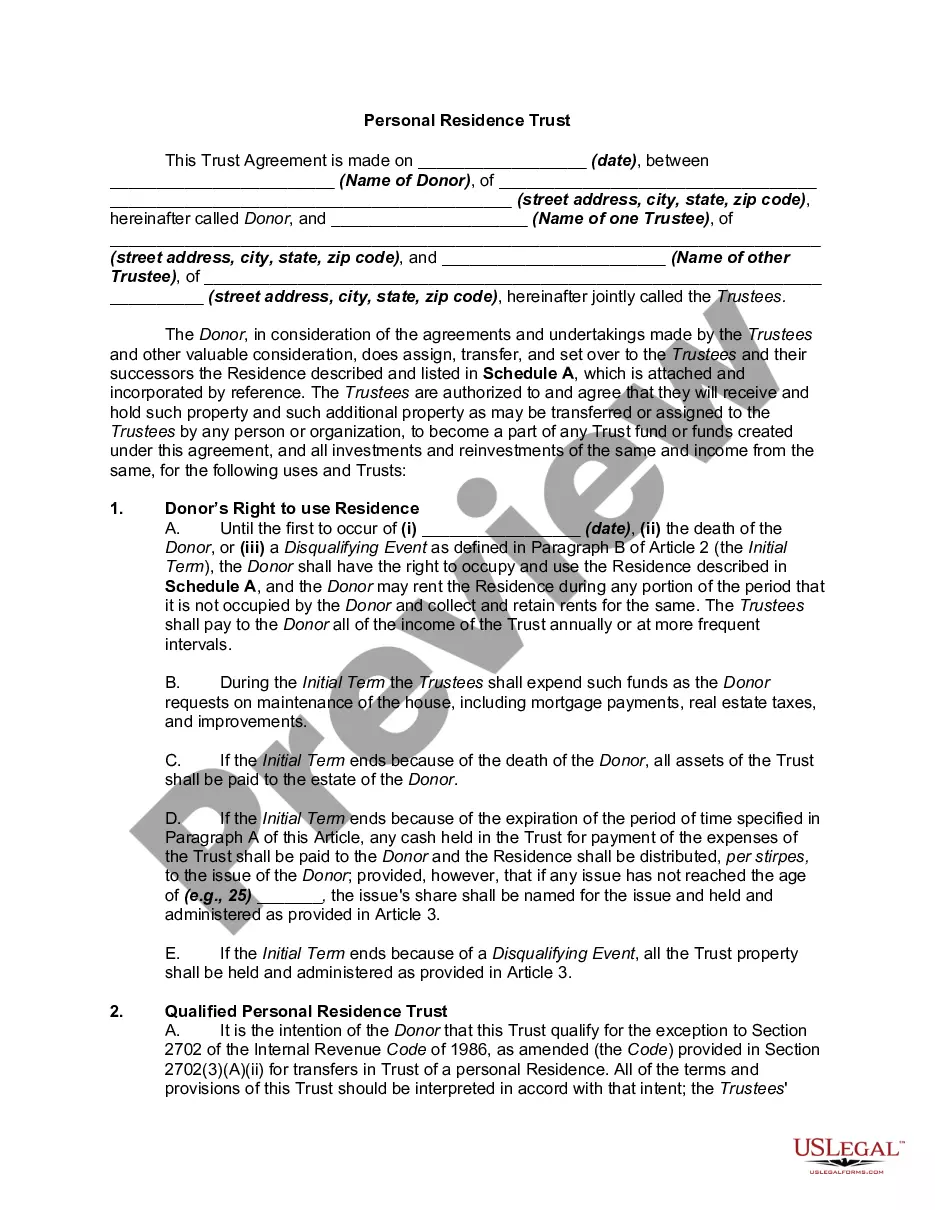

Establishing a Qualified Personal Residence Trust (QPRT) involves transferring the residence to a trust that names the persons who are to receive the residence at the end of the stated term, usually a child or children of the donor. The donor is the tr

New Hampshire Qualified Personal Residence Trust

Instant download

Description

Free preview

How to fill out Qualified Personal Residence Trust?

Have you ever been in a situation where you need documents for both business or personal use almost every day? There are numerous legal document templates available online, but finding ones you can trust is not easy.

US Legal Forms offers a vast array of template options, including the New Hampshire Qualified Personal Residence Trust, designed to satisfy federal and state requirements.

If you are already familiar with the US Legal Forms website and possess an account, simply Log In. Afterwards, you can download the New Hampshire Qualified Personal Residence Trust template.

- Locate the form you require and ensure it is for your correct locality/state.

- Use the Review button to inspect the form.

- Read the description to confirm that you have selected the right form.

- If the form isn’t what you are looking for, utilize the Search field to find the form that fulfills your needs and requirements.

- When you find the appropriate form, click Acquire now.

- Choose the pricing plan that suits you, fill out the necessary details to create your account, and pay for the order using your PayPal or Visa or Mastercard.

- Select a convenient document format and download your copy.

Form popularity

FAQ

QPRT and Other Trust Forms In a bare trust, the beneficiary has the absolute right to the trust's assets (both financial and non-financial, such as real estate and collectibles), as well as the income generated from these assets (such as rental income from properties or bond interest).

QPRT and Other Trust Forms In a bare trust, the beneficiary has the absolute right to the trust's assets (both financial and non-financial, such as real estate and collectibles), as well as the income generated from these assets (such as rental income from properties or bond interest).

A qualified personal residence trust (QPRT) is a trust to which a person (called the settlor, donor, or grantor) transfers his personal residence. The grantor reserves the right to live in the house for a period of years; this retained interest reduces the current value of the gift for gift tax purposes.

A qualified personal residence trust (QPRT) is a specific type of irrevocable trust that allows its creator to remove a personal home from their estate for the purpose of reducing the amount of gift tax that is incurred when transferring assets to a beneficiary.

A qualified personal residence trust (QPRT) is a special type of irrevocable trust that's designed to remove the value of your primary residence or a second home from your taxable estate.

The Qualified Personal Residence Trust offers the benefits of a trust to protect a residence. At the same time, the owner can still live in the house while the trust is in effect. This means while the residence is held within the QPRT it is protected from judgments and creditors.

The biggest benefit of a QPRT is that it removes the value of your primary or second home and its appreciation from your taxable estate. Continued use of the property. With your home in a QPRT, you can still live in the property rent-free and enjoy any income tax deductions associated with it.

Specifically, a QPRT is an irrevocable grantor trust, which allows an individual to take advantage of the gift tax exemption by putting a personal residence, either primary or secondary, into a trust. The grantor determines how long he will retain possession and use of the residence.

What are the Disadvantages of a Trust?Costs. When a decedent passes with only a will in place, the decedent's estate is subject to probate.Record Keeping. It is essential to maintain detailed records of property transferred into and out of a trust.No Protection from Creditors.

Specifically, a QPRT is an irrevocable grantor trust, which allows an individual to take advantage of the gift tax exemption by putting a personal residence, either primary or secondary, into a trust. The grantor determines how long he will retain possession and use of the residence.