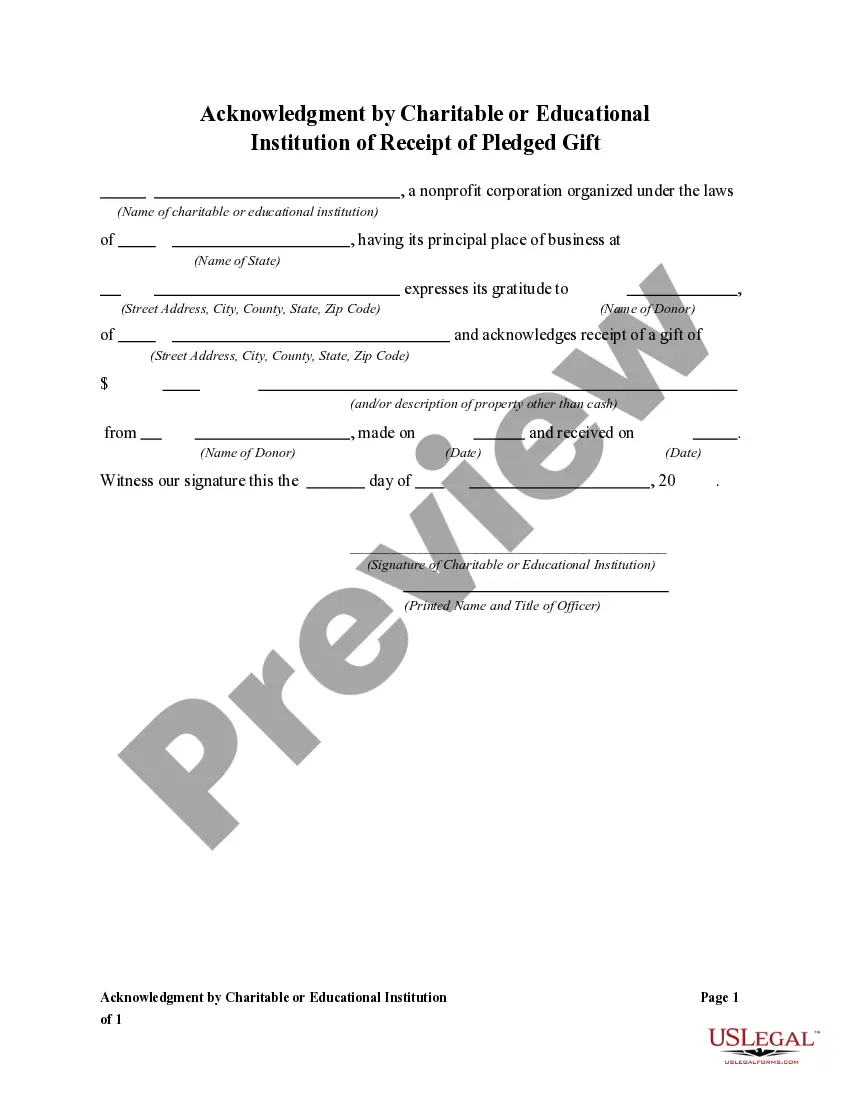

Title: Understanding the New Jersey Acknowledgment by Charitable or Educational Institution of Receipt of Gift Introduction: The New Jersey Acknowledgment by Charitable or Educational Institution of Receipt of Gift is a crucial process that ensures transparency and accountability in the state's charitable and educational sector. Accredited institutions must appropriately acknowledge and record any gifts they receive to comply with legal and regulatory requirements. In this article, we will delve into the details of this acknowledgment and explore different types of acknowledgments that may exist. 1. Importance of Acknowledgments: Charitable and educational institutions depend heavily on donations and gifts to fund their programs and initiatives. The acknowledgment process provides both legal and ethical assurances to donors, allowing them to claim tax deductions while ensuring that their contributions are used as intended. 2. Essential Elements of an Acknowledgment: A proper acknowledgment should contain specific important elements, including: — The institution's name and contact information — The donor's name and contact information — The date and descriptiotariffif— - A statement clarifying whether any goods/services were exchanged for the gift — A statement acknowledging that no favors, services, or goods were provided in return for the gift, if applicable — A statement indicating whether the institution has exclusive control over the assets received 3. Different Types of Acknowledgments: Depending on the nature of the gift or donation, various types of acknowledgments may be required by New Jersey law. Some common types include: — Monetary Contributions: Acknowledgments for cash donations, checks, credit card transactions, or electronic transfers. — In-Kind Donations: Acknowledgments for non-cash gifts, such as property, equipment, or materials. — Securities or Stocks: Acknowledgments related to the transfer of securities or stocks issued by publicly-traded companies. — Planned Giving: Acknowledgments for contributions received through bequests, Charitable Remainder Trusts (CRTs), or Charitable Gift Annuities (Gas). — Vehicle Donations: Acknowledgments for donations of vehicles, where the donor is eligible for a tax deduction based on the vehicle's fair market value. 4. Compliance with Tax Laws: New Jersey IRS tax regulations require that charitable and educational institutions comply with specific rules regarding acknowledgments. Institutions failing to meet these compliance requirements risk penalties or the loss of their tax-exempt status. 5. Retention and Reporting: Proper record-keeping is crucial to substantiate donations and support the institution in the event of an audit. Institutions must retain all gift acknowledgments, along with any accompanying documentation, for a specified period. Additionally, a summary report of all gifts received during a tax year must be submitted to the New Jersey Division of Taxation. Conclusion: Accurate and comprehensive acknowledgment of gifts received by charitable and educational institutions plays an essential role in maintaining public trust and fulfilling legal obligations. By complying with New Jersey's requirements, institutions ensure transparency, accountability, and promote ongoing donor support. Stay informed about the specific types of acknowledgments required and keep abreast of any changes in applicable laws to ensure compliance and smooth operations.

Title: Understanding the New Jersey Acknowledgment by Charitable or Educational Institution of Receipt of Gift Introduction: The New Jersey Acknowledgment by Charitable or Educational Institution of Receipt of Gift is a crucial process that ensures transparency and accountability in the state's charitable and educational sector. Accredited institutions must appropriately acknowledge and record any gifts they receive to comply with legal and regulatory requirements. In this article, we will delve into the details of this acknowledgment and explore different types of acknowledgments that may exist. 1. Importance of Acknowledgments: Charitable and educational institutions depend heavily on donations and gifts to fund their programs and initiatives. The acknowledgment process provides both legal and ethical assurances to donors, allowing them to claim tax deductions while ensuring that their contributions are used as intended. 2. Essential Elements of an Acknowledgment: A proper acknowledgment should contain specific important elements, including: — The institution's name and contact information — The donor's name and contact information — The date and descriptiotariffif— - A statement clarifying whether any goods/services were exchanged for the gift — A statement acknowledging that no favors, services, or goods were provided in return for the gift, if applicable — A statement indicating whether the institution has exclusive control over the assets received 3. Different Types of Acknowledgments: Depending on the nature of the gift or donation, various types of acknowledgments may be required by New Jersey law. Some common types include: — Monetary Contributions: Acknowledgments for cash donations, checks, credit card transactions, or electronic transfers. — In-Kind Donations: Acknowledgments for non-cash gifts, such as property, equipment, or materials. — Securities or Stocks: Acknowledgments related to the transfer of securities or stocks issued by publicly-traded companies. — Planned Giving: Acknowledgments for contributions received through bequests, Charitable Remainder Trusts (CRTs), or Charitable Gift Annuities (Gas). — Vehicle Donations: Acknowledgments for donations of vehicles, where the donor is eligible for a tax deduction based on the vehicle's fair market value. 4. Compliance with Tax Laws: New Jersey IRS tax regulations require that charitable and educational institutions comply with specific rules regarding acknowledgments. Institutions failing to meet these compliance requirements risk penalties or the loss of their tax-exempt status. 5. Retention and Reporting: Proper record-keeping is crucial to substantiate donations and support the institution in the event of an audit. Institutions must retain all gift acknowledgments, along with any accompanying documentation, for a specified period. Additionally, a summary report of all gifts received during a tax year must be submitted to the New Jersey Division of Taxation. Conclusion: Accurate and comprehensive acknowledgment of gifts received by charitable and educational institutions plays an essential role in maintaining public trust and fulfilling legal obligations. By complying with New Jersey's requirements, institutions ensure transparency, accountability, and promote ongoing donor support. Stay informed about the specific types of acknowledgments required and keep abreast of any changes in applicable laws to ensure compliance and smooth operations.