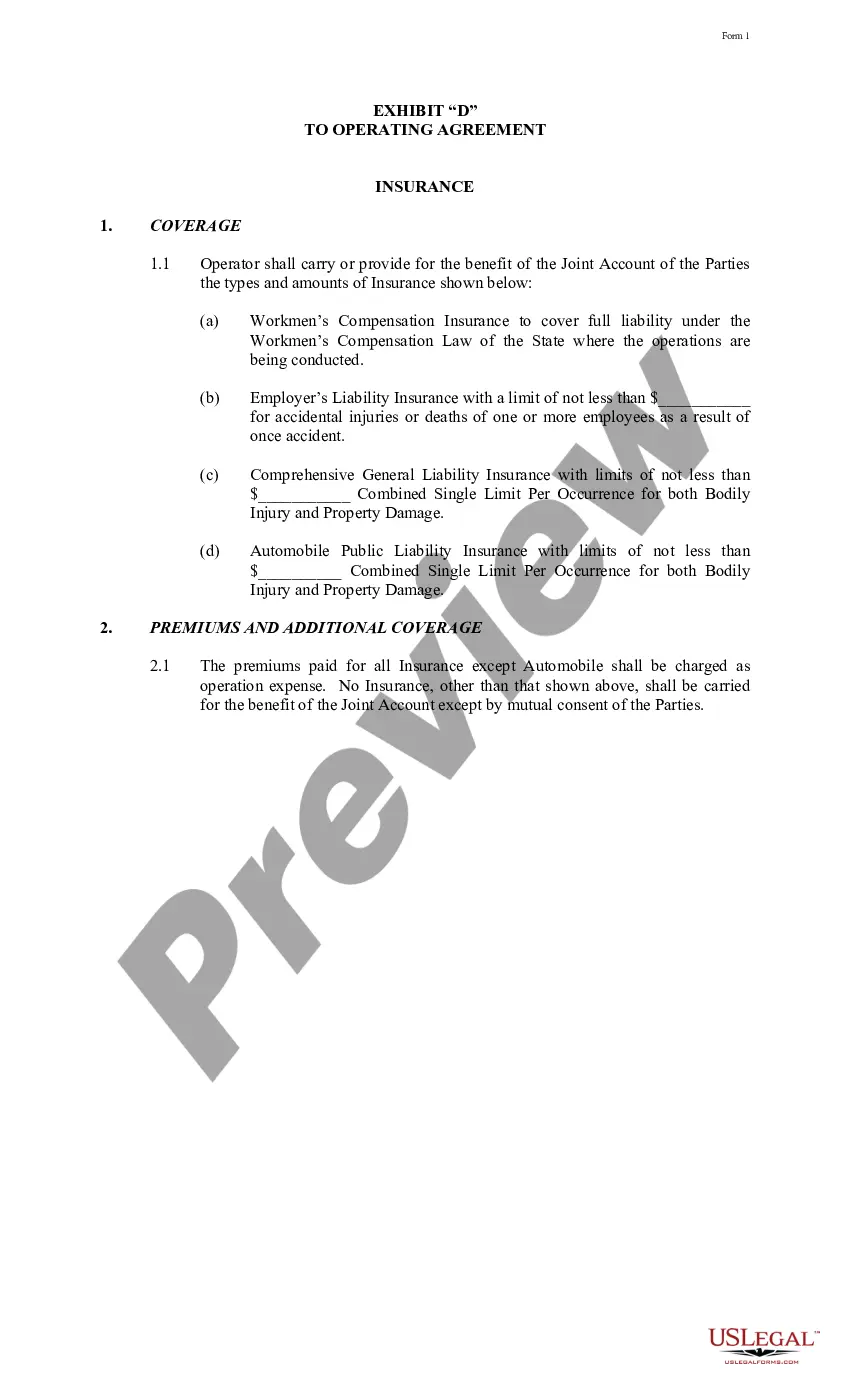

New Hampshire Exhibit D to Operating Agreement Insurance - Form 2

Description

How to fill out Exhibit D To Operating Agreement Insurance - Form 2?

US Legal Forms - among the most significant libraries of authorized kinds in the USA - provides an array of authorized file templates it is possible to acquire or print. While using web site, you can get a large number of kinds for organization and individual reasons, categorized by types, says, or search phrases.You can find the latest variations of kinds just like the New Hampshire Exhibit D to Operating Agreement Insurance - Form 2 in seconds.

If you already possess a subscription, log in and acquire New Hampshire Exhibit D to Operating Agreement Insurance - Form 2 from your US Legal Forms library. The Obtain option will show up on every develop you perspective. You gain access to all previously acquired kinds in the My Forms tab of the account.

In order to use US Legal Forms initially, listed here are straightforward directions to get you started off:

- Be sure to have chosen the best develop for your personal area/area. Go through the Review option to examine the form`s information. See the develop outline to ensure that you have chosen the right develop.

- When the develop doesn`t suit your requirements, utilize the Look for discipline at the top of the display to get the one who does.

- In case you are content with the form, verify your choice by clicking the Acquire now option. Then, opt for the rates program you like and provide your references to sign up to have an account.

- Approach the purchase. Make use of your Visa or Mastercard or PayPal account to accomplish the purchase.

- Choose the format and acquire the form in your product.

- Make alterations. Load, edit and print and sign the acquired New Hampshire Exhibit D to Operating Agreement Insurance - Form 2.

Each template you included in your account does not have an expiration day and is also your own forever. So, if you would like acquire or print yet another version, just visit the My Forms segment and click on around the develop you will need.

Get access to the New Hampshire Exhibit D to Operating Agreement Insurance - Form 2 with US Legal Forms, probably the most substantial library of authorized file templates. Use a large number of specialist and status-particular templates that meet up with your company or individual demands and requirements.

Form popularity

FAQ

How to Start an LLC in New Hampshire Name Your LLC. First of all, your business needs a name. ... Designate a Registered Agent. Next, you need to appoint a registered agent. ... Submit LLC Certificate of Formation. ... Write an LLC Operating Agreement. ... Get an EIN. ... Open a Bank Account. ... Fund the LLC. ... File State Reports & Taxes.

New Hampshire LLC Processing Times Normal LLC processing time:Expedited LLC:New Hampshire LLC by mail:7-10 business days (plus mail time)Not availableNew Hampshire LLC online:7-10 business daysNot available

Put It In Writing ? A Delaware LLC should have a written copy of the Operating Agreement that is signed and agreed upon by all the LLC members.

Create an operating agreement An operating agreement is a document that outlines the way your LLC will conduct business. New Hampshire doesn't require an operating agreement, but it is an essential component of your business.

New Hampshire LLC Formation Filing Fee: $100 Filing your Certificate of Formation has a fee of $100. You can submit the certificate through the mail or in person, or you can do it online through NH QuickStart, though you'll need to add $2 for online filings.

Best States to Form an LLC: Key Takeaways But for most small and mid-sized businesses, your home state is the simplest and least expensive option. Delaware, Wyoming, Nevada, and New Hampshire are all business-friendly states that could be appealing alternatives to your home state in specific circumstances.

How Are New Hampshire LLCs Taxed? Your New Hampshire LLC's tax classification depends on its number of members. Single-member LLCs (SMLLCs) are taxed like sole proprietors by default, and multi-member LLCs are taxed as general partnerships.