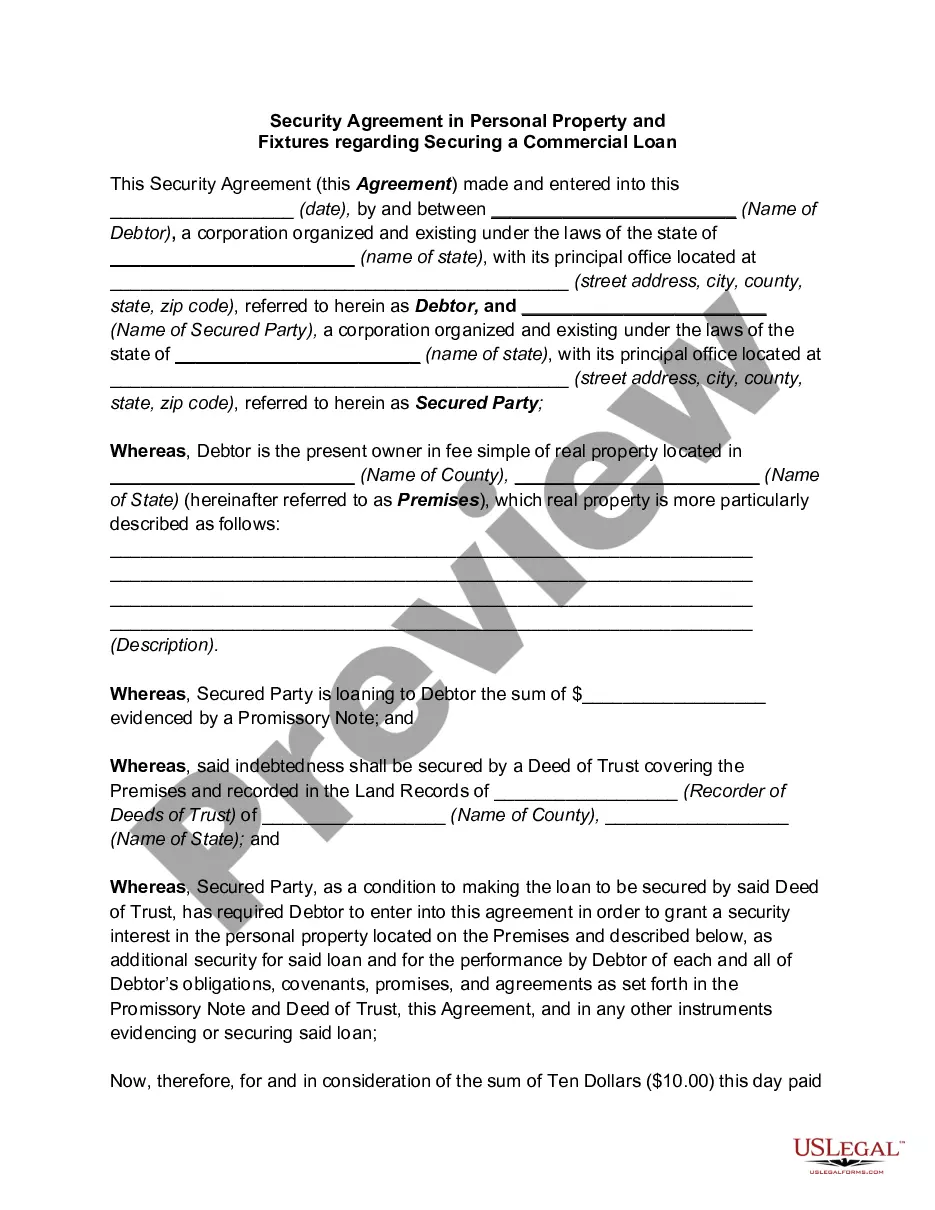

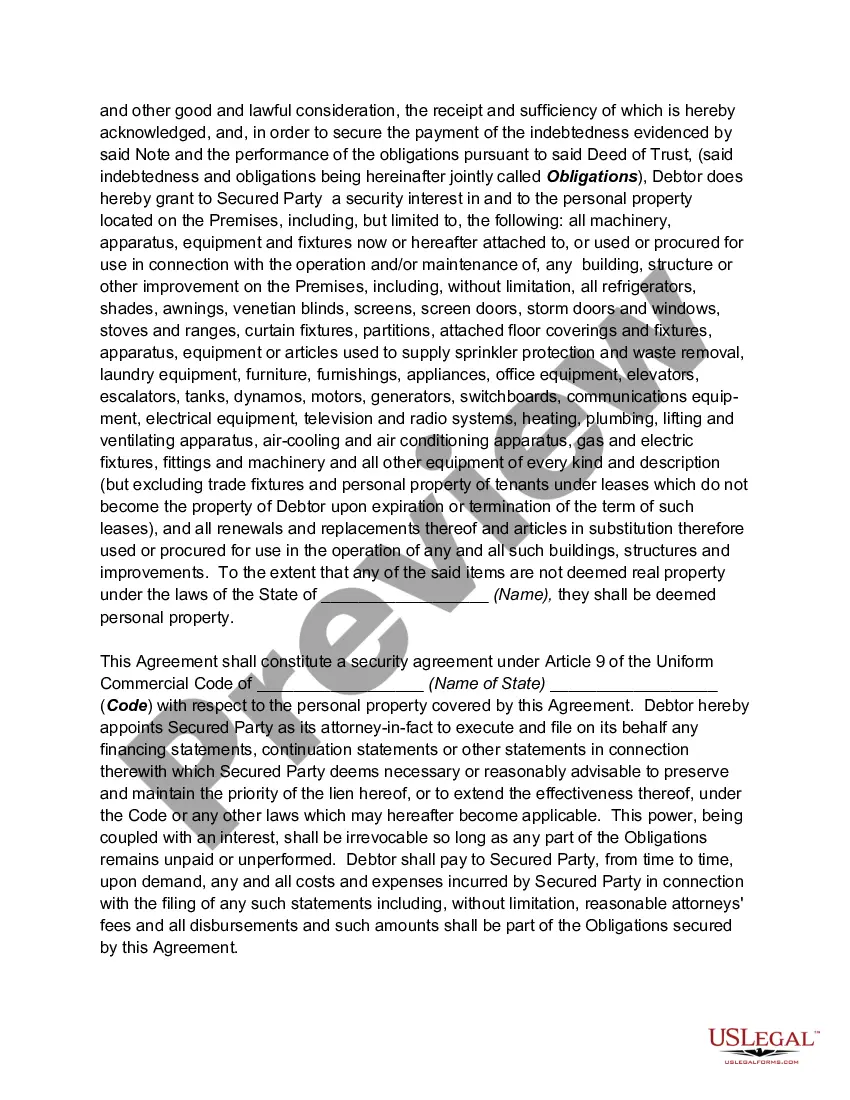

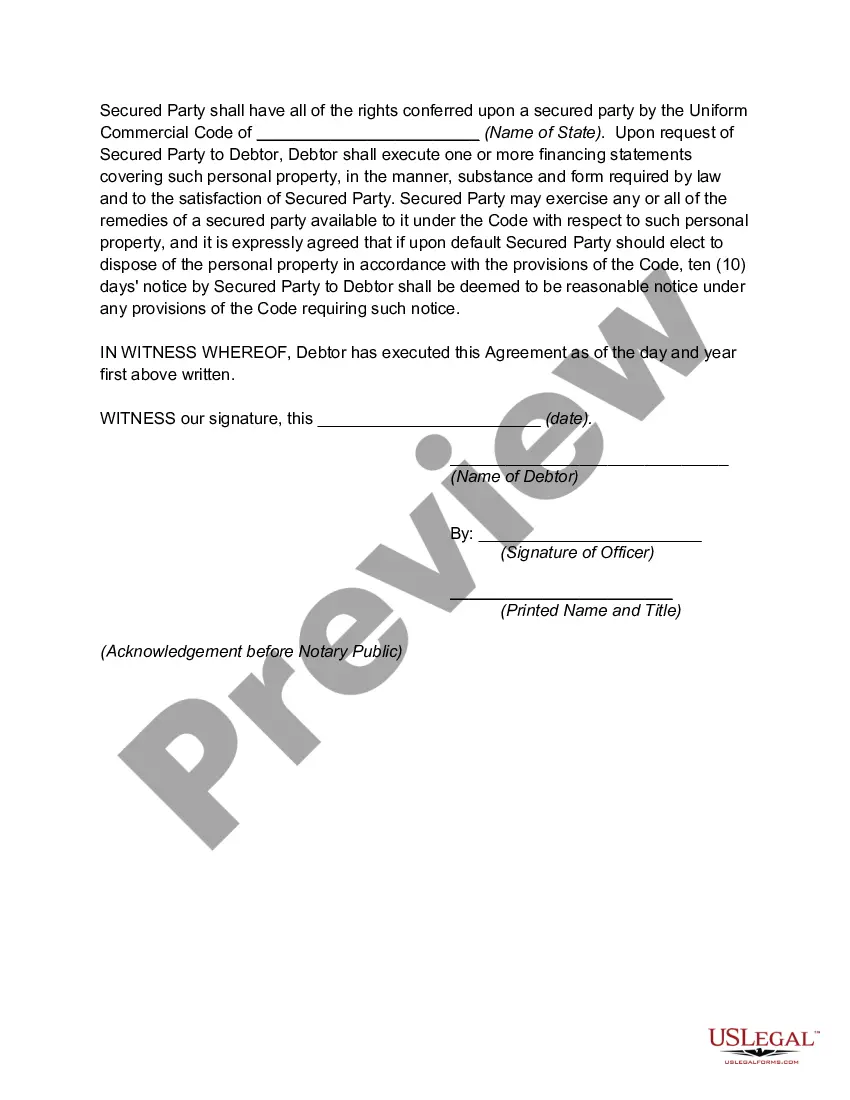

The New Hampshire Security Agreement in Personal Property Fixtures is a legal contract that is used to secure a commercial loan by granting a lender rights over the borrower's personal property fixtures. Personal property fixtures include any movable assets that are attached or affixed to real property, such as machinery, equipment, furniture, and other movable assets used in a commercial setting. This agreement enables lenders to have a security interest in the borrower's personal property fixtures, giving them the ability to recover their investment if the borrower defaults on the loan. By entering into this agreement, the borrower provides the lender with a means to seize and sell the personal property fixtures to repay the outstanding debt. The New Hampshire Security Agreement in Personal Property Fixtures is designed to protect the interests of both parties involved in the commercial loan transaction. Key details specified in this agreement include: 1. Identification of the borrower and lender: The agreement clearly identifies the parties involved, stating their respective legal names and addresses. 2. Description of collateral: The agreement defines the personal property fixtures that are subject to the security interest granted by the borrower. This includes providing detailed descriptions of the assets to ensure clarity and accuracy. 3. Security interest grant: The borrower grants the lender a security interest in the personal property fixtures as collateral for the commercial loan. 4. Perfection of security interest: The agreement addresses how the lender can perfect their security interest, which is typically done by filing a UCC-1 financing statement with the New Hampshire Secretary of State. 5. Rights and obligations of the parties: The agreement outlines the rights and responsibilities of both the borrower and the lender. It often includes provisions related to maintenance and insurance requirements for the collateral, as well as the borrower's obligations to avoid unnecessary liens on the assets. 6. Default and remedies: The agreement specifies the events that would constitute a default, such as non-payment or violation of any terms. Additionally, it outlines the remedies available to the lender in case of default, which may include the right to seize, sell, or otherwise dispose of the collateral. 7. Governing law and dispute resolution: The agreement states that the laws of the State of New Hampshire govern the agreement's interpretation and enforcement. It also often includes provisions related to dispute resolution, outlining the process for resolving any conflicts that may arise. Different variations or types of New Hampshire Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan do not exist. However, commercial loan agreements may have additional provisions and terms specific to the nature of the loan, borrower, or lender. These additional terms may include interest rates, repayment schedules, late fees, or any other details mutually agreed upon by the parties involved.

New Hampshire Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan

Description

How to fill out New Hampshire Security Agreement In Personal Property Fixtures Regarding Securing A Commercial Loan?

You may devote several hours online attempting to find the authorized document design that suits the state and federal requirements you need. US Legal Forms provides a large number of authorized forms that are examined by professionals. You can actually acquire or print out the New Hampshire Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan from our assistance.

If you currently have a US Legal Forms accounts, it is possible to log in and then click the Down load button. After that, it is possible to full, revise, print out, or sign the New Hampshire Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan. Each authorized document design you purchase is your own permanently. To have yet another copy associated with a acquired develop, visit the My Forms tab and then click the related button.

Should you use the US Legal Forms internet site for the first time, follow the basic recommendations below:

- Initial, make sure that you have chosen the right document design to the county/town of your liking. Browse the develop explanation to ensure you have picked the appropriate develop. If available, take advantage of the Review button to appear with the document design as well.

- In order to get yet another variation of the develop, take advantage of the Lookup area to get the design that fits your needs and requirements.

- After you have found the design you would like, just click Get now to carry on.

- Choose the costs plan you would like, type in your qualifications, and register for your account on US Legal Forms.

- Total the purchase. You can utilize your charge card or PayPal accounts to fund the authorized develop.

- Choose the structure of the document and acquire it to your system.

- Make alterations to your document if required. You may full, revise and sign and print out New Hampshire Security Agreement in Personal Property Fixtures regarding Securing a Commercial Loan.

Down load and print out a large number of document themes utilizing the US Legal Forms website, that offers the greatest variety of authorized forms. Use professional and express-specific themes to deal with your organization or person demands.

Form popularity

FAQ

There are three requirements for attachment: (1) the secured party gives value; (2) the debtor has rights in the collateral or the power to transfer rights in it to the secured party; (3) the parties have a security agreement ?authenticated? (signed) by the debtor, or the creditor has possession of the collateral.

Security interest is an enforceable legal claim or lien on collateral that has been pledged, usually to obtain a loan. The borrower provides the lender with a security interest in certain assets, which gives the lender the right to repossess all or part of the property if the borrower stops making loan payments.

A security interest is not enforceable unless it has attached. Attachment of a security interest generally requires a written security agreement, description of collateral, secured party's giving value, and the debtor having rights in collateral.

Security interest is an interest in personal property or fixtures that secures payment or performance of an obligation. Secured party is a lender, seller, or other person in whose favor a security interest exists.

Security Interest: An interest in personal property or fixtures -- i.e., improvements to real property -- which secures payment or performance of an obligation. Security Agreement: An agreement creating or memorializing a security interest granted by a debtor to a secured party.

Below are common types of security interests that apply to land. Mortgage. This is a loan instrument where an individual acquires a loan to buy a house. ... Deed of Trust. In the US, a deed of trust is a legal instrument used to create security interests. ... A contract for the sale of land.

Let's consider an example. Credit transactions involving large ticket items, such as cars, homes or appliances, are usually secured. When I bought my new car, I borrowed money from my bank for my car loan. My loan is a secured transaction.

In order for a security interest to be enforceable against the debtor and third parties, UCC Article 9 sets forth three requirements: Value must be provided in exchange for the collateral; the debtor must have rights in the collateral or the ability to convey rights in the collateral to a secured party; and either the ...