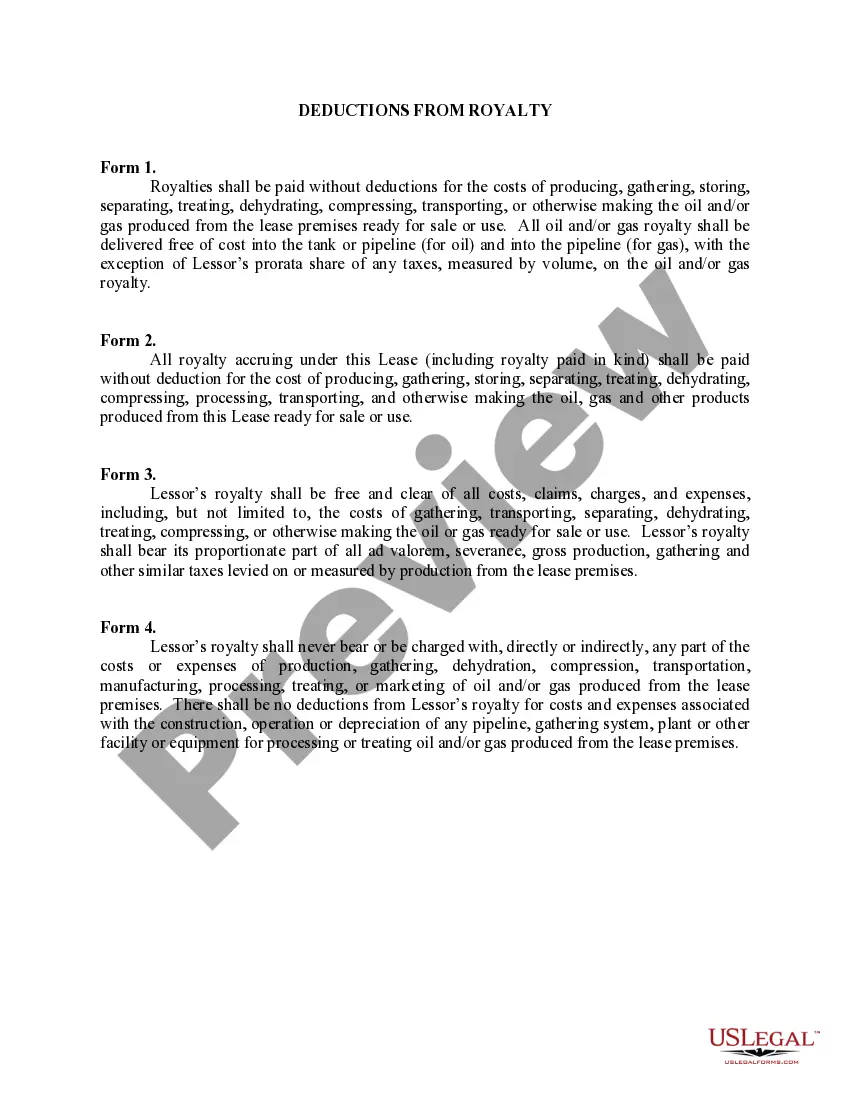

This lease rider form may be used when you are involved in a lease transaction, and have made the decision to utilize the form of Oil and Gas Lease presented to you by the Lessee, and you want to include additional provisions to that Lease form to address specific concerns you may have, or place limitations on the rights granted the Lessee in the “standard” lease form.

New Hampshire Deductions from Royalty: Explained with Relevant Keywords New Hampshire provides various deductions from royalty for businesses and individuals engaged in intellectual property rights and licensing activities. These deductions aim to promote economic growth, attract businesses, and encourage innovation within the state. Let's delve into the different types of New Hampshire Deductions from Royalty available: 1. Intellectual Property Royalty Deductions: New Hampshire allows businesses to deduct royalties paid for the usage or licensing of intellectual property such as patents, trademarks, copyrights, or trade secrets. This deduction encourages businesses to invest in innovation and intellectual property development while reducing their overall tax liability. 2. Royalty Income Deductions: Individuals who earn royalty income from intellectual property rights can deduct a portion of these earnings from their taxable income. The state acknowledges the value of creative works, such as books, music, and artwork, by providing deductions that alleviate the tax burden on individuals generating income from royalties. 3. Innovation and Research Deductions: New Hampshire supports research and development activities by providing deductions from royalty payments related to innovative technologies or advancements. These deductions aim to incentivize businesses to invest in research, development, and other innovative projects, ultimately boosting the local economy and attracting cutting-edge enterprises. 4. In-State Investment Deductions: To promote growth within the state, New Hampshire offers additional deductions for businesses that invest in or acquire intellectual property from companies located within its borders. This encourages companies to invest in local enterprises and enhances the overall competitiveness and collaboration within the state. 5. Educational Royalty Deductions: Educational institutions in New Hampshire enjoy deductions for royalty payments made for the use of intellectual property in research, teaching materials, or other educational purposes. These deductions help to support research-driven educational initiatives, foster academic collaborations, and enrich the educational experiences provided by the state's institutions. By providing these deductions, New Hampshire aims to create an environment conducive to intellectual property development, technological advancements, and innovative business practices. These measures attract businesses, foster economic growth, support local enterprises, and promote a culture of innovation within the state. Key terms: New Hampshire, deductions from royalty, intellectual property, patents, trademarks, copyrights, trade secrets, economic growth, innovation, tax liability, royalty income, creative works, research and development, in-state investment, educational institutions, teaching materials, technological advancements, business practices.