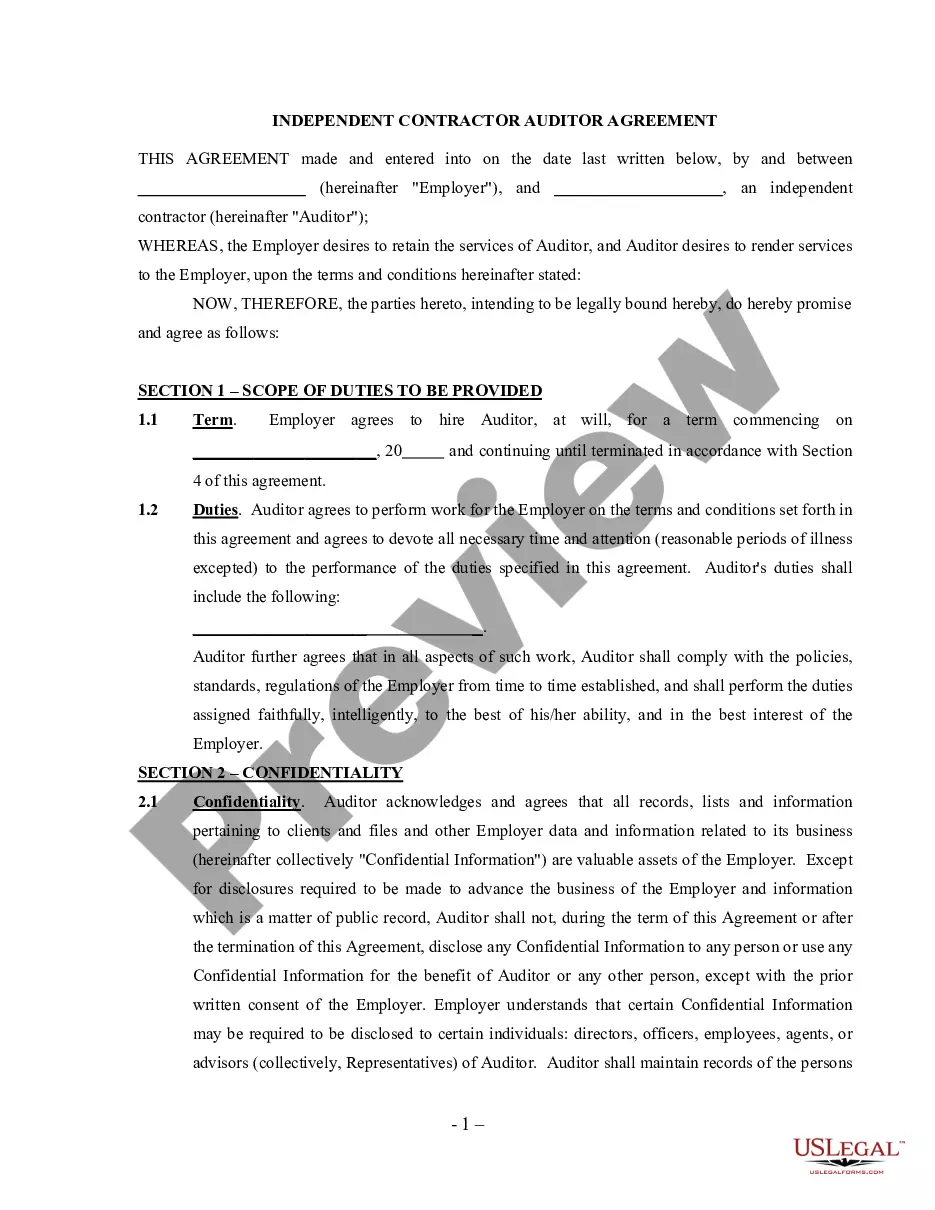

New Hampshire Agreement for Auditing Services between Accounting Firm and Municipality

Description

How to fill out Agreement For Auditing Services Between Accounting Firm And Municipality?

You are able to devote hours on-line searching for the lawful record web template that fits the state and federal needs you require. US Legal Forms provides a huge number of lawful forms that happen to be reviewed by professionals. It is possible to download or print the New Hampshire Agreement for Auditing Services between Accounting Firm and Municipality from your services.

If you have a US Legal Forms accounts, you may log in and click on the Acquire button. Next, you may complete, change, print, or sign the New Hampshire Agreement for Auditing Services between Accounting Firm and Municipality. Each lawful record web template you purchase is your own property forever. To get yet another backup of any acquired kind, proceed to the My Forms tab and click on the related button.

If you use the US Legal Forms website the very first time, follow the straightforward recommendations below:

- Very first, make certain you have selected the correct record web template for your county/area of your choice. Read the kind outline to ensure you have chosen the proper kind. If offered, utilize the Review button to check through the record web template also.

- If you would like find yet another edition of your kind, utilize the Look for field to discover the web template that meets your needs and needs.

- Upon having identified the web template you need, click Acquire now to proceed.

- Find the rates plan you need, key in your credentials, and sign up for your account on US Legal Forms.

- Total the transaction. You should use your bank card or PayPal accounts to fund the lawful kind.

- Find the file format of your record and download it for your product.

- Make adjustments for your record if necessary. You are able to complete, change and sign and print New Hampshire Agreement for Auditing Services between Accounting Firm and Municipality.

Acquire and print a huge number of record web templates while using US Legal Forms web site, that provides the largest collection of lawful forms. Use specialist and condition-certain web templates to deal with your organization or personal requires.

Form popularity

FAQ

Steps for conducting a financial audit Understand your goals. ... Decide what to include in your audit. ... Gather and organise your materials. ... Begin data analysis. ... Consider financial security. ... Examine tax reporting status. ... Compile a report. How to conduct a financial audit with detailed instructions | Indeed.com UK indeed.com ? career-development ? how-to-co... indeed.com ? career-development ? how-to-co...

Auditors perform audit procedures to get all the information they need to assess their clients' numbers and form an opinion on their financial statements. Audit procedures vary from audit to audit and client to client but generally include analytical reviews, inquiry, inspection, observation and recalculation.

Whether seeking an audit committee's permission to provide permissible tax services or other non-audit services to a public company audit client or when preparing to take a public company on as a new audit client, three important steps are: Describe, discuss, and document. Request, explain, and record. Acct. Ethics-Module 3a and 3b Flashcards | Quizlet quizlet.com ? ... quizlet.com ? ...

An audit engagement letter is a written agreement that outlines the scope of your work as an auditor, what the client is responsible for, how long the audit is estimated to take, and details about your fee, among other things. It is a binding contractual agreement between you and each of your clients.

The auditor and the client should agree on the terms of the engagement. The agreed terms would need to be recorded in an audit engagement letter or other suitable form of contract. 3. This PSA is intended to assist the auditor in the preparation of engagement letters relating to audits of financial statements.

C) the client provides capital to the external users. D) the external users can rely upon the auditor's report to reduce information risk. Answer:D. the external users can rely upon the auditor 's report to reduce information risk .

Basically, the audit team would perform inquiry with management, analytical procedures, and tie-out the financial statements to the company's internal financial statements. No substantive testing or internal control testing is performed during a review for quarterly financial statements. Are quarterly financial statements audited for public companies? universalcpareview.com ? ask-joey ? are-qu... universalcpareview.com ? ask-joey ? are-qu...

The engagement letter documents and confirms the auditor's acceptance of the appointment, the objective and scope of the audit, the extent of the auditor's responsibilities to the client and the form of any reports. Introduction Audit Engagement Letters Agreement on Written ... iaasb.org ? system ? files ? meetings ? files iaasb.org ? system ? files ? meetings ? files