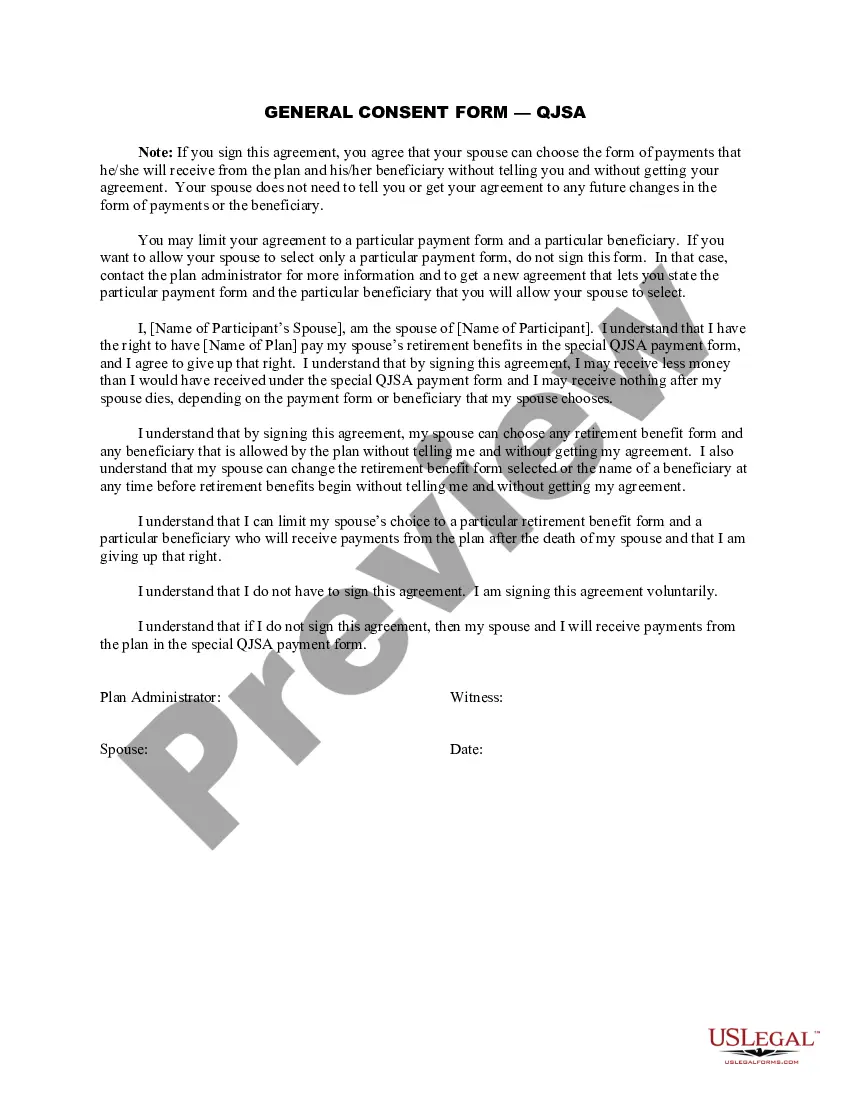

The New Hampshire General Consent Form for Qualified Joint and Survivor Annuities (JSA) is a legal document designed to provide individuals with a detailed understanding of the specific provisions and requirements related to obtaining a JSA. This form plays a crucial role in ensuring that individuals are well-informed about their options and can make informed decisions regarding their retirement benefits. Keywords: New Hampshire, General Consent Form, Qualified Joint and Survivor Annuities, JSA, legal document, provisions, requirements, retirement benefits, informed decisions There are two common types of New Hampshire General Consent Forms for Qualified Joint and Survivor Annuities JSASA: 1. Standard QJSA Consent Form: This type of consent form outlines the default options for choosing a JSA. It provides a detailed description of how the benefits will be distributed during the lifetime of the annuitant and after their death to their spouse or beneficiary. The form contains sections that explain the terms and conditions, survivor benefits, and any limitations or restrictions associated with selecting a JSA. 2. Optional JSA Consent Form: This form provides individuals with alternative options for choosing a JSA arrangement that may better suit their specific needs and circumstances. It allows the annuitant to customize the JSA plan by tailoring the distribution of benefits to match their preferences. The form includes detailed information on various election choices, including percentage allocation, payment frequency, and beneficiary designations. Both types of consent forms are crucial to ensure that individuals have a comprehensive understanding of the JSA provisions, potential benefits, and any associated risks. It is important for individuals to carefully review and complete the form, particularly considering the long-term implications it may have on their retirement savings and the financial security of their spouse or beneficiary. Note: The specific names and content of the consent forms may vary slightly depending on the insurance company or financial institution offering the annuity. It is essential to refer to the official documentation and consult with a qualified financial advisor for the most accurate and up-to-date information.

New Hampshire General Consent Form for Qualified Joint and Survivor Annuities - QJSA

Description

How to fill out New Hampshire General Consent Form For Qualified Joint And Survivor Annuities - QJSA?

If you wish to total, acquire, or produce legal file web templates, use US Legal Forms, the most important assortment of legal varieties, which can be found online. Take advantage of the site`s easy and handy look for to discover the paperwork you want. Various web templates for organization and specific uses are categorized by categories and says, or keywords. Use US Legal Forms to discover the New Hampshire General Consent Form for Qualified Joint and Survivor Annuities - QJSA within a few click throughs.

In case you are already a US Legal Forms consumer, log in to your accounts and click on the Download button to find the New Hampshire General Consent Form for Qualified Joint and Survivor Annuities - QJSA. Also you can accessibility varieties you previously delivered electronically from the My Forms tab of your own accounts.

If you are using US Legal Forms for the first time, follow the instructions beneath:

- Step 1. Be sure you have chosen the shape for that appropriate metropolis/country.

- Step 2. Make use of the Review method to examine the form`s content material. Don`t overlook to see the description.

- Step 3. In case you are not happy with all the type, take advantage of the Look for area on top of the monitor to locate other versions in the legal type template.

- Step 4. Upon having discovered the shape you want, go through the Acquire now button. Pick the rates plan you choose and include your accreditations to register to have an accounts.

- Step 5. Procedure the deal. You should use your bank card or PayPal accounts to finish the deal.

- Step 6. Pick the formatting in the legal type and acquire it on your device.

- Step 7. Complete, edit and produce or indicator the New Hampshire General Consent Form for Qualified Joint and Survivor Annuities - QJSA.

Every legal file template you get is your own forever. You possess acces to every type you delivered electronically within your acccount. Select the My Forms area and choose a type to produce or acquire again.

Be competitive and acquire, and produce the New Hampshire General Consent Form for Qualified Joint and Survivor Annuities - QJSA with US Legal Forms. There are thousands of expert and state-distinct varieties you can use for your organization or specific demands.