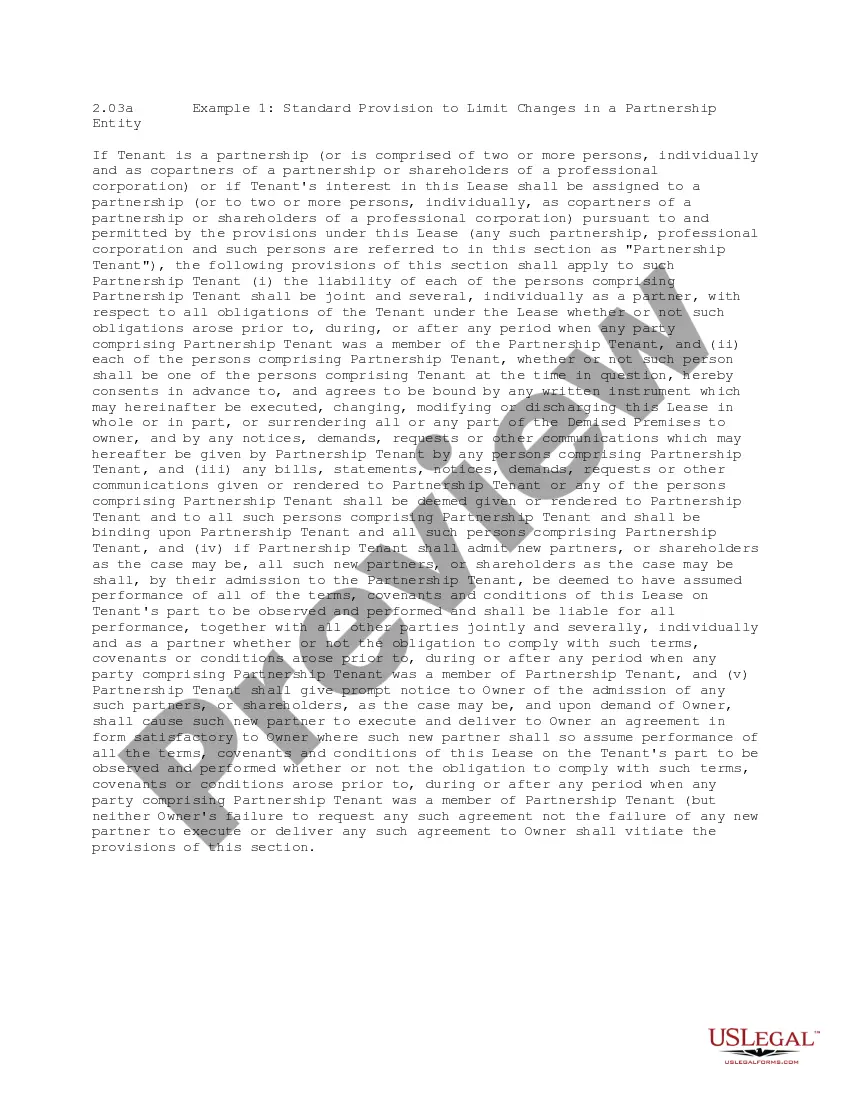

This office lease provision refers to a tenant that is a partnership or if the tenant's interest in the lease shall be assigned to a partnership. Any such partnership, professional corporation and such persons will be held by this provision of the lease.

New Hampshire Standard Provision to Limit Changes in a Partnership Entity: In New Hampshire, a partnership entity can have various standard provisions to limit changes within the entity. These provisions aim to establish a framework that ensures stability and protects the rights and interests of the partners. Some key types of provisions applicable in New Hampshire are: 1. Partnership Agreement: The partnership agreement serves as the backbone of the entity and typically contains provisions that outline the roles, responsibilities, and decision-making processes within the partnership. It defines the rights and obligations of the partners and sets limitations on changes that can be made without proper consensus or amendments. 2. Restriction on Admission of New Partners: This provision limits the ability of existing partners to admit new partners into the entity without unanimous consent or approval from a designated majority. It helps maintain the cohesiveness of the partnership by preventing unexpected changes in partner composition. 3. Restriction on Withdrawal or Retirement: These provisions establish conditions and limitations on partner withdrawal or retirement from the partnership. They typically require prior notice, a voting process, or buyouts to ensure a smooth transition and protect the interests of the remaining partners. 4. Limitations on Transfer of Partnership Interests: These provisions regulate the transfer of partnership interests from one partner to another. They may require approval from other partners, restrict transfers to outsiders, or set terms for valuation and purchase of interests to control and maintain continuity within the partnership. 5. Dissolution or Termination: Provisions related to dissolution and termination outline the circumstances under which a partnership may be dissolved or terminated. They address various situations such as bankruptcy, death of a partner, or the occurrence of specified events, and contemplate procedures and distribution of assets upon dissolution. 6. Amendment Process: This provision establishes a mechanism for making changes to the partnership agreement. It typically requires unanimous or majority consent from the partners, formal documentation, and adherence to legal requirements for amendments. 7. Dispute Resolution: These provisions address the resolution of disputes that may arise among the partners. They may incorporate mechanisms such as mediation, arbitration, or court proceedings to facilitate fair and efficient resolution. 8. Governing Law: The governing law provision specifies the legal jurisdiction or state law under which the partnership entity operates. In New Hampshire, the partnership entity is generally subject to the laws and regulations of the state. It is important for partners to consult with legal professionals when preparing or amending the partnership agreement and its provisions to ensure compliance with New Hampshire laws and to address specific needs and circumstances of the partnership entity.

New Hampshire Standard Provision to Limit Changes in a Partnership Entity: In New Hampshire, a partnership entity can have various standard provisions to limit changes within the entity. These provisions aim to establish a framework that ensures stability and protects the rights and interests of the partners. Some key types of provisions applicable in New Hampshire are: 1. Partnership Agreement: The partnership agreement serves as the backbone of the entity and typically contains provisions that outline the roles, responsibilities, and decision-making processes within the partnership. It defines the rights and obligations of the partners and sets limitations on changes that can be made without proper consensus or amendments. 2. Restriction on Admission of New Partners: This provision limits the ability of existing partners to admit new partners into the entity without unanimous consent or approval from a designated majority. It helps maintain the cohesiveness of the partnership by preventing unexpected changes in partner composition. 3. Restriction on Withdrawal or Retirement: These provisions establish conditions and limitations on partner withdrawal or retirement from the partnership. They typically require prior notice, a voting process, or buyouts to ensure a smooth transition and protect the interests of the remaining partners. 4. Limitations on Transfer of Partnership Interests: These provisions regulate the transfer of partnership interests from one partner to another. They may require approval from other partners, restrict transfers to outsiders, or set terms for valuation and purchase of interests to control and maintain continuity within the partnership. 5. Dissolution or Termination: Provisions related to dissolution and termination outline the circumstances under which a partnership may be dissolved or terminated. They address various situations such as bankruptcy, death of a partner, or the occurrence of specified events, and contemplate procedures and distribution of assets upon dissolution. 6. Amendment Process: This provision establishes a mechanism for making changes to the partnership agreement. It typically requires unanimous or majority consent from the partners, formal documentation, and adherence to legal requirements for amendments. 7. Dispute Resolution: These provisions address the resolution of disputes that may arise among the partners. They may incorporate mechanisms such as mediation, arbitration, or court proceedings to facilitate fair and efficient resolution. 8. Governing Law: The governing law provision specifies the legal jurisdiction or state law under which the partnership entity operates. In New Hampshire, the partnership entity is generally subject to the laws and regulations of the state. It is important for partners to consult with legal professionals when preparing or amending the partnership agreement and its provisions to ensure compliance with New Hampshire laws and to address specific needs and circumstances of the partnership entity.