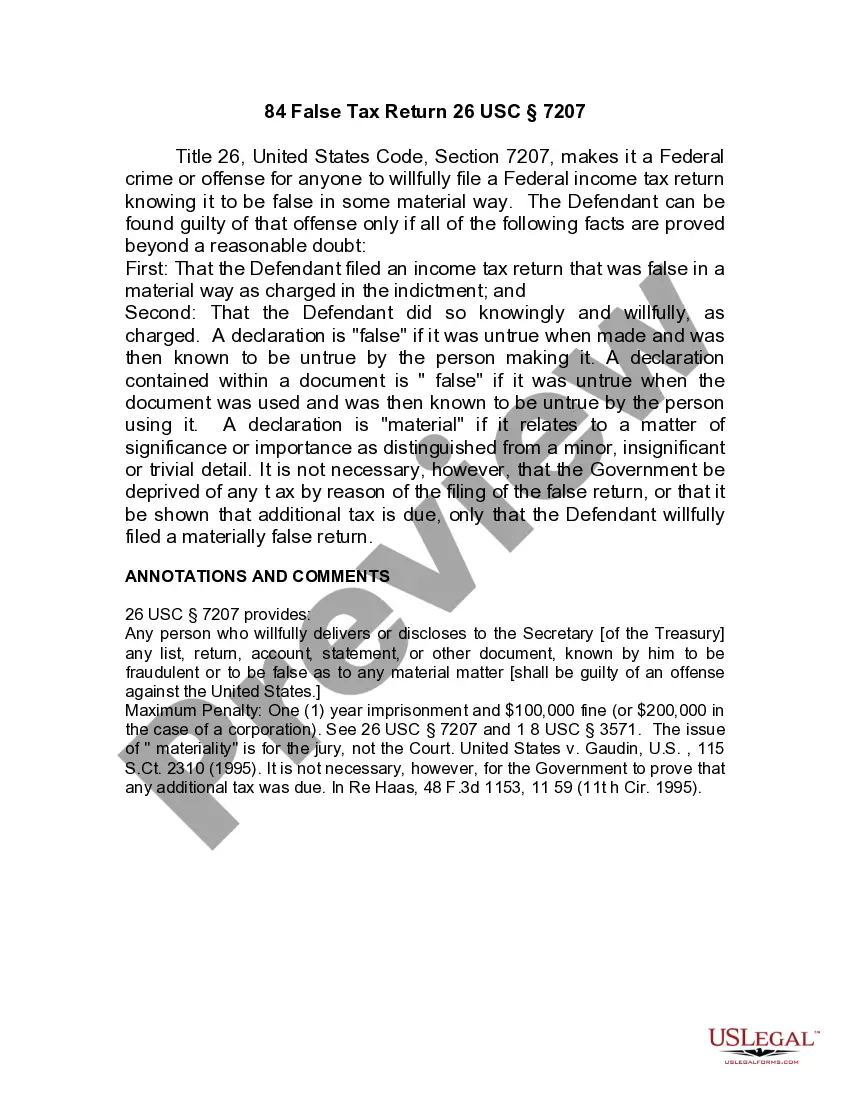

New Hampshire Jury Instruction - 10.10.6 Section 6672 Penalty

Description

How to fill out Jury Instruction - 10.10.6 Section 6672 Penalty?

It is possible to invest time on the web trying to find the authorized papers web template that suits the state and federal requirements you want. US Legal Forms provides 1000s of authorized types which can be evaluated by experts. You can actually download or printing the New Hampshire Jury Instruction - 10.10.6 Section 6672 Penalty from our support.

If you already possess a US Legal Forms accounts, it is possible to log in and click on the Obtain button. Afterward, it is possible to total, edit, printing, or signal the New Hampshire Jury Instruction - 10.10.6 Section 6672 Penalty. Each and every authorized papers web template you get is your own property permanently. To get an additional backup of any obtained type, visit the My Forms tab and click on the related button.

If you are using the US Legal Forms site for the first time, adhere to the straightforward directions beneath:

- Initially, be sure that you have chosen the proper papers web template for that state/town of your liking. Read the type information to make sure you have selected the correct type. If readily available, take advantage of the Preview button to appear with the papers web template as well.

- If you would like discover an additional version of the type, take advantage of the Lookup area to discover the web template that meets your needs and requirements.

- Once you have discovered the web template you want, click on Get now to proceed.

- Choose the prices program you want, enter your credentials, and register for a merchant account on US Legal Forms.

- Comprehensive the transaction. You can use your charge card or PayPal accounts to purchase the authorized type.

- Choose the structure of the papers and download it for your gadget.

- Make changes for your papers if needed. It is possible to total, edit and signal and printing New Hampshire Jury Instruction - 10.10.6 Section 6672 Penalty.

Obtain and printing 1000s of papers layouts using the US Legal Forms website, that provides the biggest variety of authorized types. Use skilled and condition-distinct layouts to deal with your small business or specific needs.