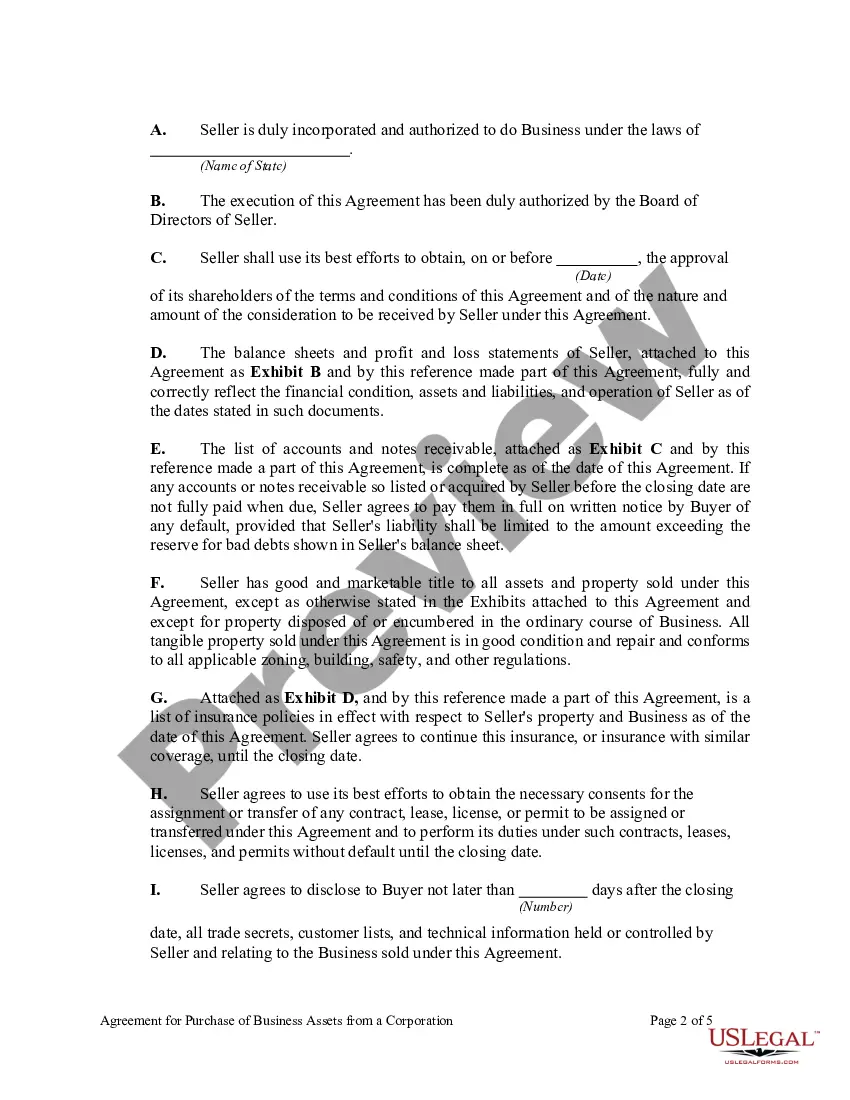

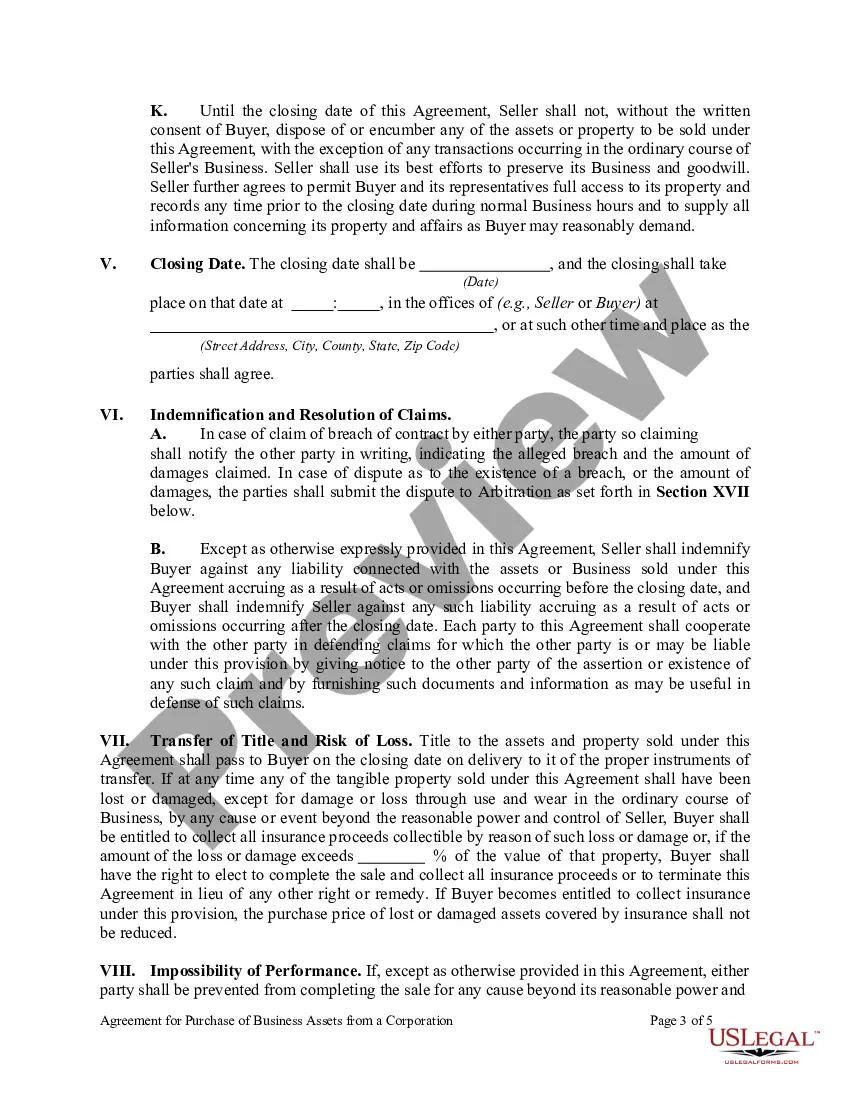

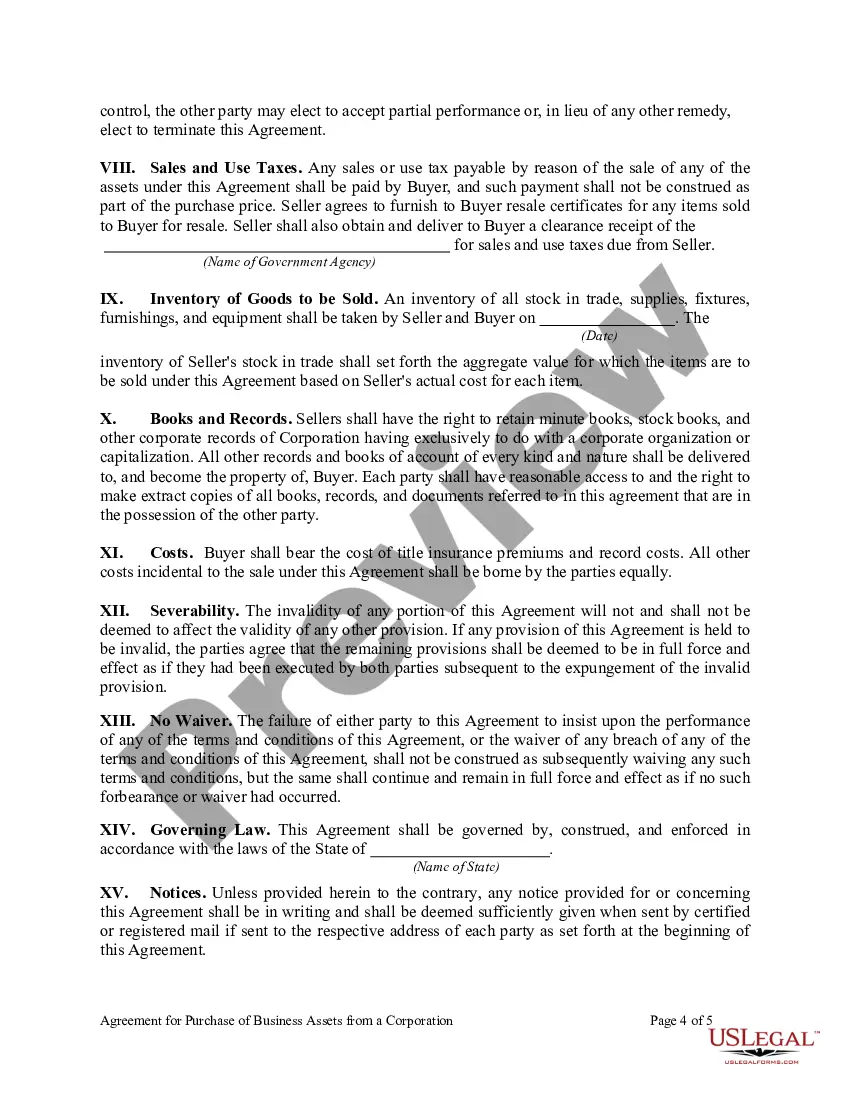

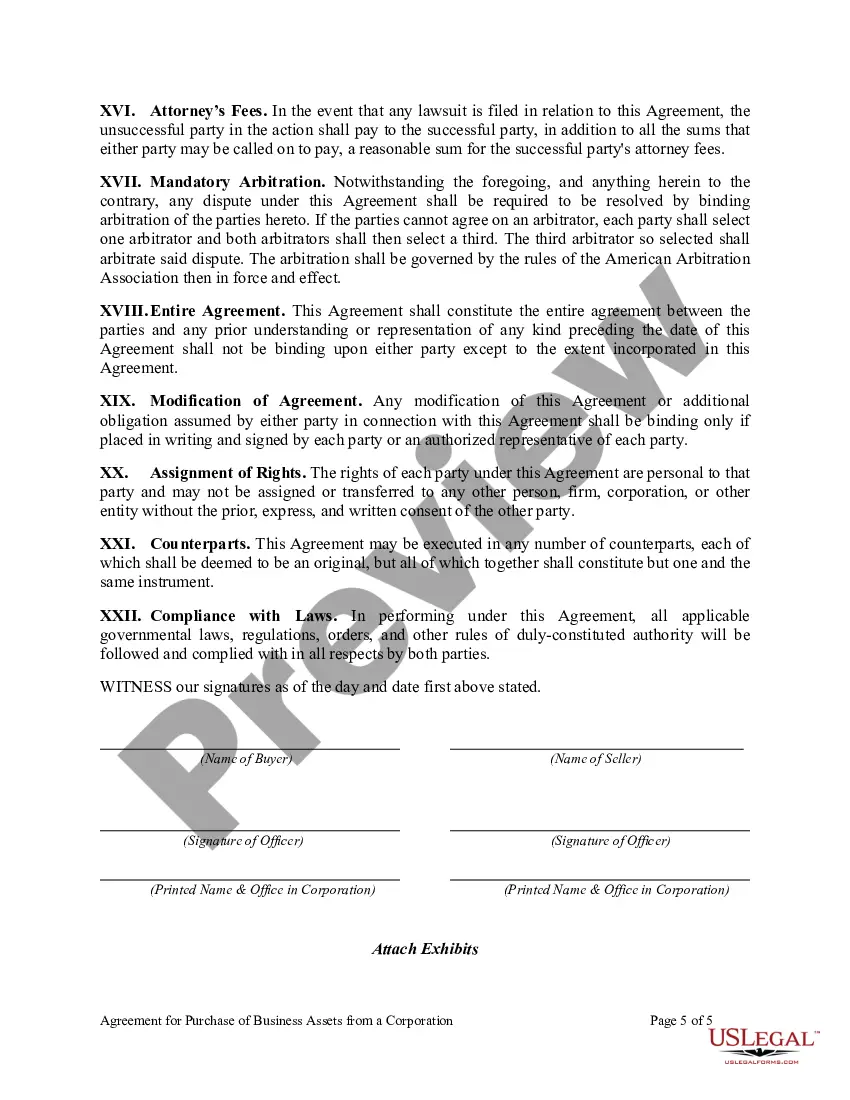

The New Jersey Agreement for Purchase of Business Assets from a Corporation is a legally binding document that facilitates the transfer of ownership of business assets from a corporation to a buyer. This agreement outlines the terms and conditions of the sale, protecting the interests of both the buyer and the seller. The agreement generally includes key elements such as the purchase price, payment terms, identification of the assets being sold, representations and warranties, and any specific conditions or contingencies. It ensures that both parties understand and agree upon the terms of the transaction, reducing the risk of potential disputes in the future. There are different types of New Jersey Agreement for Purchase of Business Assets from a Corporation depending on the nature of the transaction. These may include: 1. Asset Purchase Agreement: This type of agreement involves the purchase of specific assets of a corporation, such as inventory, equipment, intellectual property, customer contracts, and goodwill. The buyer may choose to acquire only certain assets instead of taking over the entire business. 2. Stock Purchase Agreement: In contrast to the asset purchase agreement, this type involves the purchase of all outstanding shares of a corporation. By acquiring the stock, the buyer assumes control of the corporation, including both its assets and liabilities. 3. Merger Agreement: This agreement is used when two corporations decide to merge into a single entity. The merger agreement outlines the terms of the consolidation, including the transfer of assets, assumption of liabilities, and exchange of stock. When drafting a New Jersey Agreement for Purchase of Business Assets from a Corporation, it is important to include relevant keywords to ensure clarity and specificity. Some keywords that may be applicable to include "purchase price," "payment terms," "assets," "representations and warranties," "conditions," "contingencies," "inventory," "equipment," "intellectual property," "customer contracts," "goodwill," "stock," "merger," and "liabilities."

New Jersey Agreement for Purchase of Business Assets from a Corporation

Description

How to fill out New Jersey Agreement For Purchase Of Business Assets From A Corporation?

You can devote hours on the web trying to find the authorized papers design that meets the federal and state needs you require. US Legal Forms offers thousands of authorized forms that happen to be reviewed by professionals. You can easily obtain or print the New Jersey Agreement for Purchase of Business Assets from a Corporation from the support.

If you have a US Legal Forms accounts, you can log in and then click the Obtain option. Afterward, you can complete, change, print, or indication the New Jersey Agreement for Purchase of Business Assets from a Corporation. Each and every authorized papers design you buy is your own permanently. To acquire one more backup of any purchased kind, proceed to the My Forms tab and then click the related option.

Should you use the US Legal Forms website initially, adhere to the basic guidelines under:

- Initial, make sure that you have selected the correct papers design for your region/town of your choosing. Look at the kind information to make sure you have picked out the proper kind. If available, make use of the Review option to check through the papers design at the same time.

- If you want to get one more edition of the kind, make use of the Research field to obtain the design that suits you and needs.

- Once you have found the design you want, click Get now to continue.

- Find the costs program you want, enter your references, and register for an account on US Legal Forms.

- Total the transaction. You may use your credit card or PayPal accounts to purchase the authorized kind.

- Find the file format of the papers and obtain it to your gadget.

- Make alterations to your papers if required. You can complete, change and indication and print New Jersey Agreement for Purchase of Business Assets from a Corporation.

Obtain and print thousands of papers layouts utilizing the US Legal Forms website, that offers the biggest variety of authorized forms. Use professional and state-certain layouts to tackle your small business or individual requires.