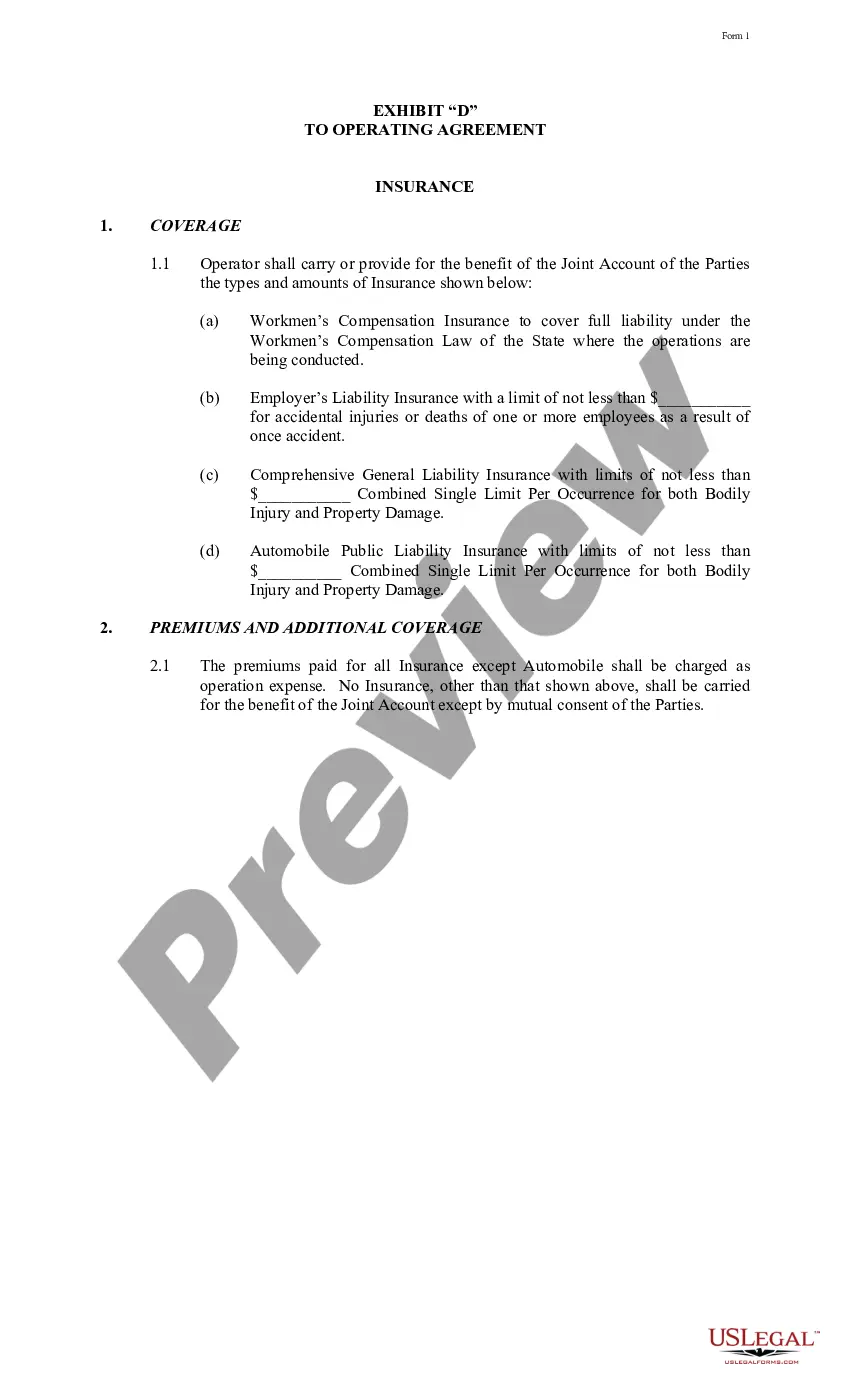

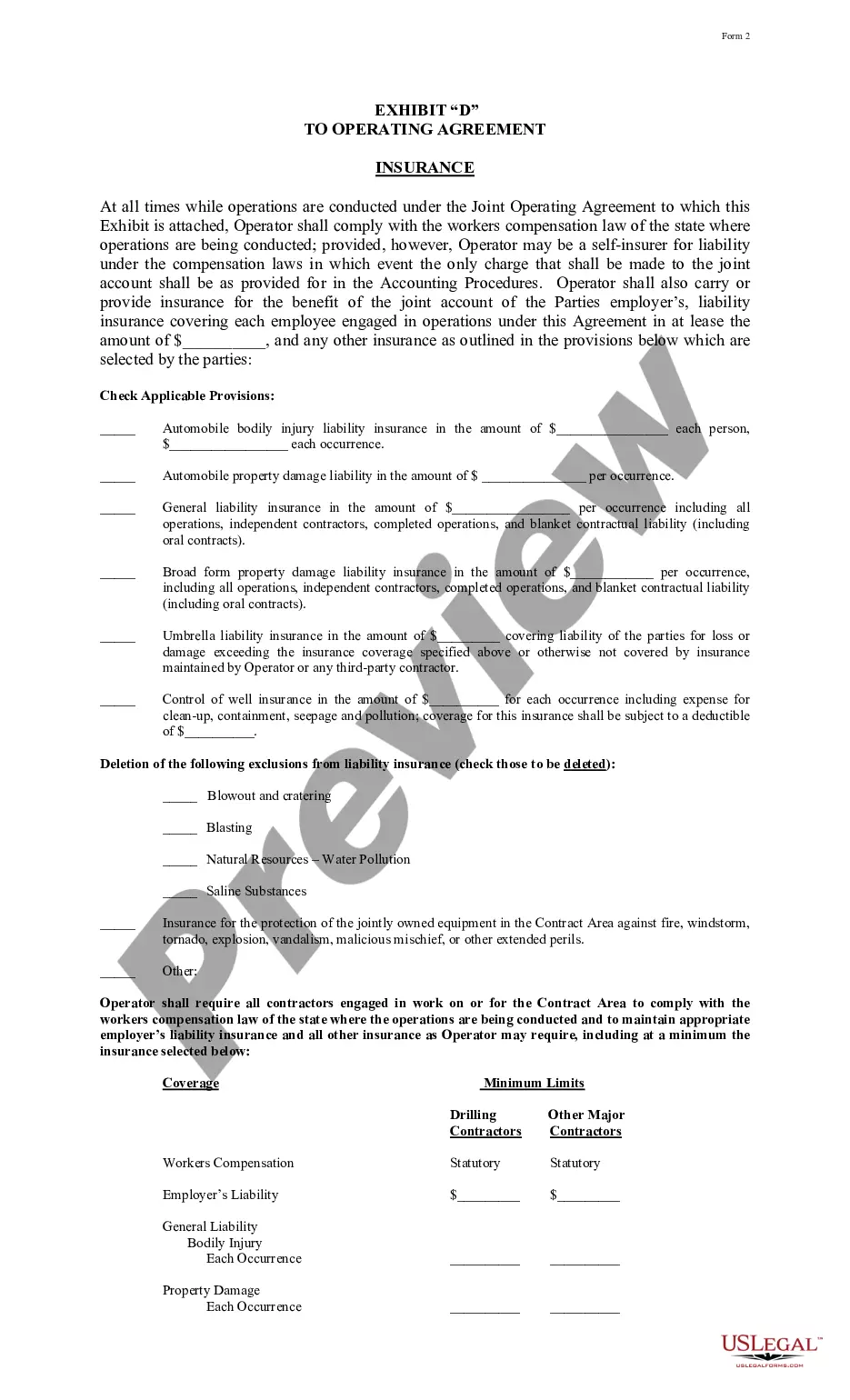

New Hampshire Exhibit C Accounting Procedure Joint Operations

Description

How to fill out Exhibit C Accounting Procedure Joint Operations?

Choosing the best lawful file design might be a battle. Needless to say, there are tons of layouts available online, but how can you get the lawful form you want? Take advantage of the US Legal Forms site. The service offers a huge number of layouts, like the New Hampshire Exhibit C Accounting Procedure Joint Operations, which you can use for company and private requirements. All of the forms are checked by pros and satisfy state and federal needs.

In case you are already authorized, log in to the profile and then click the Down load option to find the New Hampshire Exhibit C Accounting Procedure Joint Operations. Make use of your profile to check through the lawful forms you possess ordered formerly. Go to the My Forms tab of your own profile and acquire an additional copy of your file you want.

In case you are a whole new user of US Legal Forms, allow me to share simple instructions for you to stick to:

- First, ensure you have selected the appropriate form to your city/region. It is possible to look through the form while using Review option and browse the form information to make certain it will be the best for you.

- In the event the form is not going to satisfy your needs, take advantage of the Seach area to get the correct form.

- Once you are sure that the form would work, click the Acquire now option to find the form.

- Select the rates plan you would like and enter the required info. Build your profile and pay money for your order utilizing your PayPal profile or Visa or Mastercard.

- Choose the data file structure and down load the lawful file design to the product.

- Comprehensive, modify and printing and sign the attained New Hampshire Exhibit C Accounting Procedure Joint Operations.

US Legal Forms is the biggest library of lawful forms for which you will find a variety of file layouts. Take advantage of the service to down load expertly-produced files that stick to express needs.